Key Takeaways

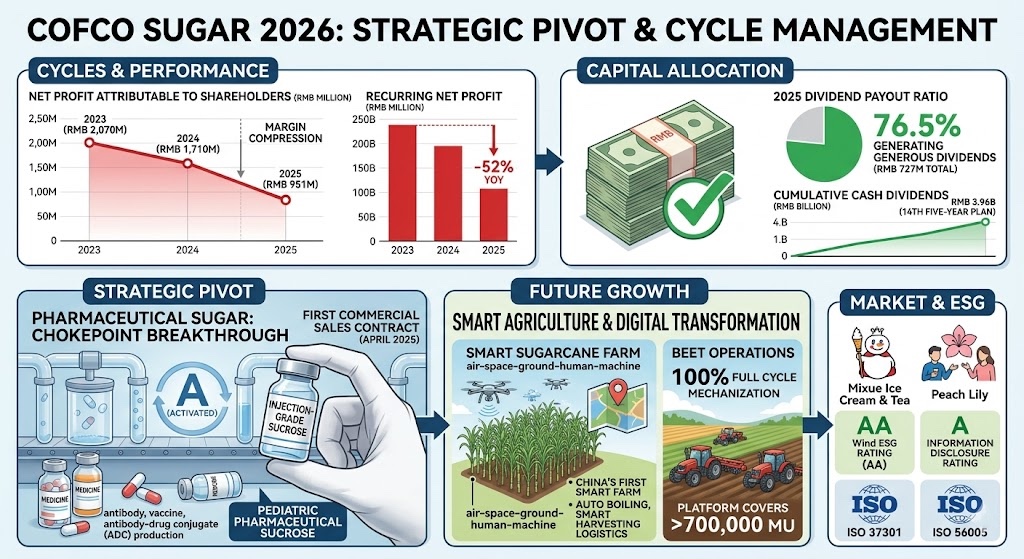

COFCO Sugar Holdings (600737.SH), China’s largest integrated sugar company, reported a sharp earnings decline for fiscal year 2025. Revenue fell 18.4% to RMB 26.5 billion (approximately USD 3.6 billion), while net profit attributable to shareholders dropped 44.5% to RMB 951 million. Despite the downturn, the company maintained a generous 76.5% dividend payout ratio and continued investing in high-value segments — most notably pharmaceutical-grade sugar — that could reshape its earnings profile in future cycles.

Table: COFCO Sugar Key Financial Performance (2023–2025)

| Metric (RMB Billion) | 2025 | 2024 | 2023 | YoY Change (25 vs 24) |

|---|---|---|---|---|

| Revenue | 26.51 | 32.50 | 33.11 | -18.42% |

| Net Profit (Attributable) | 0.95 | 1.71 | 2.07 | -44.48% |

| Recurring Net Profit | 0.81 | 1.69 | 2.10 | -52.02% |

| ROE (%) | 8.24% | 14.44% | 19.42% | -6.20 ppts |

The Numbers: A Cycle in Full Retreat

The headline figures tell a story of an industry moving decisively past peak profitability. After two consecutive years of strong earnings driven by elevated global and domestic sugar prices, 2025 marked a sharp reversal.

Net profit fell from RMB 2.07 billion in 2023 to RMB 1.71 billion in 2024, and then to RMB 951 million in 2025 — a cumulative decline of 54% over two years. The deceleration was even more pronounced on a non-GAAP basis: recurring net profit dropped 52% year-over-year to RMB 812 million, indicating that the core business bore the brunt of the downturn rather than one-off items masking the trend.

What stands out is the margin compression. Revenue declined 18.4%, yet profit before tax fell 42.1%, meaning the drop in sugar prices cut much deeper into profitability than the top-line contraction alone would suggest. This is the classic “operating leverage in reverse” dynamic that characterizes commodity processors — fixed costs in farming, milling, and refining do not flex downward as easily as selling prices do.

