China Sugar Imports 2025–2026 · Full Data Analysis

China Sugar Import Report 2025–2026

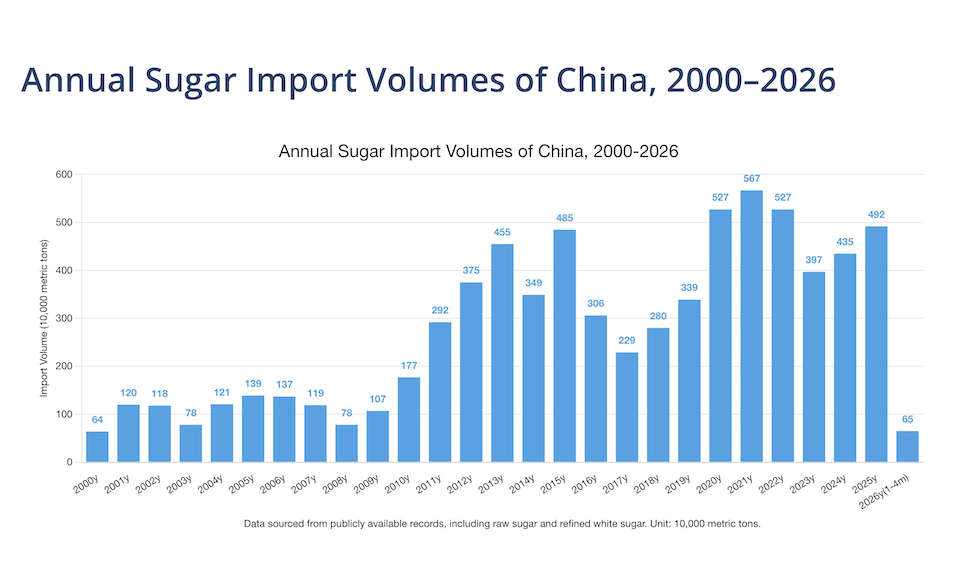

China imported 4.92 million MT of sugar in 2025 — remaining elevated despite recovering domestic production and weaker global sugar prices. Brazil dominates supply, while provincial and trade-type structures show significant new shifts.

4.918M

Total Annual Imports (MT)

+12.89%

Year-on-Year Growth

87.26%

Share from Brazil

CNY 3,162

Avg. CIF Price (per MT)

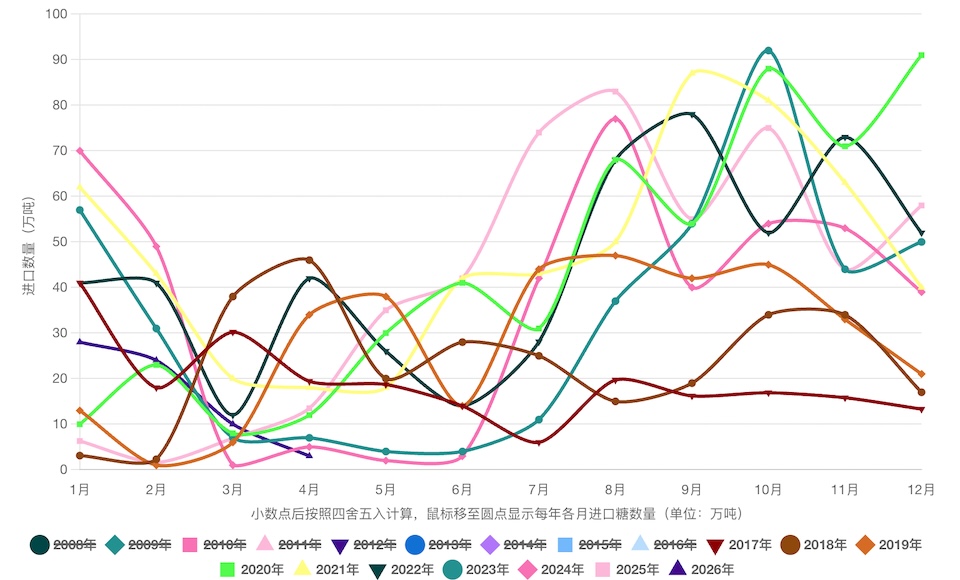

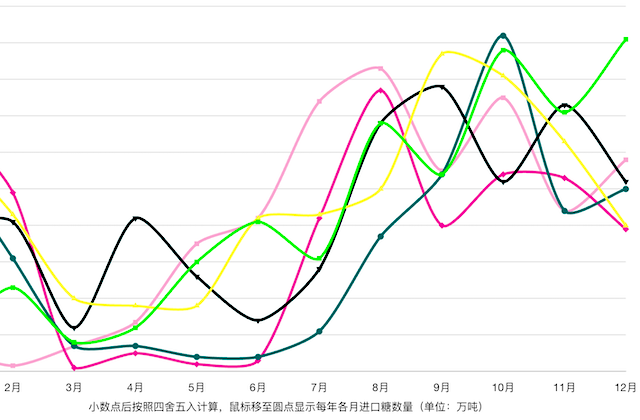

Chart: China monthly sugar import volume, 2025