Headline Numbers

China’s refined sugar industry kicked off 2026 with a striking production surge. According to the latest data from the National Bureau of Statistics, refined sugar output reached 3.125 million metric tons in March 2026, up 79.9% year-on-year. Cumulative Q1 production (January–March) totaled 9.884 million tons, a 26.6% increase compared with the same period last year.

This marks one of the strongest first-quarter performances in recent memory and signals a robust recovery in China’s sweetener supply chain.

2003–2026 China Refined Sugar Production – Annual Statistics

Why the Sharp Increase?

The Q1 jump is not simply a matter of stronger demand—it reflects a combination of seasonal timing, agricultural conditions, and global price dynamics:

1. Delayed start to the 2025/26 crushing season. The new crushing season officially began in November 2025, but sugar mills in the key producing regions of Guangxi and Yunnan largely postponed opening their operations. This pushed peak production activity into February and March, mechanically inflating Q1 output figures compared to the prior year.

2. Higher cane yields. Sugarcane output improved in several growing regions this season, providing mills with more feedstock. This aligns with broader industry expectations—MY 2025/26 cane acreage was expected to expand in Guangxi, China’s largest sugar producing area, largely because margins were higher compared to competition crops such as fruits, which have been less profitable due to weak market demand.

3. A surge in imported sugar processing. A crucial nuance often missed by overseas observers: China’s official “refined sugar” statistic covers large industrial enterprises with annual revenues above RMB 20 million and includes both domestically produced sugar and imported raw sugar that is refined onshore. Since late 2025, international sugar prices have collapsed to five-year lows, reopening the import arbitrage window. Q1 2026 sugar imports reached 620,000 tons—a staggering 320% year-on-year increase—and much of this volume flowed directly into Chinese refineries.

This import surge is consistent with global market signals. which reached a five-year low.

The Crushing Season Winds Down

As the calendar turned to late March, Guangxi and Yunnan entered their end-of-season phase. As of April 20, approximately 90% of Guangxi’s sugar mills had completed crushing operations, marking the effective close of the domestic production cycle. From this point forward, monthly refined sugar output will shift toward processed imports and residual beet sugar production.

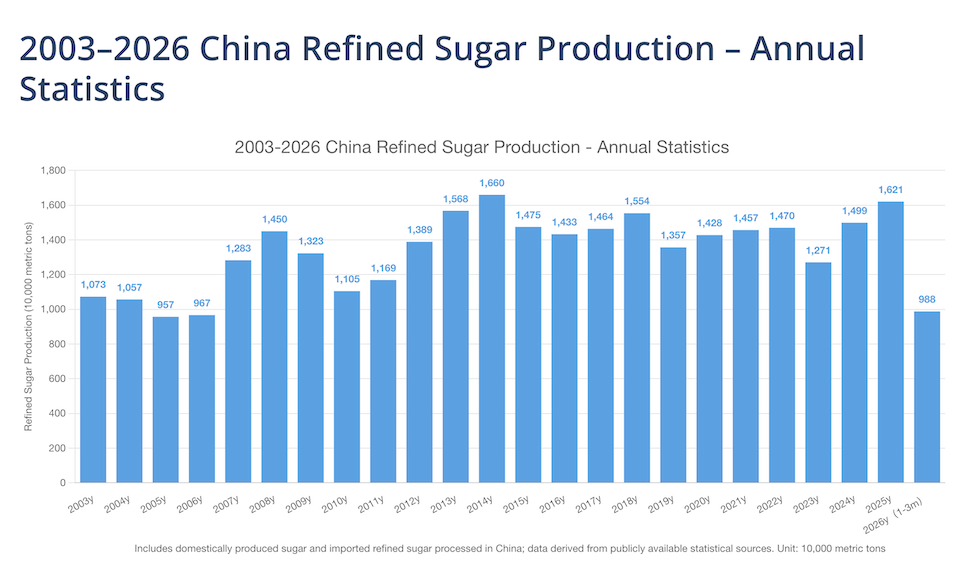

Putting 2025 in Historical Context

The 2026 rebound follows what was already a strong 2025. Full-year refined sugar production in 2025 reached 16.21 million tons, up 9.0% year-on-year and marking the second-highest annual output on record—trailing only the 2014 peak of 16.60 million tons.

The long-term chart reveals a clear structural pattern:

- 2003–2006: Output ranged between 9.57 and 10.73 million tons

- 2007–2011: A transition phase, fluctuating between 11.05 and 14.50 million tons

- 2012–present: Annual production has consistently exceeded 13 million tons, peaking above 16 million tons

- 2023 trough: Output dipped to 12.71 million tons due to weather-related cane shortfalls

- 2024–2025 recovery: A sharp rebound to 14.99 million and then 16.21 million tons

Implications for Global Markets

China remains a pivotal player in global sugar trade. As the world’s second-largest sugar consumer with annual consumption around 15 million tons and the third-largest producer at 11 million tons of pure sugar, China’s fundamental deficit between domestic consumption and production has established it as a consistent net importer, shaping supply chains and price formation across key producing regions from Southeast Asia to South America.

For international traders, three takeaways stand out:

- Refined sugar production growth ≠ domestic cane surge alone. A meaningful portion of the Q1 increase reflects refined imports being processed by Chinese mills, not a fundamental expansion of domestic sucrose supply.

- Import appetite remains robust. With MY 2025/26 China’s sugar imports forecast at 5.3 million tons and prices remaining relatively low, supporting continued sugar imports, Brazilian and Thai exporters will continue to find strong demand from Chinese buyers.

- Global surplus context. The International Sugar Organization forecasts the 2025/26 global sugar market will remain in surplus by 1.625 million tons, with global production rising to 181.767 million tons—5.552 million tons more than the previous season—driven mainly by India, Thailand, and Pakistan. This surplus is helping keep prices attractive for Chinese importers.

Looking Ahead

With the domestic crushing season now largely complete and China’s 2025 production hitting a near-record high, the key question for the remainder of 2026 is whether global sugar prices stay low enough to sustain the import-driven refining boom. If raw sugar remains near five-year lows, expect China’s monthly refined sugar output to continue outpacing historical norms—even after domestic cane supply is exhausted for the season.

For Western analysts and traders, the Q1 2026 data should be read carefully: the headline 26.6% growth is impressive, but it is driven as much by global price arbitrage and seasonal timing shifts as by any structural expansion of Chinese sugar production itself.

Disclaimer: The information and analytical data contained in this report are provided by the ynsugar.com editorial team for informational and educational purposes only. While we strive for maximum data precision, ynsugar.com makes no warranties regarding the absolute accuracy or completeness of the information. The commodity market is subject to high volatility; therefore, the insights provided herein do not constitute financial, investment, or trading advice. Any actions taken based on this report are at the sole risk of the user.