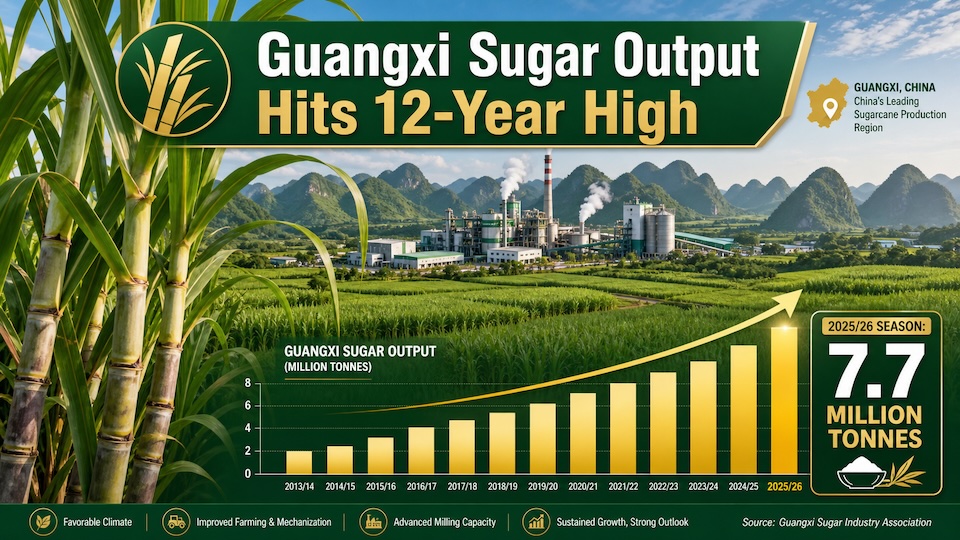

China’s largest sugarcane-producing region delivers an estimated 7.7 million tonnes of sugar — the highest level since 2013/14 — exceeding pre-season forecasts by a wide margin.

Guangxi, which accounts for roughly 60% of China’s domestic sugar supply, officially closed its 2025/26 crushing season in early May 2026. Production significantly outpaced industry expectations, marking a 12-year high for the region. Meanwhile, planting for the upcoming 2026/27 season is already in its final stretch.

Production Overview: A 12-Year Peak

By April 30, 2026, Guangxi’s mills had crushed a cumulative 60.91 million tonnes of sugarcane, an increase of 12.31 million tonnes year-on-year. Mixed sugar production reached 7.6951 million tonnes, up 1.2301 million tonnes from the previous season. The sugar yield rate declined to 12.63%, down 0.67 percentage points — a modest trade-off more than offset by the substantial gain in cane volume.

The season officially concluded on May 9, 2026, when the Xijiang Sugar Mill, operated by Guangxi Sugar Industry Group, completed its final crushing run. Total sugar production is now estimated at approximately 7.7 million tonnes, an increase of around 1.24 million tonnes (+19.1%) over 2024/25.

The figure substantially overshoots early-season market forecasts, which had clustered in the 6.8–7.0 million tonne range, and represents Guangxi’s strongest output in 12 years, since the 2013/14 season.

Guangxi Sugar Production: 12-Year Historical Context

The scale of this year’s rebound becomes clearer when placed against the backdrop of the past decade:

| Sugar Season | Production (10,000 tonnes) | YoY Change | Notes |

|---|---|---|---|

| 2014/15 | 634.00 | — | Baseline |

| 2015/16 | 511.00 | −19.40% | Period low |

| 2016/17 | 529.50 | +3.62% | Recovery phase |

| 2017/18 | 602.50 | +13.79% | Expansion |

| 2018/19 | 634.00 | +5.23% | Returned to 2014 level |

| 2019/20 | 600.00 | −5.36% | Slight contraction |

| 2020/21 | 628.80 | +4.80% | Stable growth |

| 2021/22 | 611.90 | −2.69% | Minor fluctuation |

| 2022/23 | 527.00 | −13.87% | Significant decline |

| 2023/24 | 618.14 | +17.29% | Strong rebound |

| 2024/25 | 646.50 | +4.59% | Continued growth |

| 2025/26 | 770.00 | +19.10% | 12-year historic high |

After bottoming out at 5.27 million tonnes in 2022/23 — a low point driven by drought stress and narrow planting margins — Guangxi’s sugar industry has now posted three consecutive seasons of growth, culminating in this year’s decisive breakout above the 7-million-tonne threshold.

Operational Snapshot

A total of 73 mills were active during 2025/26, just one fewer than the previous season. The crushing campaign ran for 175 days, extending 30 days longer than 2024/25 — a reflection of the larger cane volumes processed rather than operational inefficiencies.

Planting for 2026/27: Cautiously Optimistic

As of early May, sugarcane planting progress for the 2026/27 season had already surpassed 90%, according to field surveys. While the late conclusion of crushing has delayed systematic seedling assessments at many mills, early indicators are encouraging.

Weather has played a central role. Above-average temperatures and ample rainfall through the past winter and spring have supported strong germination across Guangxi’s cane belts. By the end of April, seedling conditions in most producing areas were reported to be better than the historical average.

Acreage: Modest Growth, Greater Discipline

Analysis from the YnSugar Analysis Team indicates that Guangxi’s sugarcane planted area will continue to expand in 2026, though the pace of growth is noticeably narrower than in the previous two seasons. A definitive read on acreage changes is unlikely before June or July, once new plantings and mill-led land surveys are finalized.

Several structural factors are underpinning farmer sentiment:

- Stable procurement prices for sugarcane, reducing income volatility.

- Guaranteed offtake from local mills, ensuring reliable demand.

- Ongoing government subsidy programs that tilt economics in cane’s favor.

Compared with competing crops such as eucalyptus and citrus, sugarcane’s relative profitability has strengthened, encouraging growers to maintain or expand their cane plots.

That said, the era of aggressive expansion appears to be cooling. With cane supply now broadly aligned with mill processing capacity, sugar producers have scaled back incentive programs for new planting and field expansion, prioritizing balanced growth over volume-at-any-cost strategies.

Outlook: Solid Foundation, Watchful Eye on Weather

For the 2026/27 season, Guangxi enters the new cycle with a stable-to-slightly-larger planted area and a healthier-than-usual seedling base — both positive signals for China’s sugar production outlook.

However, risks remain. A potential return of El Niño-driven weather patterns could bring drought stress and heighten pest and disease pressure during the critical growth months ahead. Traders, importers, and analysts tracking Chinese sugar fundamentals will need to monitor these conditions closely through the summer.

Sources: Guangxi Sugar Industry Group; Crushing data and field research by YnSugar Analysis Team; Historical archives.

Disclaimer: This report reflects data available as of May 10, 2026, and is intended for sugar industry professionals and market analysts.

Meet the YnSugar Team at Guangxi Sugar Expo 2026

As part of our commitment to global sugar industry analysis, the YnSugar team will be present at the 19th Guangxi International Sugar Industry Technology & Smart Equipment Exhibition. This is the premier event to understand China’s technological leap in sugarcane processing.

Plan Your Visit:

-

When: July 24-26, 2026

-

Where: Hall D, Level 2, Nanning International Convention & Exhibition Center

-

Inquiries: [email protected]