1. The Big Picture: From Tight to Loose — A Market in Transition

On April 9, the Market Early Warning Expert Committee of China published its latest sugar supply and demand balance sheet and accompanying analysis. The data points to a decisive shift in China’s 2025/26 sugar marketing year: the market is moving from “production falling short of demand” to a phase of “structural oversupply.”

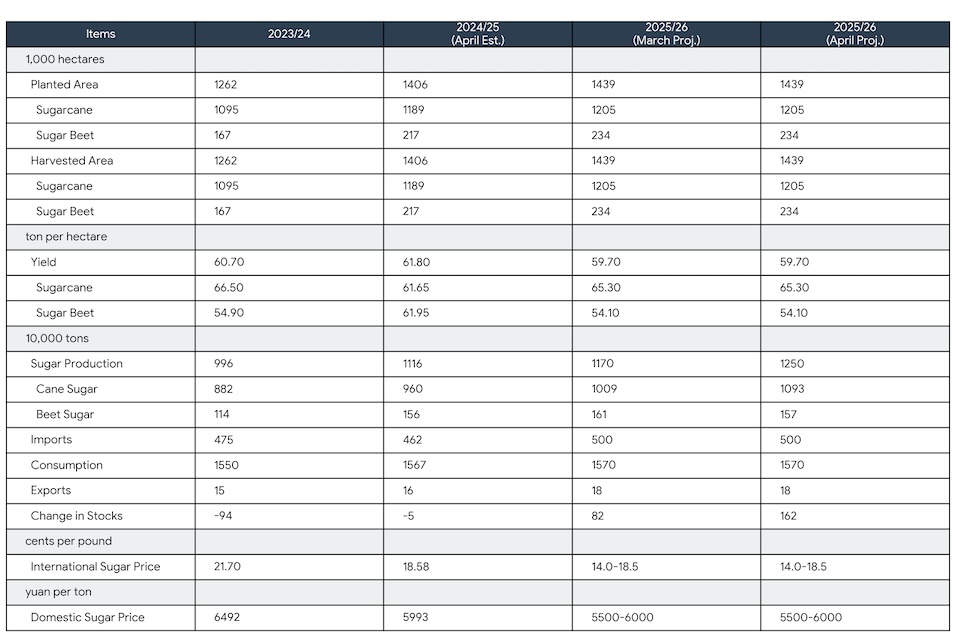

The April forecast projects the 2025/26 ending stock change at +1.62 million metric tons (MMT), a sharp upward revision of 0.80 MMT from the +0.82 MMT projected in March, and a striking reversal from the -0.94 MMT deficit recorded in 2023/24.

The message is clear: China’s domestic sugar supply is transitioning into a period of meaningful surplus.

2. Supply Side: Acreage Expansion and a Confirmed Production Uptrend

Planted Area Continues to Grow

Total sugar crop planted area for 2025/26 is estimated at 1.439 million hectares, up 14.0% from 1.262 million hectares in 2023/24 and up 2.3% from 1.406 million hectares in 2024/25.

| Crop | 2023/24 | 2024/25 (Est.) | 2025/26 (Apr. Fcst.) | Change vs. 2023/24 |

|---|---|---|---|---|

| Sugarcane | 1,095 | 1,189 | 1,205 | +10.0% |

| Sugar beet | 167 | 217 | 234 | +40.1% |

| Total | 1,262 | 1,406 | 1,439 | +14.0% |

Unit: 1,000 hectares

The dramatic expansion in sugar beet acreage — concentrated in Inner Mongolia and Xinjiang — reflects a surge in planting enthusiasm among northern farmers, closely linked to improved grower returns driven by elevated sugar prices over the prior two seasons.

The Headline: Production Forecast Raised by 800,000 Tons

The most significant revision in this month’s report is the production upgrade. The 2025/26 sugar output forecast was raised to 12.50 MMT, up 0.80 MMT (6.8%) from the March projection of 11.70 MMT.

The increase is primarily driven by better-than-expected sugarcane crop performance in Guangxi and Yunnan, where growing conditions have been favorable and sugar extraction rates are running at historically high levels, pushing output well above earlier expectations.

Crushing season data through the end of March from the key producing regions confirms this trend:

- Guangxi — China’s largest sugar-producing province — reported cumulative output of 7.407 MMT, up 14.65% year-on-year, with strong production momentum continuing.

- Yunnan reported cumulative output of 2.134 MMT, up 6.25% year-on-year, showing steady gains.

