Welcome to the latest ICE Sugar No. 11 Weekly Review, where we analyze the convergence of technical bottoms and emerging climate risks…

I. Market Recap

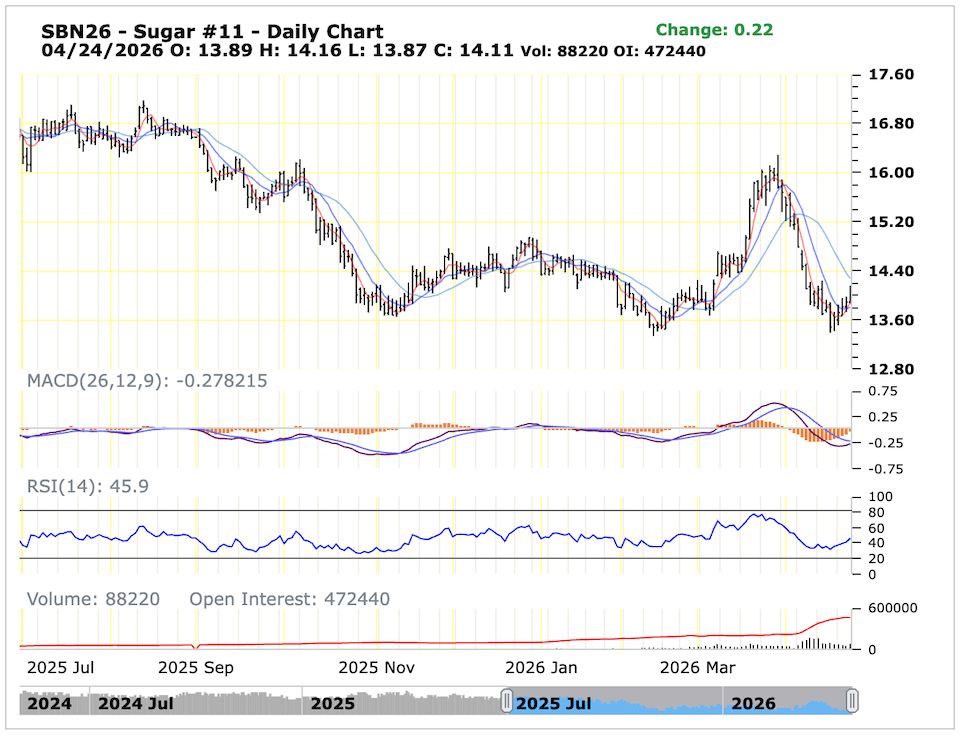

On Friday (April 24), the front-month July contract of ICE Sugar No. 11 futures last traded at 14.11 cents/lb, gaining 0.22 cents on the day for a 1.58% advance, with an intraday high of 14.16 and a low of 13.87. Open interest rose by 4,587 contracts to 472,440, while trading volume reached 88,220 contracts—a classic pattern of price and volume rising in tandem.

From a technical structure perspective, sugar prices previously declined from a high of 16.29 cents to find support near 13.39 cents, establishing a stage bottom. The current price has reclaimed both the 5-day moving average (13.83) and the 10-day moving average (13.81), but remains capped by the 20-day MA (14.43), 40-day MA (14.59), and 60-day MA (14.33). Bulls need to break through these medium- and long-term moving averages to confirm a reversal. On the MACD front, while DIFF (-0.28) and DEA (-0.23) remain below the zero line, the red histogram has begun to contract, with the STICK value of -0.10 indicating sustained weakening of bearish momentum and showing signs of bottom divergence.

Notably, the latest COT positioning report reveals one of the most extreme positioning imbalances in Sugar No. 11 over the past 18 years: commercial net long positions stand at 128,130 contracts—the second highest since 2007 (only behind the approximately 160,000 contracts in September-October 2020)—while non-commercial (fund) net short positions reach -125,628 contracts. This extreme positioning structure suggests the potential for a short squeeze driven by short covering ahead.

II. Fundamental Drivers in Global Markets

1. Short-Term Rebound Momentum

The May front-month ICE raw sugar futures contract closed up 0.33 cents (+2.43%) on Friday, while the August London White Sugar #5 contract (SWQ26) closed up $7.80 (+1.82%). Sugar prices extended this week’s gains, with NY sugar hitting a one-week high and London sugar reaching a two-week high. The recent strength of the Brazilian real has triggered short covering in sugar futures, with the real climbing to a two-year high against the U.S. dollar on Thursday, dampening export sales by Brazilian sugar producers.

2. Downward Revision of Brazilian Supply Outlook

Reduced Brazilian sugar production expectations are providing price support. On Tuesday, the USDA forecast Brazil’s 2026/27 sugar production at 42.5 million tonnes, down 3% year-on-year, citing increased allocation of cane toward ethanol production rather than sugar. This shift is closely tied to rising crude oil prices, as higher energy prices improve ethanol production economics, prompting mills to favor a higher cane-to-ethanol ratio.

