Modern market insights indicate that China starch sugar industry 2026 performance has quietly positioned the nation as the world’s largest producer and exporter of starch-based sweeteners.

China has quietly become the world’s largest producer and exporter of starch-based sweeteners—a category known as starch sugar —yet the sector remains largely underreported in Western industry media. As global food and beverage manufacturers increasingly scout for cost-competitive sugar alternatives, understanding China’s starch sugar landscape has never been more relevant.

What Is Starch Sugar?

Starch sugar is a broad category of sweeteners derived from starch-rich crops—primarily corn, wheat, and cassava—through a series of industrial processes including liquefaction, saccharification, isomerization, and purification. The end products vary significantly in composition and application:

-

Liquid Sweeteners: High-fructose corn syrup (HFCS), maltose syrup, and glucose syrup.

-

Solid Sweeteners: Crystalline glucose (dextrose) and maltodextrin.

These products are characterized by adjustable sweetness levels, high solubility, and functional versatility, making them suitable replacements or complements to cane and beet sugar across a wide range of industrial applications.

Market Size and Growth Trajectory

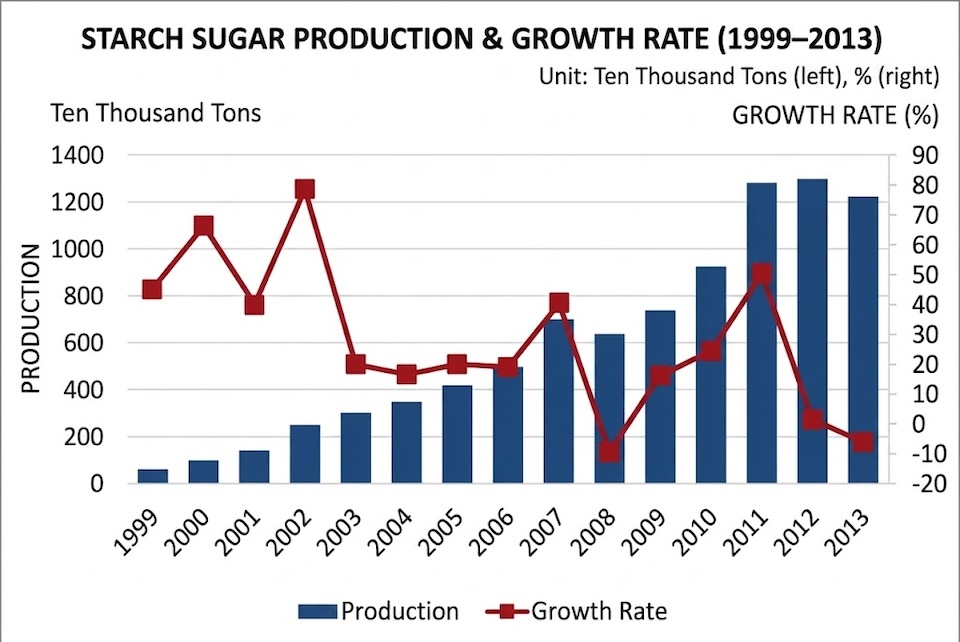

China’s starch sugar industry traces its modern origins to 1999. Growth has been rapid and sustained: annual output crossed the 10 million metric ton (MMT) threshold in 2011, reached 16.88 MMT in 2022, and surged to 19.15 MMT in 2023—representing a near-doubling of output in just over a decade.

For the 2025/2026 marketing years, industry data indicates the market has entered a mature high-volume plateau, balancing solid domestic demand with expanding export volumes.

Starch sugar has become a structurally important substitute for cane and beet sugar in the Chinese sweetener market, helping to narrow the country’s persistent sugar supply deficit. Given that China imports millions of tons of refined sugar annually, the domestic starch sugar industry serves a genuine strategic function in reducing overall import dependency.

Demand Drivers and End-Use Structure

The food and beverage sector dominates consumption, accounting for the vast majority of starch sugar demand. A breakdown by application segment reveals the following distribution:

China Starch Sugar End-Use Structure (%)

├── Beverage Industry : ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ 36% (Mainly HFCS)

├── Food Processing : ▓▓▓▓▓▓▓▓▓▓▓▓ 23%

├── General Food Manufacturing : ▓▓▓▓▓▓▓ 14%

├── Beer Brewing : ▓▓▓▓ 8%

└── Frozen Desserts & Ice Cream : ▓▓▓ 6%

(Note: Pharmaceuticals, chemicals, and fermentation account for the remaining share)

Maltodextrin deserves special mention—it plays an outsized role in frozen dessert formulations and condiment manufacturing, where its texturizing and bulking properties are valued alongside sweetness.

Several macro trends are reinforcing demand growth:

-

Premiumization: The upgrading of products in China’s urban consumer market requires more sophisticated and tailored sweetener profiles.