Return on equity fell from 14.4% to 8.2%, and earnings per share declined from RMB 0.80 to RMB 0.44. While these metrics remain solidly positive — COFCO Sugar is far from distressed — they represent a meaningful step-down from the elevated returns shareholders had grown accustomed to during the 2023–2024 sugar bull market.

Quarterly earnings reveal a second-half deterioration. Q4 net profit was just RMB 136 million, with recurring net profit of only RMB 70 million — roughly one-fifth of the Q3 figure. Cash flow patterns were equally seasonal: the company burned over RMB 1 billion in operating cash in Q1 (peak procurement season for sugarcane and beet) and nearly RMB 1.9 billion in Q4, offset by strong inflows of RMB 2.1–2.2 billion in Q2 and Q3. This “cash trough – cash peak – cash trough” rhythm is structural to the sugar milling business and should not alarm investors, but it does underscore the working capital intensity of the model.

China’s Sugar Market: Structural Deficit, Policy Complexity

To understand COFCO Sugar’s results, one must first understand the peculiarities of the Chinese sugar market.

China consumes between 15 and 16 million tonnes of sugar annually, making it one of the world’s largest markets. However, domestic production consistently falls short, covering only about 65% of demand. The remaining 35% — roughly 5 million tonnes per year — must be imported. This structural supply deficit means China’s domestic sugar price is perpetually influenced by global benchmarks, trade policy, and currency fluctuations.

Yet unlike most global sugar markets, China’s upstream cost structure is significantly higher. Sugarcane, which accounts for 88% of domestic output, is predominantly grown in Guangxi and Yunnan provinces on hilly terrain that limits mechanization. Government-mandated minimum purchase prices for cane provide income stability for farmers but lock in production costs well above those in Brazil, Thailand, or Australia. The result is a domestic industry that is structurally uncompetitive on cost but shielded by import controls — a policy framework designed to balance food security, rural livelihoods, and consumer affordability.

COFCO Sugar operates across this entire value chain. Its 5 cane mills, 8 beet mills, and 3 refineries give it unmatched domestic scale. Its beet sugar output exceeds 350,000 tonnes annually, making it China’s largest beet sugar producer. Its refining operations handle imported raw sugar, and its trading arm manages domestic distribution and logistics. This vertically integrated model provides some insulation against price swings at any single point in the chain, but it cannot fully offset a broad-based decline in sugar margins — as 2025 demonstrated.

One underappreciated data point from the report: China’s per capita sugar consumption remains below 50% of the global average. The company frames this as long-term upside potential, noting growing public awareness that natural sugar has legitimate nutritional value and that synthetic sweeteners carry their own health risks. Whether this translates into meaningful demand growth will depend on shifting consumer attitudes and regulatory trends around artificial sweeteners — both of which appear to be moving in sugar’s favor, at least directionally.

Refining Operations: Adapting to a Changing Raw Sugar Supply

A significant operational theme in the 2025 report is the challenge posed by diversifying raw sugar import sources. As China broadens its procurement beyond traditional origins, refineries increasingly handle higher-color-value raw sugar that contains more impurities, requires more energy to process, and yields less consistent product quality.

COFCO Sugar’s response has been notably technical. Its Liaoning refinery established a dedicated task force for molasses-washing optimization, substantially increasing daily throughput of high-color-value raws. Its Zhangzhou refinery processed 90,000 tonnes of high-color-value raw sugar in a single campaign for the first time, developing what it describes as an integrated “gradient decolorization – precision crystallization” process that achieved nationally leading steam consumption rates under stable production conditions.

For international observers, this is analogous to the challenge oil refineries face when shifting from light sweet crude to heavier sour grades: it requires capital investment, process innovation, and operational expertise. COFCO Sugar’s ability to handle a wider range of raw sugar qualities at competitive conversion costs represents a genuine competitive moat that is difficult for smaller Chinese refiners to replicate.

