The official announcement of the India Sugar Export Ban 2026, following the release of DGFT Notification No. 16/2026-27 on May 13, 2026, has prompted the YNSugar Research Team to analyze the deep implications of this sudden policy shift.

India’s Directorate General of Foreign Trade (DGFT) issued an immediate ban on sugar exports on May 13, 2026 — a sharp policy reversal that caught global commodity markets off guard and sent international sugar prices surging within hours.

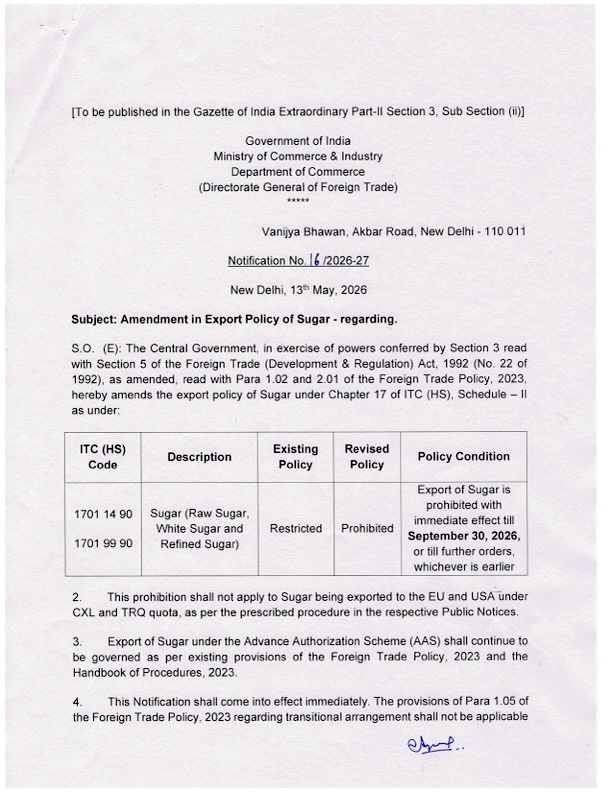

What the Notification Actually Says

Under Notification No. 16/2026-27, the Indian government has amended the export classification of Raw Sugar, White Sugar, and Refined Sugar (ITC HS Codes 1701 14 90 and 1701 99 90) from “Restricted” to “Prohibited”, effective immediately and valid through September 30, 2026, or until further orders — whichever comes first.

The notification was issued under Section 3 of the Foreign Trade (Development & Regulation) Act, 1992, and carries the authority of the Minister of Commerce & Industry, signed off by DGFT Director General Lav Agarwal.

Four Key Exemptions

Not all sugar exports are halted. The ban explicitly carves out the following categories:

-

EU and US quota shipments under the CXL and TRQ quota frameworks remain permitted under existing procedures

-

Advance Authorization Scheme (AAS) exports continue under Foreign Trade Policy 2023 provisions

-

Government-to-government (G2G) exports may be approved to address food security needs of requesting nations

-

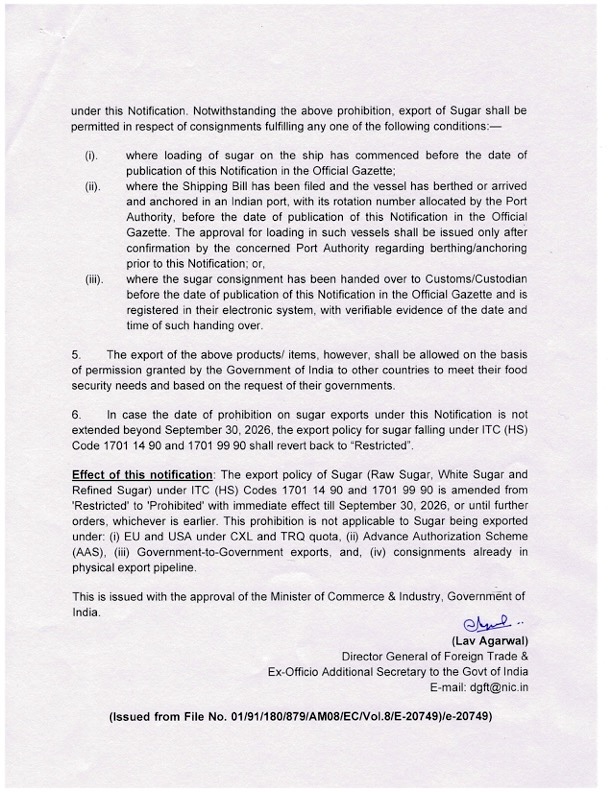

In-transit consignments — shipments already loaded, vessels already berthed with port rotation numbers assigned, or cargo already handed to customs prior to the notification date — are grandfathered in

Critically, the notification explicitly states that transitional arrangement provisions (Para 1.05 of FTP 2023) do not apply, meaning there is no grace period for new shipments.