-

Functional Foods: Increased market traction for glucose oligomers and specific sugar alcohols that offer health-positioning opportunities.

-

Health-Conscious Reformulation: Driving localized demand for low-glycemic and low-calorie starch-derived sweeteners.

-

Cost Competitiveness: Starch-based alternatives offer excellent cost stability relative to sucrose, particularly as cane sugar prices remain volatile on global commodity markets.

Regional Production Concentration

Starch sugar manufacturing in China is geographically clustered around both raw material sources and downstream consumption hubs. Shandong Province leads nationally, accounting for approximately 39% of total output—a reflection of its massive corn processing infrastructure and proximity to major food industry clusters. Guangdong, Hebei, and Jilin round out the top four producing provinces.

Demand is especially strong in the economically developed coastal regions of East China (华东) and South China (华南), where the concentration of food manufacturers, beverage companies, and pharmaceutical producers creates dense end-user markets.

Competitive Landscape

The Chinese starch sugar market remains fragmented relative to other mature commodity processing industries, though consolidation is accelerating. The top 10 producers collectively account for approximately 65.62% of national output by volume. The leading players and their estimated production shares are:

| Producer Name | Market Share (%) | Regional Strength / Profile |

| Guangzhou Shuangqiao | 10.49% | Market leader; highly dominant in the South China market. |

| Zhucheng Xingmao | 8.30% | Massive processing capacity based in northern corn belts. |

| Yufeng Industrial | 8.10% | Strong integrated agricultural processing footprint. |

| Luzhou Food | 7.83% | Multi-regional manufacturing bases. |

| COFCO Biotechnology | 6.62% | State-owned industry leader with deep vertical integration. |

Other notable participants include Xiwang Sugar and various specialized subsidiaries of COFCO Group.

Large producers enjoy compounding competitive advantages: economies of scale in raw material procurement, proprietary enzyme and fermentation technology, and established distribution networks into global food conglomerates. Smaller and mid-sized producers face a more difficult operating environment—rising corn input costs, stricter environmental compliance requirements, and margin compression from larger rivals are accelerating industry consolidation.

Major Capacity Expansion Projects (2025–2026)

Two landmark investment projects signal strong long-term institutional confidence in the sector’s growth:

1. COFCO Biotechnology (SZ: 000930) — Taicang, Jiangsu

In April 2025, COFCO Biotechnology announced plans to construct a 550,000-ton-per-year starch sugar facility in Taicang, Jiangsu Province, with total investment approaching RMB 1 billion (~USD 138 million). The project directly targets the Yangtze River Delta’s dense food and beverage manufacturing base and reflects COFCO’s strategy of vertically integrating its grain processing operations with high-value sweetener production.

2. Shuangqiao (Jiaxing) Biotech — Haining, Zhejiang

In May 2026, Shuangqiao (Jiaxing) Biotechnology Co., Ltd.—a wholly owned subsidiary of Guangzhou Shuangqiao established during the 2025 restructuring—publicly filed environmental and construction disclosures for a landmark 1,000,000-ton-per-year starch sugar and liquid sugar complex in Haining, Zhejiang.

The project involves the acquisition of approximately 200 mu (~13.3 hectares) of industrial land and the installation of a fully integrated production system, including:

-

Bulk starch unloading, saccharification, membrane filtration, ion exchange, activated carbon decolorization, isomerization, MVR evaporative concentration, bipolar membrane electrodialysis, chromatographic separation, biogas boiler systems, wastewater treatment, and fully automated packaging and tank truck filling lines.

Upon completion, the facility is projected to generate annual revenues of RMB 3.5 billion (~USD 480 million), with a total project investment exceeding RMB 1.3 billion (~USD 179 million). This expansion positions Shuangqiao to extend its historical South China leadership directly into the strategically critical East China market.

YnSugar Outlook

China’s starch sugar industry is transitioning from a high-growth, fragmented phase into a more mature, consolidation-driven era. Key dynamics to watch include:

-

Further M&A activity as large producers absorb or displace smaller local competitors.

-

Functional and specialty sweetener growth, particularly in low-calorie and prebiotic sugar categories.

-

Export expansion, as Chinese starch sugar producers aggressively explore Southeast Asian and broader emerging market opportunities.

-

Regulatory and environmental pressure potentially accelerating capacity rationalization among less compliant smaller mills.

For international food ingredient buyers, contract manufacturers, and investors tracking the Asian sweetener supply chain, China’s starch sugar sector represents both a significant sourcing opportunity and a structural force reshaping global sweetener market dynamics.

Data Sources: * China Starch Industry Association (CSIA) Annual Reports.

-

Corporate Disclosures & Environmental Impact Assessment (EIA) Filings (COFCO Biotechnology & Shuangqiao Biotech, 2025-2026).

-

YnSugar Internal Industry Database.