May 2026 — China refined sugar production has recorded strong growth in the early months of 2026, driven by a highly concentrated crushing peak and a surge in domestic processing of imported raw sugar.

📊Key Highlights

- China’s refined sugar output reached 1.043 million metric tons in April 2026, up 73.3% year-on-year

- Cumulative production for January–April 2026 totaled 10.746 million metric tons, a 28.0% YoY increase

- 2025 full-year output of 16.21 million metric tons marked the second-highest level in history

- Sugar imports jumped 129.2% YoY in the first four months of 2026, fueled by 5-year lows in global sugar prices

Strong Start to 2026: April Output Soars 73.3%

According to the latest data released by China’s National Bureau of Statistics, refined sugar production in April 2026 reached 1.043 million metric tons, representing a remarkable 73.3% year-on-year increase. For the January–April 2026 period, cumulative output totaled 10.746 million metric tons, up 28.0% compared with the same period in 2025 — pointing to a strong growth trajectory in the early months of the year.

These figures cover industrial enterprises above designated size (i.e., those with annual main business revenue exceeding RMB 20 million), and include both domestically produced sugar and imported refined sugar processed within China.

⚙️ Why the Surge? Three Key Market Drivers

1. Delayed Crushing Season Shifts Peak Production into Q1 2026

The 2025/26 crushing season, which began in November 2025, was characterized by widespread delays in mill start-ups across the two largest producing regions — Guangxi and Yunnan provinces. As a result, the production peak was concentrated in February and March 2026, rather than being spread more evenly across the crushing cycle.

As of May 20, 2026:

- Guangxi had completed its crushing season entirely

- Yunnan still had 22 sugar mills continuing operations

2. Higher Cane Sugar Yields in Both Major Producing Regions

Through April 30, 2026, the season-to-date production figures showed strong growth in both leading producing provinces:

| Region | 2025/26 Season Output (through Apr 30) | YoY Change |

|---|---|---|

| Guangxi | 7.6951 million metric tons | +1.2301 million tons |

| Yunnan | 2.7522 million metric tons | Up from 2.3639 million tons in prior season |

3. Surging Imports as Global Sugar Prices Hit 5-Year Lows

Since late 2025, international sugar prices have fallen to their lowest levels in five years, opening up a favorable window for Chinese sugar importers. According to customs data, China imported 650,000 metric tons of sugar during January–April 2026 — a 129.2% year-on-year jump.

This sharp increase in imported raw sugar has translated directly into higher volumes of refined sugar processed domestically, further amplifying the headline production growth figures.

Looking Back: 2025 Was a Near-Record Year

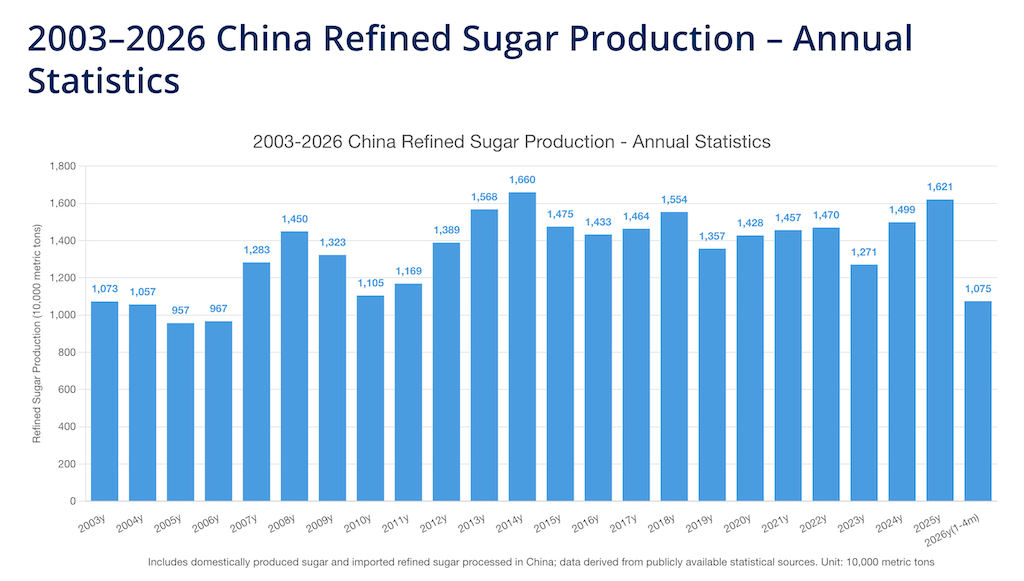

For full-year 2025, China’s total refined sugar production reached 16.21 million metric tons, growing 9.0% year-on-year. This output represents the second-highest annual total on record, trailing only the all-time peak of 16.60 million metric tons set in 2014.

Long-Term Trend: Stable Production Above 13 Million Tons Since 2012

Examining the longer historical picture from the chart data:

- 2003–2006: Output remained below 11 million tons annually, with 2005 marking a low at 9.57 million tons

- 2007–2011: Production climbed steadily from 12.83 million tons to above the 11-million-ton threshold

- 2012 onward: China’s annual refined sugar production has consistently stayed above 13 million metric tons, peaking above 16 million tons in multiple years

- 2014: All-time high of 16.60 million metric tons

- 2023: A cyclical low of 12.71 million metric tons

- 2024–2025: Recovery to 14.99 million and 16.21 million tons respectively

- 2026 (Jan–Apr): Already at 10.75 million tons, suggesting another strong year ahead

After the temporary dip in 2023, production has rebounded sharply and is now firmly back in the high-output operating range that has characterized the Chinese sugar industry over the past decade.

📉 Long-Term Trend Analysis: 2003–2026 Historical Picture

An examination of the historical data since 2003 illustrates the cyclical resilience of China’s refining sector:

+-----------+---------------------------------+----------------------------------------+

| Era | Production Range (Annual) | Key Structural Characteristics |

+-----------+---------------------------------+----------------------------------------+

| 2003–2006 | Below 11 million metric tons | Cyclical low in 2005 at 9.57M tons. |

| 2007–2011 | 11 to 14.5 million metric tons | Steady capacity expansions. |

| 2012–2026 | Consistently above 13M tons* | Established high-output operating range|

+-----------+---------------------------------+----------------------------------------+

*Note: Excluding the cyclical trough of 12.71M tons recorded in 2023.

-

The All-Time Peak: Set in 2014 at 16.60 million metric tons.

-

The Recent Recovery: Following the 2023 low, production bounced back to 14.99 million tons in 2024, expanded to 16.21 million tons in 2025, and has already accumulated 10.75 million tons in just the first four months of 2026.

YnSugar Outlook

With the 2025/26 crushing season nearly complete in Guangxi and only a handful of mills still operating in Yunnan, the supply-side momentum from the late-starting season is largely captured in the year-to-date data. Going forward, the key swing factor for monthly production figures will likely be import-driven refining volumes, which remain closely tied to global sugar price trends and the China-international price spread.

If international prices remain at multi-year lows, China’s refined sugar output could continue to outpace historical norms in 2026 — potentially challenging the 2014 all-time record.

Data sources: China National Bureau of Statistics; Production figures cover industrial enterprises with annual main business revenue above RMB 20 million, including both domestic and imported-refined sugar. Unit: 10,000 metric tons unless otherwise stated.