The Pharmaceutical Sugar Gambit: Small Volume, Strategic Significance

Perhaps the most forward-looking element of the 2025 report is the progress in pharmaceutical-grade sugar. COFCO Sugar’s injection-grade sucrose production line became fully operational, and the company signed its first commercial sales contract in April 2025. Separately, its proprietary pediatric pharmaceutical sucrose received approval from China’s National Medical Products Administration, achieving “A (Activated)” status for use in marketed drug formulations. The pharmaceutical sugar product portfolio now spans oral-grade to injection-grade, with total volume exceeding 23,000 tonnes.

The strategic significance here extends well beyond the volume. Injection-grade sucrose is a critical excipient in the production of antibodies, vaccines, and other biopharmaceuticals. This has historically been a bottleneck controlled by foreign suppliers — one of the so-called “chokepoint” dependencies that Chinese industrial policy is actively seeking to eliminate. COFCO Sugar’s breakthrough positions it at the intersection of two powerful policy tailwinds: food security and pharmaceutical supply chain sovereignty.

From a financial perspective, pharmaceutical sugar commands unit economics vastly superior to commodity sugar. While 23,000 tonnes is a rounding error relative to the company’s millions of tonnes in sugar trading volume, the margin contribution per tonne is likely multiples higher. If the company can scale this business — and the regulatory approvals suggest the runway is now clear — it could become a meaningful earnings contributor within 3–5 years and a structural re-rating catalyst.

The company also reported initial progress in liquid sugar and natural sweetener businesses, securing five certifications for sucrose-based and natural sweetener products. This diversification into adjacent categories signals an intent to evolve from a pure commodity processor into a broader sweetener solutions provider — a strategic direction that mirrors the evolution of global peers like Südzucker and Tereos.

Digital Transformation and Smart Agriculture: Real Investment, Long Payback

COFCO Sugar’s report devotes considerable space to digitalization and smart farming initiatives. Its sugarcane operations have established China’s first “smart sugarcane farm” with an integrated “air-space-ground-human-machine” digital system. Its beet operations have achieved 100% mechanization across the full production cycle, with smart platforms covering over 700,000 mu (approximately 47,000 hectares) of beet fields.

On the factory floor, the company’s Chongzuo sugar mill independently developed 12 core systems spanning automated sugar boiling, safety management, intelligent boiler combustion, and smart harvesting logistics. This work earned recognition from Guangxi’s Department of Industry and Information Technology, which designated Chongzuo as the pilot unit for the sugar industry’s digital transformation and invited it to help create the sector’s “navigation map” for intelligent upgrading.

These initiatives address the fundamental cost disadvantage of Chinese sugar production relative to global competitors. Brazil’s sugarcane yields benefit from flat terrain, large-scale mechanization, and decades of agricultural R&D. China cannot replicate Brazil’s geography, but it can narrow the productivity gap through precision agriculture, automation, and data-driven decision-making. The payback period on these investments is inherently long, but for an industry where raw material costs typically represent 60–70% of total production costs, even modest yield improvements compound significantly over time.

Capital Allocation: Generous Dividends Signal Discipline

In a year when profits nearly halved, COFCO Sugar’s board proposed a cash dividend of RMB 3.40 per 10 shares (approximately RMB 0.34 per share), totaling RMB 727 million. This represents 76.5% of net profit — a payout ratio that most global sugar companies would consider extremely generous, and one that underscores the company’s commitment to shareholder returns even through the trough of the cycle.

Since the beginning of the “14th Five-Year Plan” period, the company has distributed cumulative cash dividends of RMB 3.96 billion (excluding the proposed 2025 distribution). For its controlling shareholder, COFCO Group — a state-owned enterprise under SASAC holding 50.73% of shares — this translates to reliable cash upstream flows that support the parent’s own capital requirements.

