Source: UNICA data through March 16, 2026 | Analysis by YnSugar

⚠️ Disclaimer: The analysis and views expressed in this article represent the personal opinions of YnSugar analysts only and are provided for informational reference purposes. This content does not constitute investment advice, trading recommendations, or any form of financial guidance. Readers should conduct their own independent research before making any business or investment decisions. YnSugar.com assumes no liability for any losses arising from use of this information.

Brazil’s 2026/27 crushing season is set to begin on April 1. On the evening of March 27 (Beijing Time), the Brazilian Sugarcane Industry Association (UNICA) released its latest production report covering data through March 16 — marking the official close of the 2025/26 season. The final bi-weekly figures revealed a dramatic and extreme strategic shift: an almost complete pivot to ethanol production.

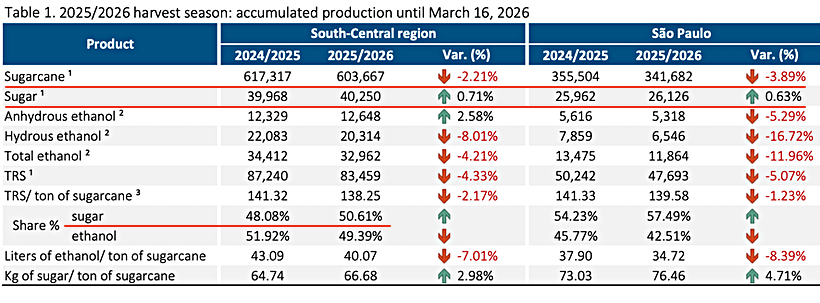

1. 2025/26 Season Overview: Lower Cane Crush, Sugar Output Edges Higher

According to UNICA’s latest data, cumulative sugarcane crushed in Brazil’s Center-South region through March 16 reached 603.67 million metric tons, down 2.21% year-on-year. São Paulo state processed 341.68 million metric tons, down 3.89% YoY. Cane quality also declined, with Total Recoverable Sugars (TRS) per metric ton falling from 141.32 kg in the prior season to 138.25 kg, a 2.17% YoY decline.

Despite lower cane volumes, cumulative sugar production achieved modest counter-trend growth. Center-South output reached 40.25 million metric tons, up 0.71% YoY. São Paulo state produced 26.126 million metric tons, up 0.63% YoY.

In terms of sugar-ethanol mix, the sugar allocation ratio rose significantly from 48.08% last season to 50.61% this season. São Paulo’s ratio climbed from 54.23% to 57.49%, reinforcing the season’s dominant “sugar-first” theme.

2. 2025/26 Ethanol Production

In contrast to sugar’s modest gains, the ethanol sector underperformed overall. Cumulative ethanol production in Brazil’s Center-South region totaled 32.962 billion liters, down 4.21% YoY.

-

Anhydrous Ethanol: 12.648 billion liters, up 2.58% YoY — the only ethanol category to post positive growth

-

Hydrous Ethanol: 20.314 billion liters, down 8.01% YoY — the primary drag

São Paulo state fared worse, with total ethanol output at 11.864 billion liters, down a sharp 11.96% YoY, and hydrous ethanol falling 16.72%.

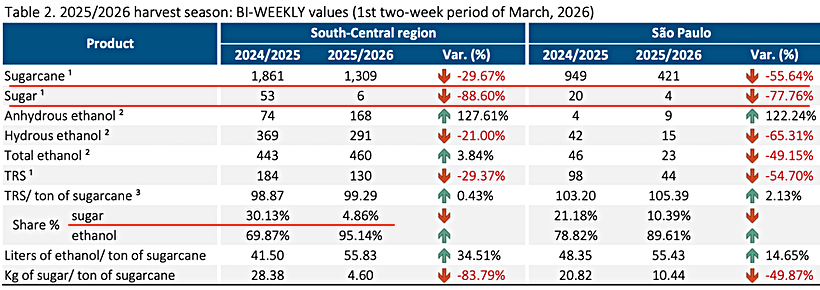

3. Bi-Weekly Data: Dramatic Sugar-to-Ethanol Reversal in Early March

The early March (March 1–16) bi-weekly figures are the most striking element of this report, showing an almost complete production pivot from sugar to ethanol — a sharp contrast to the season’s cumulative “sugar-first” pattern.

Center-South bi-weekly cane crush fell to just 1.309 million metric tons, down 29.67% YoY, reflecting the sharp reduction in active mills at season-end. Bi-weekly sugar output collapsed to only 0.06 million metric tons, plunging 88.60% YoY. The sugar allocation ratio plummeted from 30.13% in the same period last year to just 4.86%, while ethanol’s share surged to 95.14% (vs. 69.87% a year ago).

Bi-weekly total ethanol production reached 460 million liters, up 3.84% YoY:

-

Anhydrous Ethanol: 168 million liters, surging 127.61% YoY (vs. 74 million liters last year) — the standout figure of this report

-

Hydrous Ethanol: 291 million liters, down 21.00% YoY

São Paulo state also showed a strong ethanol bias but with limited absolute output due to sharply reduced cane processing. Bi-weekly cane crush: 421,000 metric tons, down 55.64% YoY. Sugar output: 4,000 metric tons, down 77.76% YoY. Sugar ratio dropped from 21.18% to 10.39%, with ethanol share rising to 89.61% (vs. 78.82% a year ago).

4. Price Driver: Ethanol Sugar-Equivalent Premium Exceeds 18%

Clear price logic underpins this dramatic production shift.

Before mid-March, when the Trump administration escalated military action against Iran, ICE raw sugar futures had already fallen to approximately 14.1–14.4 cents/lb — near five-year lows. The onset of conflict pushed energy prices higher, stimulating demand for fuel ethanol.

Brazil’s ethanol sugar-equivalent price reached 18 cents/lb, representing a 18%–27% premium over raw sugar. With ethanol inventories in Brazil remaining persistently low — further supporting elevated ethanol prices — mills at season-end had every incentive to effectively abandon sugar production and maximize ethanol output from remaining cane.

📊 Supply Chain Note: The ethanol-sugar production ratio shift has direct implications for China’s sugar import volumes and sourcing strategy in 2026–27. Explore the compiled transactional records instantly.

5. Summary & Outlook

The 2025/26 season maintained an overall “sugar-first” profile with a cumulative sugar ratio exceeding 50.6%. However, the final weeks saw a dramatic reversal: Center-South sugar allocation collapsed to 4.86%, ethanol share surged to 95.14%, and anhydrous ethanol production more than doubled YoY.

This end-of-season shift does not signal a full strategic change. Rather, it reflects the rational decision of a shrinking number of still-operating mills to maximize ethanol output from remaining cane supplies, driven by persistently weak sugar prices and a significant ethanol premium.

Looking ahead, as Brazil’s 2026/27 season is expected to begin rolling out from April onward, market consensus anticipates the sugar allocation ratio will ease from this season’s elevated 50.6% back toward approximately 48%. With ethanol profitability remaining attractive, Brazilian mills are expected to prioritize fuel ethanol production — a dynamic with meaningful implications for global sugar supply expectations and forward price trajectories.