The latest data for Thailand Sugar Production 2025-26 has been officially released as the sugarcane crushing season wrapped up on May 3, 2026. According to the final report by…

Thailand has officially wrapped up its 2025/26 sugarcane crushing season, delivering production numbers that are drawing significant attention across the global sugar market. According to the final official report released by Thailand’s Office of the Cane and Sugar Board (OCSB), milling operations concluded on May 3, 2026. The results point to the country’s strongest production recovery in the past three seasons, rebounding sharply from recent drought-induced lows.

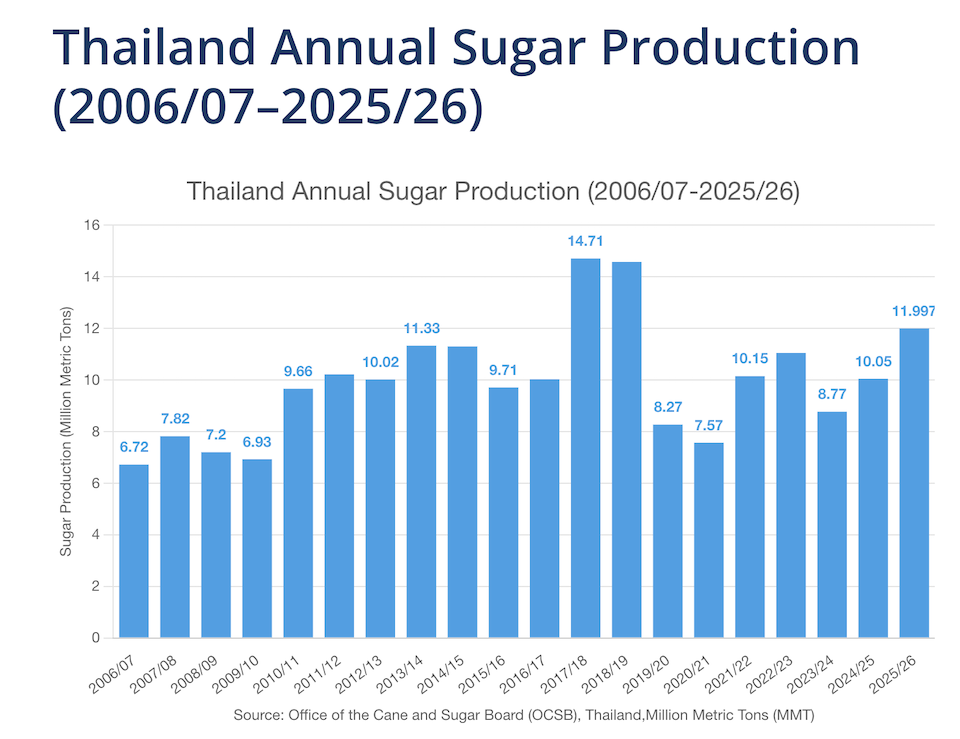

📊 Season-End Production Data

The headline figures from the OCSB tell a compelling story of both volume growth and significantly improved cane quality for the 2025/26 crop:

-

Total Cane Crushed: 105.86 million metric tons (MT), an increase of 13.82 million MT (+15.01%) year-on-year.

-

Commercial Cane Sugar (CCS): 12.94%, up 0.33 percentage points from the prior season.

-

Average Sugar Extraction Rate: 11.333%, up 0.414 percentage points year-on-year.

-

Total Sugar Production: 11.997 million metric tons (MT), up 1.946 million MT (+19.37%) compared to the 2024/25 season.

Breakdown by Sugar Type:

-

Raw Sugar: 9.1645 million MT

-

Plantation White Sugar: 2.3585 million MT

-

Refined Sugar: 0.4739 million MT

Market Note: Raw sugar continues to dominate Thailand’s output mix. This structure aligns with the nation’s export-oriented refining capabilities and its established role as the primary supplier to regional toll-refiners across Asia.

📈 Why the Numbers Matter: Quality and Yield Gains

The concurrent improvement in both CCS and the sugar extraction rate is a highly positive indicator for the industry. Higher sugar content means mills process more sugar per ton of sugarcane, a metric that directly boosts profitability for both sugarcane farmers and mill operators.

A 0.414-percentage-point jump in extraction efficiency applied across a massive crushing volume of over 105 million MT translates into hundreds of thousands of additional tons of sugar—achieved without expanding physical planting acreage.

Agronomic experts attribute this year’s success to a combination of three core factors:

-

Favorable Weather: Improved and well-distributed rainfall during the critical elongation phase, particularly in major producing regions like Khon Kaen, Nakhon Ratchasima, and Kanchanaburi.

-

Varietal Management: Wider adoption of high-yield, drought-resistant cane varieties.

-

Harvest Logistics: More disciplined and timely harvesting schedules implemented by millers and farmers to minimize post-harvest sucrose inversion.

🌐 Thailand’s Position in the Global Sugar Market

To contextually frame this season’s performance: during the previous 2024/25 cycle, Thailand maintained its position as the world’s second-largest sugar exporter, trailing only Brazil. Thai sugar exports reached approximately 5.5 million MT, generating over USD 2.6 billion in export revenue. With the 2025/26 production climbing close to the 12 million MT mark, Thailand is well-positioned to expand its export allocations in the coming months.

This supply surge arrives at a critical juncture for global trade flows:

-

Brazil’s Dynamics: While Brazil’s 2025/26 Center-South crushing season is underway, global buyers are closely monitoring alternative origins to hedge risks.

-

Indian Export Policy: Continued restrictions on sugar exports from India leave a structural deficit in international markets, opening a clear window for Thai-origin sugar to supply key premium destination markets including Indonesia, China, South Korea, and the Middle East.

🔍 Key Factors to Watch Going Forward

As the Thai industry transitions from production to marketing, several key wildcards will dictate the ultimate global market impact:

-

Export Logistics & Pace: Whether Thai ports (primarily Laem Chabang and Map Ta Phut) can maintain efficient bulk and container loading paces to handle the increased surplus.

-

Global Price Pressure: The influx of Thai supply could cap potential upside rallies in New York No. 11 raw sugar futures, depending on the final numbers out of Brazil’s Center-South.

-

Domestic Allocation (Quotas): The Thai government’s regulatory split between domestic consumption quotas (Quota A) and export allocations (Quota B and C) will dictate the exact volume accessible to international trade houses.

-

Regional Competition: Any potential policy shift from New Delhi regarding Indian sugar exports later in the year could trigger direct price competition with Thai sugar for Asian market share.

🗃️ Data Source

All production and milling statistics cited in this report are verified and sourced directly from the Office of the Cane and Sugar Board (OCSB), Ministry of Industry, Thailand, issued at the official conclusion of the 2025/26 crushing season.

Disclaimer: The information and analysis contained in this article are based on official data provided by the Office of the Cane and Sugar Board (OCSB) of Thailand and are intended solely for informational and educational purposes. This content does not constitute financial, investment, or commercial advice. While we strive to ensure the accuracy and reliability of the data presented, ynsugar.com makes no representations or warranties of any kind, express or implied, about the completeness or suitability of the information for any specific trading or business decisions. Readers are advised to verify all market data independently before taking action.