The high payout ratio also implicitly communicates that the company does not foresee major capital expenditure needs in the near term. With pharmaceutical sugar facilities already operational and digital transformation progressing incrementally, the current investment phase appears to be more about optimization than expansion — a posture consistent with disciplined cycle management.

Governance and ESG: Institutional Quality Improving

International investors will note that COFCO Sugar has received consecutive “A” ratings from the Shanghai Stock Exchange for information disclosure quality. Its Wind ESG rating was upgraded to “AA” following the publication of its 2024 ESG report, and the company passed ISO 37301 (compliance management) and ISO 56005 (innovation management) international certifications.

The company’s ESG framework — branded “ESG SWEET” — is structured around a “1+72+153” work system aligned with dual materiality principles. While the practical impact of such frameworks varies widely across Chinese listed companies, COFCO Sugar’s external recognition from multiple industry associations and media outlets suggests a genuine commitment rather than performative box-ticking.

For a state-controlled enterprise, the governance structure is relatively straightforward: SASAC holds 100% of COFCO Group, which in turn holds 50.73% of COFCO Sugar. There are no complex cross-holdings, no pledged shares at the controlling shareholder level, and the company explicitly states there are no unrecovered losses at the parent level affecting dividend capacity.

Investment Perspective: Valuing a Commodity Leader at Cycle Trough

COFCO Sugar presents a classic commodity cycle investment case. The 2025 results represent a clear earnings trough relative to the 2023 peak, with net profit declining 54% over two years. The question for investors is whether the current earnings base is sustainable, likely to deteriorate further, or poised for recovery.

Several factors support the case that the worst may be approaching its end. Global raw sugar production for 2024/2025 is estimated at 181 million tonnes by the USDA, but weather risks in key producing regions — particularly Brazil and India — remain ever-present. Any supply disruption could rapidly tighten the global balance and push prices higher. Meanwhile, China’s structural import dependency means domestic prices would amplify any global rally.

On the other hand, the risk factors are not trivial. A sustained period of global oversupply, further weakening of domestic consumption sentiment, or adverse changes in China’s sugar import policies could extend the downturn. The company’s significant working capital requirements — evidenced by quarterly cash flow swings exceeding RMB 1–2 billion — also mean that balance sheet management matters more during prolonged downturns than headline profitability might suggest.

What differentiates COFCO Sugar from a pure commodity play is its strategic optionality. The pharmaceutical sugar business, while small today, offers a credible path to structural margin improvement. The smart agriculture investments could gradually narrow the cost gap with global competitors. The brand-building efforts in B2B and consumer segments — including new customer wins like Mixue Ice Cream & Tea and Peach Lily bakery — suggest a deliberate shift from volume-driven commodity trading toward value-driven customer relationships.

Conclusion

COFCO Sugar’s 2025 results confirm what the market already suspected: the golden period for Chinese sugar margins that characterized 2023–2024 has decisively ended. Yet within the disappointing headline numbers lies a company that is investing through the cycle with unusual strategic clarity — building capabilities in pharmaceutical sugar, precision agriculture, digital manufacturing, and customer-centric product development that could meaningfully alter its earnings quality when the next upturn arrives.

For investors with a multi-year horizon, the combination of a 76% payout ratio providing downside protection, a dominant market position in a structurally supply-short domestic market, and emerging high-margin business lines makes COFCO Sugar a compelling case study in how a state-owned commodity champion can evolve. The key variable remains timing: sugar cycles are notoriously difficult to predict, and the patience required to hold through the trough is the price of admission for capturing the eventual recovery.

Disclaimer: This analysis is based on the official 2025 Annual Report Summary of COFCO Sugar Holdings Co., Ltd. (600737.SH) published on April 27, 2026. The information provided is for industry research and informational purposes only and does not constitute investment advice. While we strive for accuracy based on the provided source documents, ynsugar.com is not responsible for any financial decisions made based on this content. Commodity markets and stock investments involve inherent risks.