The following analysis represents the personal views of YNSugar analysts and is provided for reference purposes only.

March 27, 2026 — China’s sugar sector is set for a period of relative stability in the 2025/26 marketing year, with the latest supply-demand projections pointing to improved stock levels and softer prices compared to recent years.

Key Takeaways

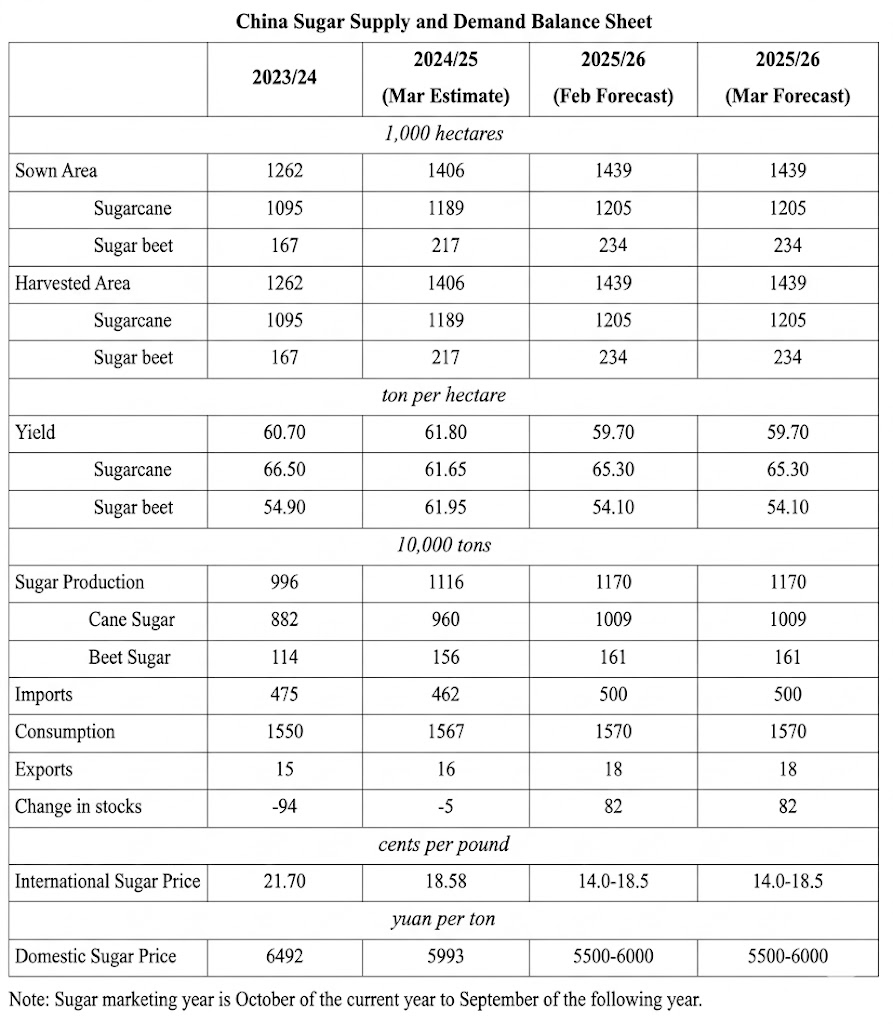

- Domestic production is forecast at 11.7 million metric tons (MMT), up from 11.16 MMT in 2024/25

- Imports projected at 5 MMT, with consumption steady at 15.7 MMT

- Prices expected to decline both domestically and internationally

Acreage Expansion Drives Output Growth

Chinese farmers continue to expand sugar crop plantings, with total harvested area projected at 1.439 million hectares—a 14% increase from 2023/24 levels. Sugarcane dominates at 1.205 million hectares, while sugar beet accounts for 234,000 hectares, primarily in northern regions.

However, yields have pulled back from last season’s highs. Overall sugar crop yields are forecast at 59.7 tons per hectare, compared to 61.8 tons in 2024/25. Sugarcane yields are expected at 65.3 tons per hectare, with sugar beet at 54.1 tons.

Supply-Demand Balance Turns Positive

Perhaps the most significant development is the shift in China’s stock position. After running deficits of 940,000 tons in 2023/24 and 50,000 tons in 2024/25, the 2025/26 balance shows a surplus of 820,000 tons.

This turnaround reflects:

- Higher domestic production (+4.8% year-over-year)

- Stable import volumes at 5 MMT

- Flat consumption growth

Price Pressure Ahead

The improved supply picture is weighing on prices. International sugar prices are forecast in the range of 14.0–18.5 US cents per pound, well below the 21.7 cents seen in 2023/24 and 18.58 cents in 2024/25.

Domestic prices in China are expected to ease to ¥5,000–6,000 yuan per metric ton.

What This Means for Global Markets

China remains a major player in the global sugar trade. With domestic production on the rise and stock levels improving, import demand may face downward pressure in the medium term—a factor worth monitoring for exporters in Brazil, Thailand, and Australia.

That said, China’s consumption of 15.7 MMT still significantly outpaces domestic production, ensuring the country remains a net importer for the foreseeable future.

Note: The sugar marketing year runs from October through September. All figures are based on the March 2026 forecast.

Disclaimer: This article reflects the personal analysis and opinions of YNSugar analysts. It is intended for informational purposes only and should not be construed as investment advice.

1 thought on “China’s Sugar Market Outlook: Steady Growth Expected in 2025/26”