A convergence of weather risks, trade policy shifts, and energy market dynamics is shifting the global sugar market outlook 2026 toward a structural squeeze for the 2026/27 season. Leading commodity analysts now broadly agree that the era of comfortable sugar surpluses is drawing to a close—and a potential supply deficit may be closer than markets anticipated just months ago.

From Surplus to Deficit: What the Numbers Say

Two of the industry’s most closely watched forecasters have significantly revised their supply outlooks in recent weeks:

-

Czarnikow, the London-based global sugar trading house, now projects the 2025/26 global sugar surplus at just 5.8 million metric tons (MMT)—a downward revision of 2.5 MMT from its previous estimate. Looking further ahead, it forecasts the 2026/27 surplus narrowing dramatically to 1.1 MMT (down 0.3 MMT from prior projections). The firm cites El Niño weather risks in India, Thailand, and Brazil as the primary drivers of the downgrade.

-

StoneX takes an even more bearish view on supply. The commodities brokerage projects the global sugar market swinging from a surplus of 2.29 MMT in 2025/26 to a deficit of 0.55 MMT in 2026/27. Its baseline assumptions are:

-

Global production falling 1% to 193.7 MMT

-

Global demand rising 0.5% to 194.3 MMT

-

While the two firms’ absolute figures differ, the directional signal is entirely consistent: the global sugar balance is tightening, and markets are aggressively pricing in that reality. Whether actual crushing data confirms this trajectory over the summer will be critical—if reality matches expectations, the bullish trend continues; if it diverges, a short-term price correction is likely.

Three Structural Forces Driving the Bullish Outlook

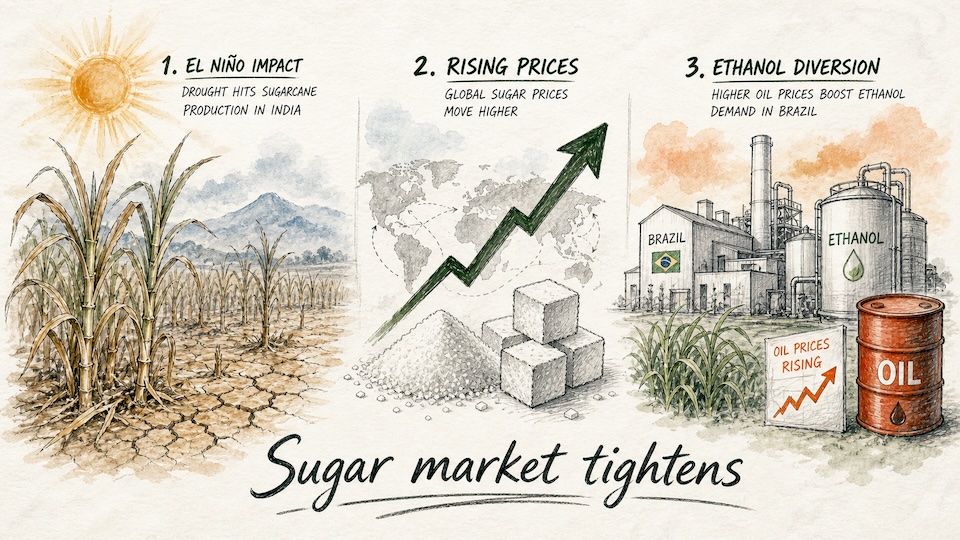

1. El Niño Probability at 82%

The U.S. Climate Prediction Center now puts the probability of an El Niño event forming in 2026 at 82%. For sugar markets, this carries severe structural implications:

-

In India and Thailand: El Niño typically weakens monsoon rainfall, leading to severe drought conditions, lower cane yields, and reduced sugar content per ton of cane.

-

In Brazil’s Center-South region: El Niño has the opposite effect—bringing excess rainfall—but this comes with its own unique set of logistical and production challenges (discussed below).

2. India Bans Sugar Exports Through September 2026

On May 13, 2026, the Indian government formally banned sugar exports effective immediately through September 30, 2026. The decision reflects a sharp deterioration in India’s domestic supply outlook and marks a pivotal moment for global trade flows.

The underlying fundamentals tell a concerning story:

-

India’s sugar production in 2024/25 and 2025/26 is estimated at 26.5 MMT and 27.6 MMT respectively, both falling below annual domestic consumption of approximately 28 MMT.

-

The government had initially approved a 1.59 MMT export quota for 2025/26, expecting a surplus, but lower-than-expected cane yields in the key state of Maharashtra completely erased that margin.

-

Under a neutral El Niño scenario, 2026/27 Indian production could fall another 10% to around 25 MMT.

