Brazil has long held an unrivaled position in the global sugar trade, and the 2025/26 season has only reinforced that dominance. Blessed with flat, fertile land, a climate tailor-made for sugarcane, and the unique distinction of being the only country capable of running a biannual cane harvest and crushing cycle, Brazil continues to set the benchmark for efficiency, scale, and policy coordination in the sweetener industry.

This article takes a closer look at how Brazil’s sugar sector actually operates,from field to mill to policy desk,and what makes its cost structure the envy of every other producing nation.

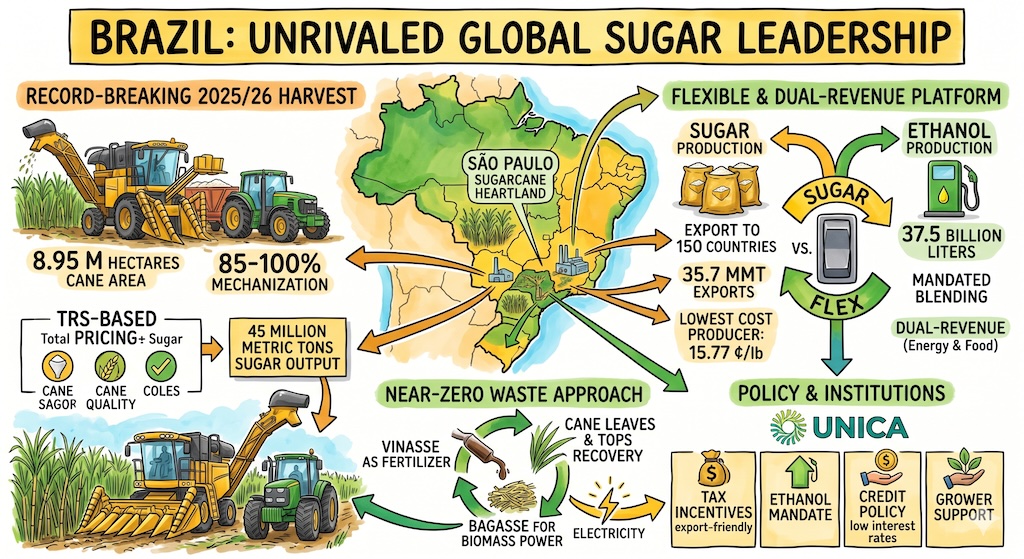

A Record-Breaking 2025/26 Harvest

The 2025/26 marketing year (April 2025 through March 2026) cemented Brazil’s grip on global sugar supply. Brazil’s government forecasting agency, Conab, raised its 2025-26 sugar output forecast to 45 million metric tons, pushing the country’s share of global production well past a quarter of the total. The country exported an estimated 35.7 million metric tonnes to 150 countries across six continents, earning around $14 billion in foreign exchange from sugar alone.

The geography behind those numbers is striking. São Paulo state — where roughly 52 to 60 percent of Brazil’s sugar is produced — sits between 20 and 24 degrees south latitude, with a climate that provides abundant sunshine during the growing season, sufficient rainfall for cane development, and a distinct dry season from April to November that is ideal for harvesting and crushing.That dry window is more than a weather footnote: dry weather during harvest increases the sucrose content of the cane (measured as ATR — Total Recoverable Sugar per tonne of cane) and reduces mechanical harvesting difficulties.

Mechanization at Near-Total Scale

One of the quiet revolutions in Brazilian agriculture has been the steady consolidation of cane farming. The traditional model—thousands of independent growers each selling into local mills—has given way to an industrial-scale system in which mill groups dominate the supply chain. Today, roughly 85% to 100% of cane operations in Brazil are mechanized, with planting and harvesting being the last holdouts to fully automate.

For the 2025/26 season, Brazil’s harvested cane area reached approximately 8.95 million hectares. This scale, combined with mechanization, has transformed productivity. Labor output has climbed, production cycles have smoothed, and the boom-and-bust swings that plague less developed sugar industries have been noticeably dampened. The result: lower unit costs, steadier returns for growers, and reliable feedstock volumes for refiners.

Quality-Based Pricing: TRS Sets the Standard

Brazil doesn’t pay for cane by the ton—it pays by the sugar inside it. The country’s pricing framework is anchored on Total Recoverable Sugar (TRS), which rewards growers for higher-quality cane rather than bulk volume. Layered on top of TRS are adjustments for domestic and international prices of both sugar and ethanol.

This mechanism produces two outcomes Western agricultural economists would quickly recognize: it aligns grower incentives with downstream quality, and it forces planted area to adjust dynamically to world prices. It also gives Brazil a shock absorber the rest of the world lacks—the ability to swing cane between sugar and ethanol depending on which is more profitable.

That flexibility was on full display in 2025/26. In a typical season, a Centre-South mill will allocate somewhere between 45 and 55 percent of its cane to sugar production and the remainder to ethanol. The 2025/26 season saw this ratio at approximately 51 percent sugar — slightly above historical norms, driven by relatively favourable international sugar prices compared to domestic ethanol returns at the start of the season.Brazilian ethanol output for the season came in at roughly 37.5 billion liters, a reminder that the country’s mills are effectively dual-revenue energy-and-food platforms.

