Five Consecutive Seasons of Growth Put Vietnam on the Map as ASEAN’s Most Productive Sugar Sector

A Tropical Sweet Spot for Sugarcane

Vietnam, situated at the heart of Southeast Asia between latitudes 8°30’N and 23°22’N, possesses natural conditions that are exceptionally favorable for sugarcane cultivation. Abundant sunshine, high average temperatures, and fertile soils across its central and southern provinces allow sugarcane to flower and set seed naturally — a trait that makes the country an ideal environment for sugarcane cross-breeding and varietal improvement. Sugarcane is one of the most important industrial crops in Vietnam, and the sugar sector has historically been second only to food grain production in Vietnam’s agricultural economy.

Vietnamese sugarcane follows two distinct planting windows: autumn planting (September–November) and winter-spring planting (December–March), with harvesting and crushing typically running from November through March each year. The government has designated key sugarcane zones in provinces such as Thanh Hoa, Quang Ngai, and Tay Ninh, where large-scale mills have been built to anchor the industry.

A Dramatic Turnaround: From Crisis to Consecutive Growth

Vietnam’s sugar industry has undergone a striking transformation since 2021. The industry’s recovery and significant growth began after Vietnam implemented trade defense measures in 2021.The anti-dumping and anti-subsidy duties imposed on sugar imports from Thailand gave domestic producers critical breathing room.

These innovations have enabled sugar production to increase nationwide for four consecutive years, with sugarcane output rising by 166% and sugar production by 161%.The turnaround is reflected vividly in the season-by-season numbers reported by the Vietnam Sugarcane and Sugar Association (VSSA):

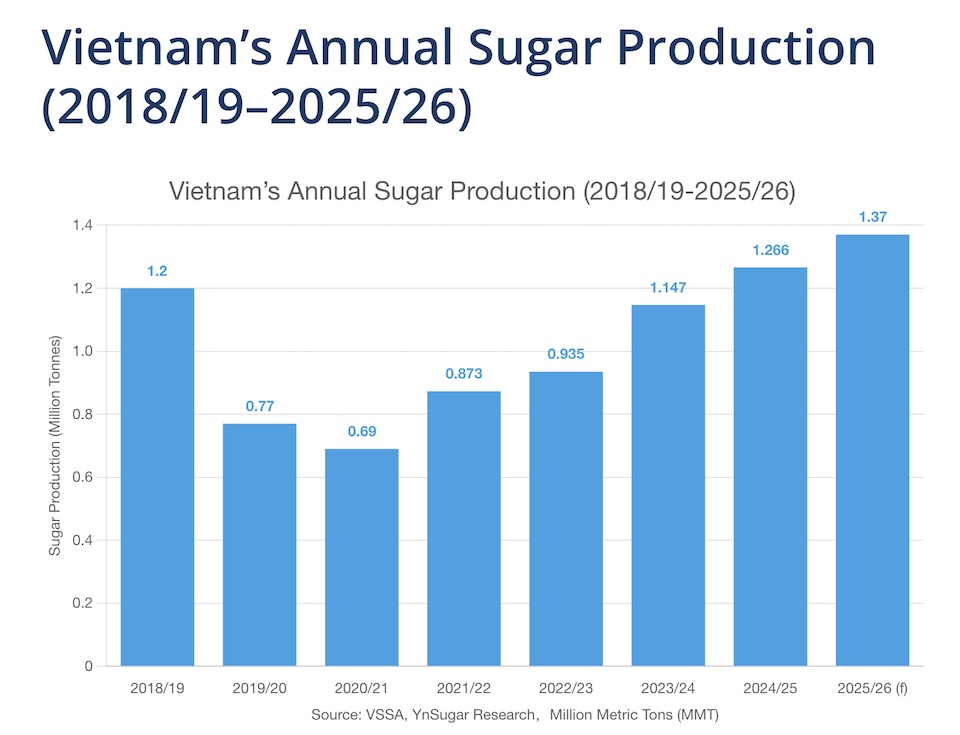

2022/23 season: According to VSSA data, the industry crushed approximately 9.5 million tonnes of sugarcane and produced around 935,000 tonnes of sugar — already a sign of recovery from the nadir of 2020/21, when output was just 763,000 tonnes.

2023/24 season: By the end of the 2023–2024 crushing season, Vietnam’s sugar industry had crushed 11,204,789 tons of sugarcane and produced 1,107,777 tons of sugar of various types. Compared to the 2022–2023 season, sugarcane output reached 117.9%, while sugar production achieved 118.4%.