3. Revisions to Global Supply-Demand Balance

Several international consultancies have downgraded their global surplus estimates:

Covrig Analytics on Tuesday cut its 2026/27 global sugar surplus forecast from the prior 1.4 million tonnes to 800,000 tonnes. Czarnikow analysts lowered their 2026/27 global sugar surplus estimate to 1.1 million tonnes, reflecting the potential impact of El Niño on cane production in India, Thailand, and Brazil. This represents a 300,000-tonne downward revision from the March forecast and is far below the February projection of 3.4 million tonnes. Global sugar production for 2026/27 is now estimated at 180.4 million tonnes, 200,000 tonnes lower than the March forecast, while global sugar consumption is expected to reach 179.3 million tonnes, up 100,000 tonnes from previous estimates.

4. Crude-Oil-Driven Ethanol Competition

The crude oil market has been a key catalyst for the sugar rebound.

ICE sugar futures climbed to more than a one-week high, primarily driven by rising oil prices and reduced production forecasts for the next crop year. Brent crude returned above $106/barrel, hitting a more than two-week high with weekly gains exceeding 4%. Persistent shipping disruptions caused by the Iran conflict have intensified oil price volatility, potentially encouraging mills to direct more cane toward ethanol production.

Higher crude oil prices have improved the ethanol parity for Brazilian sugar mills, making ethanol relatively more attractive than sugar. This will accelerate the downward shift in the sugar-mix ratio and provide additional upside support for sugar prices. This dynamic is also one of the reasons ICE raw sugar futures have rebounded from their February lows.

5. WMO El Niño Warning: Climate Factors Reignite

On Friday (April 24), the World Meteorological Organization (WMO) released its latest report, warning that El Niño could reemerge as early as May to July 2026, with early indications suggesting this El Niño event may be of significant intensity. This news became one of the key catalysts for Friday’s sugar price rally, with market concerns about climate disruptions in major sugar-producing countries notably escalating.

Historical experience shows that El Niño impacts the global sugar supply chain through the following transmission channels:

Drought risk in India and Thailand: El Niño typically weakens monsoons in South and Southeast Asia, leading to below-normal rainfall. As the world’s second-largest sugar producer, India—along with Thailand, the second-largest exporter—would see direct cuts to next year’s production outlook if cane-growing regions face drought. The El Niño event during the 2023/24 crushing season previously caused a sharp decline in Indian production and led to export restrictions.

Excess rainfall risk in Brazil: El Niño often brings excessive rainfall to Center-South Brazil, affecting cane harvest progress and sugar accumulation (lower ATR), while bringing drought to northern Brazil.

If El Niño formation is confirmed between May and July with strong intensity, the 2026/27 global supply-demand balance could tighten further, with the possibility of shifting from surplus to tight balance or even deficit.

III. Persistent Bearish Pressures

Despite strong short-term rebound momentum, medium- and long-term suppressing factors cannot be overlooked.

Late-April data shows that expectations of substantial 2025/26 surplus continue to dominate. The latest figures indicate that India’s sugar production from October to March of the 2025/26 marketing year rose 9% year-on-year to 27.12 million tonnes, while Center-South Brazil production edged up 0.7% to 40.25 million tonnes, with mills favoring sugar production. Additionally, Brazil’s 2026/27 crushing season has already begun harvesting and is gradually adding to supply, leaving spot supply pressure intact in the near term.

IV. YnSugar Market Outlook

Comprehensive Assessment: In the short term, sugar prices are benefiting from the resonance of four bullish factors—real strength, rising crude oil, downward revisions of surplus estimates by analytical institutions, and the WMO’s El Niño warning—significantly enhancing rebound momentum. Technically, the K-line has broken away from the 13.39 low to form a short-term bottom structure, and combined with the extreme positioning landscape (massive fund net shorts), there is room for a stage short-squeeze rally. The shift in climate expectations could become a critical inflection point in breaking the previous one-sided downtrend.

Risk Factors: Four key variables warrant close attention:

① The progress of the 2026/27 crushing season in Center-South Brazil and changes in the sugar-mix ratio;

② The impact of Middle East geopolitical developments on crude oil;

③ USD/BRL exchange rate movements;

④ Subsequent WMO El Niño monitoring reports and the actual monsoon rainfall conditions in India and Thailand.

Disclaimer:

This article is for informational and industry analysis purposes only and does not constitute financial or investment advice. The market data, technical levels, and climate forecasts (including information from ICE, USDA, WMO, and Czarnikow) are based on the latest available reports as of April 24, 2026. Commodity markets are inherently volatile; ynsugar.com is not responsible for any market decisions or financial outcomes resulting from the use of this content.