- Northern beet sugar factories have all completed their processing campaigns, with output at normal levels. Inner Mongolia produced 0.685 MMT and Xinjiang approximately 0.79 MMT.

Breaking down the revision by sugar type: cane sugar output was raised from 10.09 MMT to 10.93 MMT — an increase of 0.84 MMT and the primary source of the upgrade — while beet sugar was trimmed slightly from 1.61 MMT to 1.57 MMT, a reduction of 0.04 MMT.

One note of caution: beet sugar yield is forecast at 54.10 t/ha for 2025/26, a notable 12.7% decline from 61.95 t/ha in 2024/25. While the 2025/26 season output from Inner Mongolia and Xinjiang combined reached a normal level of approximately 1.48 MMT, the underlying cause of the yield decline warrants monitoring.

Stepping back to look at the broader trajectory, China’s sugar production has jumped from 9.96 MMT in 2023/24 to a projected 12.50 MMT in 2025/26 — an increase of 2.54 MMT, or 25.5%, in just two crop years. The recovery in domestic production is unmistakable.

3. Demand Side: Flat Consumption, Imports Holding Steady

Consumption Growth Has Stalled

Domestic sugar consumption for 2025/26 is projected at 15.70 MMT, unchanged from the March forecast and essentially flat versus 15.67 MMT in 2024/25 — an increase of just 30,000 tons, or less than 0.2%. The slowdown reflects both macroeconomic headwinds and continued substitution pressure from high-fructose corn syrup (HFCS) and other starch-based sweeteners eroding white sugar’s share of the sweetener market.

Imports Remain Elevated

The 2025/26 import forecast holds at 5.0 MMT, consistent with the March estimate. Despite the substantial domestic production increase, China’s sugar import dependency remains considerable. Calculated on a “production + imports” basis, import reliance stands at approximately 28.6% (5.0 ÷ 17.5), down from 32.3% (4.75 ÷ 14.71) in 2023/24 — an improvement, but still high by global standards.

Exports Remain Negligible

Export volume is steady at 180,000 metric tons, a marginal factor in the overall balance.

4. Stocks & Balance: Inventory Pressure Building Rapidly

The evolution of ending stock changes tells a clear story of a market passing through a turning point:

| Marketing Year | Ending Stock Change (MMT) |

|---|---|

| 2023/24 | -0.94 |

| 2024/25 (Est.) | -0.05 |

| 2025/26 (Apr. Fcst.) | +1.62 |

The market was actively destocking in 2023/24, reached near-equilibrium in 2024/25, and is now poised for a significant inventory build in 2025/26. The April projection has nearly doubled from the March estimate of +0.82 MMT to +1.62 MMT. An annual surplus of 1.62 MMT implies a substantial rebuild of commercial stocks, representing a meaningful headwind for sugar prices.

5. Price Outlook: Downward Pressure on Both Domestic and Global Prices

International Sugar Prices

International sugar prices have declined from 21.70 US cents/lb in 2023/24 to 18.58 cents/lb in 2024/25. The forecast range for 2025/26 is 14.0–18.5 cents/lb, with the center of gravity shifting notably lower.

The primary driver of international price weakness is the production recovery across major global origins — Brazil, India, and Thailand — tipping the global balance into surplus.

Domestic Sugar Prices

Domestic sugar prices have fallen from 6,492 CNY/ton in 2023/24 to 5,993 CNY/ton in 2024/25. The forecast range for 2025/26 is 5,500–6,000 CNY/ton, representing a further decline.

Against the backdrop of sharply higher domestic output and rising inventories, downward price pressure is considerable. And the market is already reflecting this reality: as of April 9, first-grade white sugar ex-factory prices at mills in certain remote areas of Yunnan and Xinjiang had fallen to approximately 5,000 CNY/ton.

6. ynsugar Note

The April forecast sends an unambiguous signal: China’s domestic sugar market is shifting from shortage to surplus. A projected surplus of 1.62 MMT for 2025/26 represents one of the highest levels in recent years.

Favorable cane crop conditions and historically strong sugar recovery rates in Guangxi and Yunnan have translated into actual production data — through the end of March — that fully validates the bullish supply outlook.

With the global sugar market softening in tandem and domestic production surging, a downward shift in the sugar price center of gravity appears highly probable.

All participants along the supply chain should prepare accordingly. Mills need to manage their sales pacing carefully. Traders should control inventory exposure. And at the policy level, authorities face the delicate task of balancing farmer income protection with market stability.

Note: Data sourced from the publicly released reports of the Market Early Warning Expert Committee