Running the numbers on India’s sugar balance for 2026/27 highlights the domestic pressure:

| Balance Sheet Item | Volume (MMT) |

| Estimated Carry-in Stocks | 4.3 |

| Projected Production | 25.0 |

| Total Supply | 29.3 |

| Domestic Consumption | 28.0 |

| Estimated End-Season Stocks | 1.3 |

| Government Safe Stock Threshold | 4.5 |

India’s ending stocks would fall nearly 3.2 MMT below the government’s own minimum safety buffer, potentially transforming the world’s second-largest sugar producer from a net exporter into a net importer of up to 2 MMT.

3. Brazil’s Ethanol Mandate Is Pulling Cane Away from Sugar

Brazil remains the world’s largest sugar exporter, but government energy policy is now redirecting a meaningful share of its cane harvest. In response to elevated global oil prices—with Brent crude trading above $100/barrel amid ongoing Middle East tensions—Brazil raised its mandatory ethanol blending ratio from 30% to 32% for gasoline, effective May 2026.

The mechanics of this macro shift are significant:

-

Each 1 percentage point increase in the blending mandate diverts approximately 2.5% of cane from sugar production to ethanol distilleries.

-

The 2-point increase from 30% to 32% is estimated to shift roughly 5% of total cane into ethanol.

-

Brazil’s sugar-to-cane ratio (the taxa de açúcar) is expected to drop from ~51% in 2025/26 to approximately 46% in 2026/27.

Based on 2025/26 production of approximately 44.5 MMT, each 1-point decline in the sugar ratio reduces output by roughly 800,000 MT—meaning a 5-point drop implies a ~4 MMT production decrease.

El Niño adds a further complication for Brazil. While excess rainfall in the Center-South is expected to boost total cane tonnage by around 5.3% to 709.1 MMT (per Brazil’s national supply company CONAB), prolonged cloudiness and wet conditions typically suppress sugar content (ATR) by 0.5–1.0 percentage points.

Combining all factors—the sugar ratio shift, higher cane volume, and lower ATR—Brazil’s 2026/27 sugar production is estimated to decline 10–12% from the prior season, down to roughly 39–40 MMT.

The Combined Supply Shock: Three Major Producers, One Direction

Aggregating the projected output changes across the three largest producing nations reveals a substantial volume erosion for a market that was already seeing its surplus evaporate:

Projected Production Declines for 2026/27

├── India : ⬇️ ~2.5 MMT (Due to El Niño drought)

├── Thailand: ⬇️ ~1.8 MMT (StoneX projects a 15% decline to 10.2 MMT on shrinking planted area)

└── Brazil : ⬇️ ~4.5 - 5.5 MMT (Combined ethanol mandate shift and weather effects)

====================================================================================

Total Supply Reduction: ⬇️ 8.8 – 9.8 MMT

China: Domestic Abundance Tempers the Bullish Story for Now

China’s role in the global sugar market warrants close attention, and the domestic picture is far more nuanced than the international headlines suggest. Domestic production has significantly outperformed early-season estimates. According to data compiled by the ynsugar analysis team:

-

Guangxi, China’s largest sugar-producing region, is on track to produce approximately 7.7 MMT in 2025/26—well above initial forecasts.

-

Yunnan, the second-largest producing province, is expected to exceed 2.8 MMT.

-

National production is projected to surpass 12.8 MMT, with further growth anticipated in 2026/27.

China’s import data presents a mixed picture. April 2026 imports collapsed to just 30,000 MT—down 80% year-on-year—though cumulative January–April imports still total over 650,000 MT, up 129% from the same period last year.

The market’s attention is now focused on China’s out-of-quota import licensing as a key swing variable. With domestic supply elevated, authorities have the structural option to delay issuing out-of-quota import licenses, which would:

-

Shield the domestic market from additional foreign supply pressure through July.

-

Prioritize in-quota imports and defer discretionary out-of-quota volumes to August and beyond, once domestic inventory has partially cleared.

The bottom line for China: the domestic supply situation remains comfortable—potentially at its highest stock-to-consumption ratio in a decade—which may cause domestic spot prices to lag the international rally in the near term. The bullish global story is real, but the Chinese domestic market needs time to work through its strong local harvest.

Data Sources: * Czarnikow Global Sugar Outlook (May 2026)

-

StoneX Commodities Research

-

India Ministry of Consumer Affairs, Food and Public Distribution

-

General Administration of Customs of the People’s Republic of China (GACC)

-

YnSugar Internal Research Database

Disclaimer: The trade analysis, statistical forecasts, and market outlooks presented in this report are compiled by the ynSugar research team for general informational and educational purposes only. This commercial intelligence does not constitute financial, legal, or investment advice. Global agricultural commodity trading involves substantial market risk. Market participants should consult qualified financial advisors and perform rigorous independent compliance verification before executing any commercial positions or trade contracts. ynSugar assumes no financial liability for trading outcomes based on this content.