The global sugar market deficit 2026/27 is no longer a distant possibility but a growing consensus among top analysts…

The global sugar market is undergoing a significant structural shift in its supply-demand balance — and the signals are converging across multiple forecasting agencies.

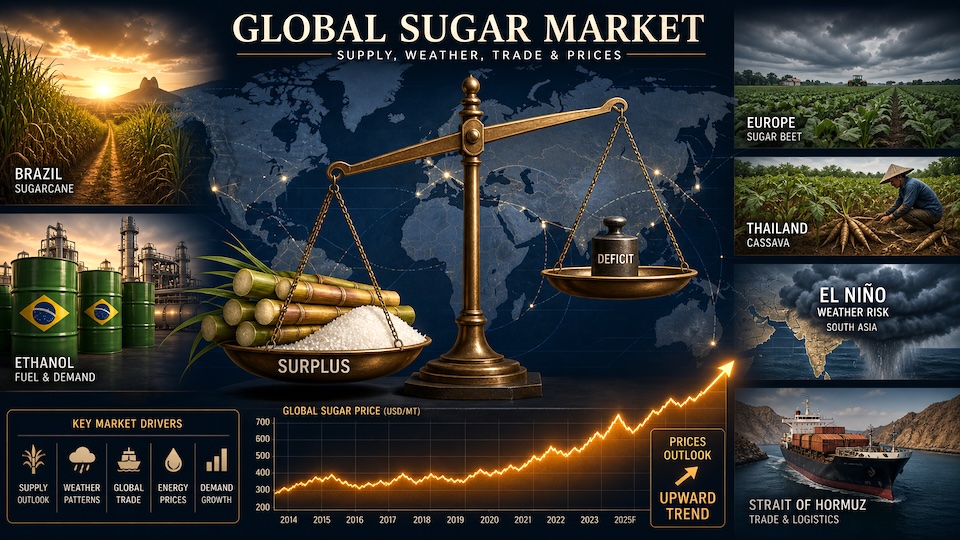

At this week’s New York Sugar Week (SugarWeek) annual conference, leading commodities financial firm StoneX projected that the global sugar market will swing from a surplus of 2.29 million metric tons in 2025/26 (October–September) to a deficit of 550,000 metric tons in 2026/27. Reuters also covered the forecast. The core driver: major producing countries are cutting output or shifting to alternative crops in response to persistently low sugar prices.

This view is not an outlier. Industry consensus is moving in the same direction:

-

Datagro raised its 2026/27 global sugar deficit estimate to 3.17 million MT, up from a prior forecast of 2.26 million MT

-

Covrig Analytics revised its 2026/27 surplus estimate down sharply, from 1.40 million MT to 800,000 MT

-

Czarnikow cut its surplus forecast dramatically, from 3.40 million MT to just 1.10 million MT

The forecasting curve across the industry is systematically shifting toward “tight balance” and in some cases, outright deficit.

Table: 2026/27 Global Sugar Balance Projections (by Agency)

| Forecasting Agency | Projection (2026/27) | Shift from Previous Forecast |

| StoneX | 550,000 MT Deficit | Swung from 2.29M MT Surplus |

| Datagro | 3.17M MT Deficit | Increased from 2.26M MT Deficit |

| Covrig Analytics | 800,000 MT Surplus | Down from 1.40M MT Surplus |

| Czarnikow | 1.10M MT Surplus | Down from 3.40M MT Surplus |

Key Producing Countries Facing Output Declines

European Union and United Kingdom are seeing the sharpest production cuts, driven by shrinking beet planting area under price pressure. StoneX projects EU+UK output will fall 12.5% to 15.3 million MT in 2026/27. Farmers responded to low prices by reducing beet acreage in 2025/26 — output that year is already expected to drop 7% year-on-year to 15.4 million MT — and planting intentions point to a further decline in 2026/27. Europe’s price mechanism is effectively self-correcting the supply side.

Thailand, one of the world’s leading sugar exporters, is another critical watch point. StoneX forecasts Thai output will fall 15% to 10.2 million MT, as farmers shift to cassava and other alternative crops. The dynamics go beyond simple price chasing:

-

The Thai government’s preliminary cane purchase price for the 2025/26 crush season was set at 900 Thai baht/MT (~$28.29), a 22% year-on-year drop, according to Green Pool — a level farmers say does not cover production costs

-

Cane-growing regions in northeastern Thailand have been hit hard by white leaf disease this season, prompting some farmers to uproot affected cane fields and replant with cassava

This is a sharp reversal from just over a year ago, when cassava prices collapsed 37% and farmers switched back to cane. Mitr Phol Group had at that point expected Thai cane production to jump from 92 million MT to 105 million MT. The price cycle has now turned in the opposite direction.