2024/25 season: Vietnam’s mills had completed crushing by June, producing more than 1.266 million tonnes of sugar, an increase of 14.2% compared with the previous season.Total harvested cane area for the 2024–2025 season reached 189,360 hectares, up from 163,019 hectares in the previous one.Cane output was nearly 12.429 million tonnes, up from about 11.205 million tonnes posted the year before.

2025/26 season (forecast): For the 2025–2026 crop, the association expects 25 mills to remain in operation, the same number as last season, with a combined design capacity of 124,000 tonnes of cane per day.Output is projected at more than 13.34 million tonnes of cane and over 1.37 million tonnes of sugar, representing an 8.24% increase year-on-year.

ASEAN’s Productivity Leader

While Vietnam is not ASEAN’s largest sugar producer by volume — that distinction belongs to Thailand, which produces over 10 million tonnes annually — it has earned a different accolade. Vietnam’s sugar productivity reached 6.69 tons per hectare in the 2024/2025 crop, the highest in ASEAN and ahead of Thailand, Indonesia, and the Philippines.In the prior season, Vietnam’s sugar yield for the 2023–2024 crop reached 6.79 tonnes per hectare, higher than other key producers in the region.

This achievement is largely driven by mechanization and modern agronomy. According to the VSSA, the mechanisation rate for land preparation has surpassed 90 per cent.Through technology transfer cooperation programmes and international funding, some sugar companies have started experimenting with new Industry 4.0 solutions from countries like the US and Australia to digitise the management of sugar mills.Additionally, the Sugarcane Research Institute has introduced 23 new lines, including 12 Vietnamese hybrids and eight imported varieties which are being tested across various ecological regions.

Structural Challenges Remain

Despite impressive production growth, Vietnam’s sugar sector faces deep structural constraints. Raw material supply remains the primary bottleneck: many mills operate at only 60%–80% of their designed crushing capacity due to insufficient sugarcane supply. The national average sugar content of cane remains relatively low at around 10.2%, though high-yield areas can reach 13.6% while underperforming regions drop as low as 8.5%.

The industry has also undergone significant consolidation. Due to many recent factors such as the effectiveness of the ASEAN Trade in Goods Agreement (ATIGA) and the influence of the COVID-19 pandemic, the number of sugar mills dropped significantly from 38 to 29 in 2019/2020 and finally dropped to 25 in 2020/2021. As of 2025, Vietnam has approximately 25–30 operational sugar mills, a significant declinefrom over 40 at the industry’s peak. The surviving mills are predominantly joint ventures or foreign-invested enterprises with modern equipment and stable raw material zones.

Sugar Smuggling: A Bitter Pill

The industry’s recovery remains incomplete due to the persistent problem of sugar smuggling. In the 2023–2024 crop year, many acts of trade fraud related to smuggled sugar from Laos and Thailand to Vietnam have been detected by authorities in many provinces and cities across the country. In the 2024/25 season, the oversupply crisis deepened dramatically: the industry processed over 12.68 million tons of sugarcane, producing more than 1.25 million tons of sugar. Over 70 percent of this output remains in factory storage — an unprecedented level.

Consumer trends are shifting increasingly towards the use of high-fructose corn syrup (HFCS), which has significantly weakened market demand.This combination of smuggled sugar, rising HFCS competition, and record inventories has created what VSSA Chairman Nguyen Van Loc described as a market saturation crisis, with some factories forced to sell below production cost.

Rising Farm Incomes Offer Hope

On the farmer side, the picture is more positive. The purchase price for sugarcane from farmers has risen continuously, up by 152% compared to the 2019/2020 crop.Since the beginning of 2025, sugarcane prices have remained high, with factories offering up to VND1.23 million (US$48) per ton. When additional costs are factored in, the price can reach VND1.33 million per ton — the highest level recorded since 2018.The industry provided livelihoods for over 225,000 farming households.

Ynsugar Outlook

Vietnam’s sugar industry has staged an undeniable comeback after years of existential pressure from cheap ASEAN imports and the COVID-19 pandemic. The country now boasts the highest sugar productivity in the region, expanding cultivation areas, and rising farmer incomes. However, the path forward is far from sweet: the La Niña phenomenon could cause prolonged rainfall and flooding in 2025, negatively affecting sugarcane production, particularly in northern and central regions.Tackling smuggling, managing HFCS substitution, and improving cane sugar content will be decisive in determining whether Vietnam’s sugar recovery is durable — or merely a temporary reprieve.