Key Takeaway

China sugar imports 2025 data reveals a total volume of 4.92 million tonnes, marking a significant 13.1% year-on-year increase (up 570,000 tonnes) as declining international sugar prices spurred a robust recovery in buying activity. While imports saw a strong rebound, China’s export volumes remained modest at 144,000 tonnes, representing a 10.9% growth compared to the previous year.

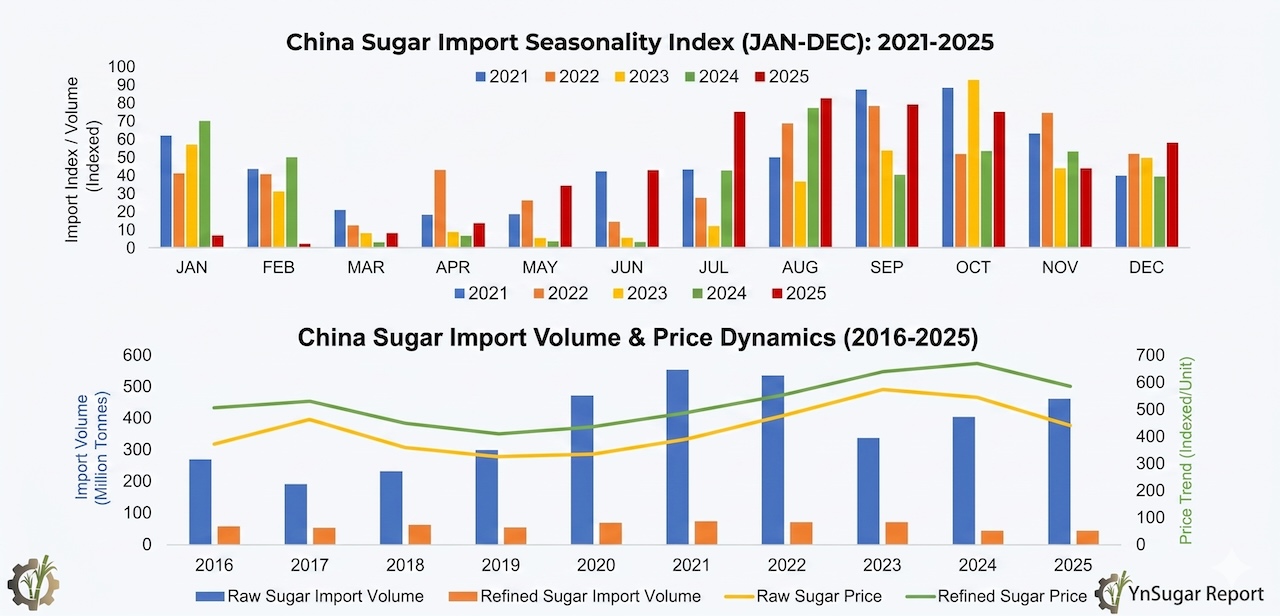

A Decade of Fluctuation

China’s sugar import trajectory over the past ten years can be broadly divided into three phases:

| Period | Annual Imports | Context |

|---|---|---|

| 2016–2019 | ~3 million tonnes | Decade-low trough |

| 2020–2022 | >5 million tonnes | Decade-high peak |

| 2023 | ~4 million tonnes | Pullback amid elevated global prices |

| 2024–2025 | Gradual recovery | Easing international prices |

Exports, by contrast, have remained negligible throughout the period.

Pronounced Seasonality

A distinctive feature of China’s sugar imports is their strong seasonal concentration. Volumes typically peak between August and December, while the March-to-July window consistently registers lower inflows (see Chart 1). Traders and analysts tracking China’s sugar demand should therefore expect heavier procurement activity in the second half of the calendar year.

Raw Sugar Dominates the Mix

Over the past decade, raw sugar has accounted for 80–95% of total sugar imports, consistently priced well below refined sugar (see Chart 2). General trade has been the primary import channel, representing over 50% of volumes — reaching 58.2% (2.86 million tonnes) in 2025, with other trade modes collectively making up the remaining 41.8%.

Brazil: The Undisputed Supplier

Brazil has cemented its position as China’s overwhelmingly dominant sugar supplier. Its share of China’s total sugar imports followed a U-shaped pattern — declining initially, then rising — before stabilizing at commanding levels:

- Pre-2020: Fluctuating share

- 2020 onward: Consistently above 70%

- 2024–2025: Approximately 90%

This extreme supplier concentration is a structural factor that market participants should monitor closely, given the implications for supply-chain resilience and price transmission from Brazilian crop conditions to the Chinese market.

Regional Registration & Distribution

Sugar imports are registered primarily in Beijing, Guangdong, and Shandong. Notably, Beijing saw a sharp drop in registered import volumes in 2025, falling to its lowest share in a decade. Eight provinces or municipalities each imported more than 100,000 tonnes, collectively accounting for 95.9% of the national total.

Data Sources: This report is synthesized from official public data provided by the China (GACC) and the China Sugar Association (CSA).