This flexibility means that global sugar supply from Brazil is not fixed by harvest size alone — it is also determined by the sugar-ethanol margin at any given point in the season. In summary: when crude oil prices are high enough to make ethanol competitive, Brazil’s effective sugar export volume falls even if the cane harvest is large. When crude is low — as in Q1 2026, with WTI around $62 to $66 per barrel — more cane flows to sugar.

The World’s Lowest-Cost Sugar Producer

According to calculations by the consultancy Pecege, the average production cost for raw sugar FOB Santos Port for the 2025/26 season is estimated at 15.77 cents per pound.

No sugar-producing country can match Brazil on cost. The economics break down into two main buckets: mill-level processing costs (equipment depreciation, labor, taxes, logistics) and raw material costs, with cane consistently the largest single line item.

What keeps the cane bill in check is vertical integration. Brazilian sugar operations typically control cane supply through three channels: roughly 30% comes from company-owned, company-managed plantations paired directly with mills and ethanol distilleries; about 40% comes from cane grown on leased land; and the remaining 30% comes from third-party grower contracts. Owning a sizable share of their own plantations gives sugar companies a price anchor and a guaranteed supply floor—something independent refiners elsewhere in the world simply don’t have.

On the factory floor, Brazilian mills lean heavily on automation. Plant-wide networked control systems monitor equipment in real time, allowing operators to run larger units with leaner staffing. Continuous crystallization equipment has replaced traditional batch pans, shrinking building footprints, cutting labor requirements, and reducing energy use. Combine that with near-total field mechanization and remote crop monitoring, and the cost advantages compound at every stage.

Turning Byproducts Into Profit Centers

If there’s one area where Brazil deserves particular study, it’s its near-zero-waste approach to cane. Vinasse—the liquid residue left over after ethanol fermentation—is returned to cane fields as fertilizer. Rich in minerals and organic matter, it reduces synthetic fertilizer use, boosts cane growth, eliminates a potential water pollution stream, and lowers input costs all at once. Cane leaves and tops are also returned to the soil at essentially 100% recovery. Combined with vinasse application, this practice improves soil moisture retention and strengthens the cane’s drought resilience—an increasingly valuable trait as climate volatility intensifies.

Brazil’s ethanol story itself dates back to the first oil crisis of the 1970s, when the country pioneered large-scale fuel ethanol production. It remains the world’s second-largest fuel ethanol producer, and roughly half of the annual cane crop flows into ethanol rather than sugar. Bagasse—the fibrous residue after cane is pressed—feeds biomass power plants, generating renewable electricity that powers the mills themselves and often feeds surplus power back to the grid.

Policy, Institutions, and the State’s Guiding Hand

Brazil’s industry didn’t get here by market forces alone. Institutional scaffolding has been central from the start. The Brazilian Sugar and Alcohol Institute, established in 1933, served as the original regulatory body coordinating sugar and ethanol production. In 1997, the Brazilian Sugarcane Industry Association (UNICA) was founded; today it’s the country’s largest organization representing sugar, ethanol, and bioenergy interests and plays a leading role in consolidation and advocacy.

Four policy levers stand out:

Differentiated cane taxation. State governments don’t tax cane grown within their borders, but cane brought in from other states attracts a levy of more than 9%. Domestic sugar sales carry a 12% turnover tax, while exports are tax-free—a clear pro-export tilt that helps explain why Brazil ships so aggressively.

Mandated ethanol blending. The federal government sets the ethanol-gasoline blend ratio, and mills are required to allocate at least 15% of output to ethanol. Above that floor, they’re free to optimize the sugar/ethanol mix based on market economics.

Grower insurance and subsidy programs. Dedicated support schemes for cane farmers provide a safety net against weather and price shocks, with subsidy rules clearly codified.

Agricultural credit policy. Commercial banks are required to direct at least a quarter of deposits into agricultural lending, with interest rates held below commercial benchmarks. For capital-intensive cane operations, this cheap credit is a quiet but significant competitive edge.

| Policy Lever | Mechanism | Strategic Impact |

| Tax Incentives | 0% tax on intra-state cane; 0% tax on exports | Massive pro-export bias |

| Ethanol Mandate | Mandatory gasoline blending (min 15% ethanol) | Guaranteed domestic demand floor |

| Credit Policy | 25% of bank deposits directed to ag-lending | Lower interest rates for mill expansion |

| TRS Pricing | Payments based on sugar content, not cane weight | Aligns grower incentives with mill quality |

Looking Ahead to 2026/27

The 2026/27 outlook suggests a modest pullback. Datagro estimated CS production for 2026/27 at approximately 43.2 MMT — a modest reduction from 2025/26, primarily due to expected lower sugarcane yields after the 2024 drought and wildfire damage that reduced ratoon cane quality.Mills are recalibrating their production mix, downgrading the sugar allocation ratio in favour of ethanol to capture premiums driven by elevated energy prices. The strategic shift takes effect for the 2026/27 season commencing in April.

For global buyers, the takeaway is clear: Brazil’s sugar machine isn’t just large—it’s structurally flexible, vertically integrated, and backed by coherent policy. Those attributes are what keep it at the top of the export league year after year, and they’re the reason any serious student of commodity markets needs to understand how the Brazilian model actually works.

🎯 Destination Analysis: China, as the world’s largest sugar importer, is the primary destination for this cost advantage — explore the full infrastructure picture in our China sugar import report.