Why Now? The Supply Story Behind the Ban

A Season of Downward Revisions

India’s 2025-26 sugar season has been marked by a steady stream of production downgrades. The All India Sugar Trade Association (AISTA) cut its output forecast by 4.4% to 28.3 million metric tonnes in early March 2026, citing adverse weather conditions in Maharashtra and Uttar Pradesh — the country’s two largest cane-growing states — which compressed sugarcane yields. After factoring in sugarcane diverted to ethanol production, net sugar availability narrowed considerably against domestic consumption needs of approximately 28 million tonnes.

The Stunning Policy U-Turn

What makes this ban particularly significant is its speed and reversal of prior official positions. As recently as April 6, 2026, India’s Food Secretary publicly stated there were “no plans to restrict sugar exports”. On May 5, 2026 — just eight days before the ban — Reuters reported that India “sees no need to curb sugar exports for now”. The speed of this reversal strongly suggests that domestic supply assessments deteriorated sharply in early May, likely compounded by uncertainty around the upcoming June–September monsoon season. A below-average monsoon would threaten not just current-season supplies but next year’s cane crop as well, justifying a precautionary lock-down of export availability.

Market Impact: Winners, Losers, and Price Dynamics

Immediate Price Reaction

Global sugar markets responded instantly. New York raw sugar futures (Contract #11) and London white sugar futures both jumped sharply upon the announcement. The reaction reflects India’s status as the world’s second-largest sugar exporter — any withdrawal from the export market creates a structural supply gap that other producers must scramble to fill.

Who Gains and Who Loses

Reading the Fine Print: Policy Design and Intent

The notification’s structure reveals deliberate policy craftsmanship. By setting a hard deadline of September 30 — the end of India’s sugar marketing year — the government preserves maximum flexibility. Clause 6 explicitly states that if the ban is not extended beyond September 30, 2026, export policy automatically reverts to “Restricted” status. This is not a permanent prohibition; it is a managed supply buffer, designed to ensure sufficient closing stocks before the next crushing season begins in October.

The G2G exemption (Clause 5) also signals diplomatic sensitivity — India is not abandoning its role as a food security partner to smaller economies, but rather prioritizing state-managed allocations over open commercial exports.

What to Watch Through Q3 2026

Three variables will determine whether this ban is lifted on schedule or extended:

-

2026 monsoon performance — A normal or above-average monsoon would ease fears over next season’s supply and support a timely ban lift. A weak monsoon almost certainly triggers an extension.

-

Domestic sugar inventory levels — If mill-level closing stocks trend above 6–7 million tonnes by September, the government has room to reopen exports.

-

Ethanol blending targets — India’s aggressive push toward 20% ethanol blending in petrol competes directly with sugar production. If cane diversion to ethanol remains high, usable sugar output stays constrained regardless of crop size.

Bottom Line

India’s export ban is a textbook case of a large agricultural producer prioritizing domestic food security over trade commitments in the face of production uncertainty. The move will keep international sugar prices elevated through at least September 2026, redirect trade flows toward Brazilian and Thai origins, and force importers across Asia and Africa to reprice procurement strategies. For industry professionals and commodity analysts tracking global sugar trade, the key date to watch is late September 2026, when India will signal whether supplies have recovered enough to reopen the world’s second-largest export tap.

: Does This Ban Affect China’s Sugar Market?

From the perspective of the Chinese sugar market, India’s export prohibition carries three notable — if limited — implications.

Firmer international prices offer a floor for domestic values. The ban lends upward support to global raw sugar prices at a time when China’s domestic market is entering a multi-season production expansion cycle. Both the 2025/26 and 2026/27 crushing seasons are forecast to deliver output growth, creating natural downward pressure on domestic prices. A stronger international benchmark helps slow that decline, offering mild relief to Chinese mills and trading houses.

Brazil remains China’s dominant supplier — India’s exit changes little. Over 80% of China’s imported sugar originates from Brazil, with Indian sugar accounting for a negligible share of total import volumes. From a supply chain and procurement standpoint, Chinese buyers are essentially unaffected by this ban. No meaningful sourcing diversification is required.

Policy reference value: minor, but worth a footnote. If one were to stretch for a broader lesson, India’s move is a textbook example of a major producer placing food security above export revenue — a logic that Chinese policymakers have themselves applied in various commodity sectors over the years. The direct parallels are limited.

In short: India’s ban is a significant event for global sugar trade, but for China’s market specifically, the impact is marginal. Watch the price channel, ignore the supply channel.

Source: Government of India, Ministry of Commerce & Industry, DGFT Notification No. 16/2026-27, dated May 13, 2026. Filed under ITC (HS) Chapter 17.

Disclaimer: The analysis provided in this report is for informational purposes only and does not constitute financial, investment, or commercial advice. While based on official government notifications and market data available as of May 13, 2026, YNSugar does not guarantee the future accuracy of market predictions or policy changes.