Brazil, the world’s largest sugar producer, continues to divert cane toward ethanol, suppressing sugar output. Citibank forecasts Brazilian sugar production at 39.5 million MT in 2026/27 — well below CONAB’s estimate of 43.95 million MT — citing mills’ strong incentive to maximize ethanol output as gasoline prices surge. This trend is already visible in recent data: UNICA reported that sugar production in Brazil’s Center-South region during the first half of April fell 11.9% year-on-year to 647,000 MT, with the cane-to-sugar allocation ratio dropping from 44.7% to just 32.9% compared to the same period last year.

Weather risk adds another layer of uncertainty. Citi warns that a potential strong El Niño pattern over the next 6–12 months could significantly impact sugar production in both India and Thailand. The USDA currently projects India will have a 2.5 million MT sugar surplus in 2026/27 — its first surplus in two years — potentially making India a key buffer against a global shortfall. However, that buffer depends heavily on El Niño not delivering worse-than-expected damage.

Geopolitical disruption is also providing additional price support, a factor that fundamental supply-demand models often underweight. Covrig Analytics notes that the closure of the Strait of Hormuz has affected approximately 6% of global sugar trade, constraining refined sugar output and adding a layer of uncertainty to an already tightening market. In a market with thin surplus margins, geopolitical shocks carry amplified price elasticity.

Finally, on May 13, the Indian government reinstated a sugar export ban, which relieved market concerns that India might redirect more cane toward ethanol production in response to potential crude oil supply disruptions linked to the Iran conflict. India’s export restriction effectively preserves a key safety valve for global sugar supply.

Does This Mean Sugar Prices Will Rally?

The shift from surplus to deficit in the supply-demand balance does create medium-term upside potential for prices. But several structural constraints are worth noting:

The deficit is modest in absolute terms. StoneX’s projected shortfall of 550,000 MT is a small fraction of global consumption of nearly 200 million MT. Markets can absorb modest deficits without dramatic price moves.

Brazil’s ethanol parity acts as an invisible price ceiling. As long as sugar prices remain below ethanol parity, Brazilian mills have an incentive to convert more cane to ethanol. If sugar prices rise above that threshold, mills can quickly pivot back to sugar production — an automatic self-correcting mechanism that caps the upside.

Demand growth is weak. Global sugar consumption is expected to grow only 0.5% — far slower than the pace of supply contraction. The ynsugar analysis team views this as a “passive” rather than “demand-driven” price recovery, meaning it lacks strong, sustainable upward momentum.

ynsugar Analysis Team Summary

The logic chain behind the 2026/27 shift from surplus to deficit is well-supported across major industry forecasters. We summarize it as:

Low prices forcing supply contraction (EU beet, Thai cane) + crop substitution pressure (cassava) + disease impact + ethanol diversion (Brazil) + weather risk (El Niño) + geopolitical disruption (Strait of Hormuz)

This is a classic supply-side structural shift — not a demand-driven rally.

For participants across the global sugar supply chain, the ynsugar team identifies three key nodes to monitor closely:

-

El Niño intensity in H2 2025 — this will determine the final scale of production declines in India and Thailand

-

Weather conditions in Brazil’s Center-South region in Q1 2026 — the most critical variable for Brazil’s new crush season output

-

The sugar-to-ethanol ratio in Brazil’s production reports — the most sensitive short-term “supply valve” in the market

The bottom line: sugar prices are unlikely to develop into a strong one-directional bull trend, but the lower bound of the trading range is systematically rising. For 2026/27, that may be the most important trading thesis to internalize.

Disclaimer: The information and analysis provided in this report are for informational purposes only and do not constitute financial, investment, or trading advice. While YNSugar strives for accuracy by sourcing data from reputable agencies like StoneX, Reuters, and Datagro, we do not guarantee the completeness or reliability of these projections. Commodity markets are subject to high volatility; readers should consult with a professional financial advisor before making any market commitments.