The Germany industrial sugar market has long stood as one of Europe’s sugar-producing powerhouses, but the 2025/26 season marks a critical turning point…

How the EU Common Agricultural Policy Reshaped Germany’s Sugar Industry: A Data-Driven Analysis

Germany has long stood as one of Europe’s sugar-producing powerhouses, but the past two decades have transformed the sector almost beyond recognition. From the 2006 reform of the Common Market Organization to the abolition of production quotas in 2017, EU sugar policy under the Common Agricultural Policy (CAP) has reshaped how German farmers grow beets, how processors compete, and how much sugar ultimately reaches the market. With the latest 2025/26 figures from the German Sugar Association (WVZ) now confirmed, the contraction many analysts predicted has materialized—and this article examines those changes with the most recent data available.

1. The Legacy Regime: Quotas, Intervention Prices, and Protected Markets

For nearly half a century, Germany’s sugar industry operated inside one of the most tightly regulated markets in European agriculture. For decades, the EU sugar market was highly regulated by production quotas, intervention prices, prohibitive import tariffs and export subsidies. Moreover, the EU sugar regime had long been excluded from the liberalisation process of the EU Common Agriculture Policy (CAP) started with the MacSharry reform in 1992.

The Common Market Organization for Sugar regulated the sugar market in the European Union. For a long time, it was also known as the EU sugar quota system, after its most notable aspect. The sugar production quotas were in place from 1968 to 2017. Before ending the quota system, a thorough restructuring of the sugar production sector took place between 2006 and 2010. What now remains of the Common Market Organization is a much looser regulation.

The original logic was straightforward: in order to meet the goals of the CAP, the intervention prices for sugar were so high that even the least efficient producers could make an income. The actual wholesale prices were usually well above the intervention prices, which were in turn normally well above world market prices. Germany, with its highly productive beet regions in Lower Saxony, North Rhine-Westphalia, and Bavaria, was a major beneficiary—generating consistent farm income and supporting a powerful processing sector dominated by firms like Südzucker, Nordzucker, and Pfeifer & Langen.

2. The 2006 Reform: A Turning Point

External pressure—particularly from a WTO dispute initiated by Brazil—forced the EU’s hand. With the end of the “peace clause” signed in Marrakesh, Brazil struck the charge against the European sugar policy by seizing the WTO in 2003. The world’s largest sugar exporter accused the EU of not counting re-exports of ACP sugar in its export subsidy limitation commitments. In addition, it challenged the double quota system as a form of export subsidy for over-quota production. This standoff led the European Union to meet its commitments made at the time of the creation of the WTO: subsidized exports should not exceed 1.35 Mt even though the volumes actually marketed were more than 5 Mt.

The response was the 2006 reform, which represented a complete change of logic in the regulation of the European sugar sector. Under the 1968 regime, exports were the adjustment variable to stabilize the domestic market and the volume of imports was under control. The aim of the reform was to cap exports and adjust European production, taking into account almost unimpeded import flows. To adjust the internal market, quotas were maintained but reduced by more than 6 Mt in 3 years. The restructuring was done on a voluntary and incentive basis: it proposed to buy back the quotas and compensate plant shutdowns. The restructuring fund was directly fueled by a tax on sugar.

For Germany, the reform produced a paradoxical outcome. While many EU member states downsized dramatically, Germany consolidated its position. Modeling at the time projected that production in France, Germany and Poland would not be affected by the decrease in the price policy; rather output may increase by about 1.7 and 1.6 percent in France and Germany respectively, and by 0.7 percent in Poland. Production was reduced in virtually all other member states, and more significantly in Italy, the UK, Spain, Belgium, Greece, Sweden, Denmark and the Czech Republic.

3. The 2017 Quota Abolition: Liberalization Hits Home

The truly seismic shift came on 1 October 2017. Since 2006, the EU sugar market has been gradually liberalised. While in the 2006 reform EU production quotas were considerably reduced, the EU quota system was completely abolished in 2017. In addition, sugar is no longer excluded from tariff reductions under regional trade agreements that have been concluded between the EU and third countries in recent years.

German processors initially welcomed the change. The most competitive processors from Germany, Benelux and France wanted to expand production as WTO limitations on EU sugar exports also ended with the sugar quota system. The majority of sugar plants are located in Germany, France, and Poland, and the majority of sugar quotas were controlled by companies headquartered in Germany, France, the Netherlands and the United Kingdom. The sugar quota system in the European Union had been operated by only a few very powerful operators: Südzucker, Nordzucker, Tereos, ABF, Pfeifer & Langen, Royal Cosun and Cristal Union.

But liberalization came with consequences. 18 EU beet sugar factories have closed since 2017/18. Germany was not spared from this rationalization, with closures affecting smaller plants and forcing growers in some regions to transport beets longer distances.

4. Germany’s Sugar Sector Today: By the Numbers

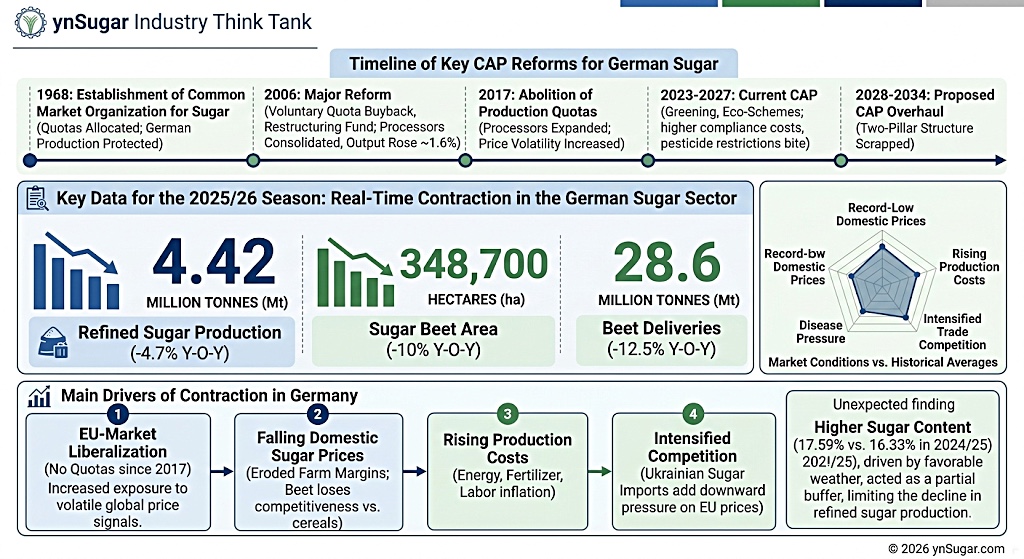

Germany’s sugar industry remains a continental heavyweight, but the latest WVZ data confirm a notable contraction in the 2025/26 marketing year. According to the German Sugar Association (WVZ), Germany’s refined sugar production from beets totaled 4.42 million metric tonnes in the 2025/26 season, down 4.7% from the previous year, amid a 10% reduction in the total sugar beet area.

Specifically, in 2025/26 MY the total sugar beet area amounted to 348,700 hectares, compared to 386,200 hectares in 2024/25 MY. Sugar beet supplies this season decreased to 28.6 million tonnes from 32.7 million tonnes in the previous season. Sugar beet yield decreased by 3%, to 82 t/ha. However, due to favorable weather conditions, the average **sugar content increased from 16.33% to 17.59%**, which partially offset the impact of reduced acreage and lower per-hectare yields.

Table 1: German Refined Sugar Production – Recent Seasons

| Marketing Year | Refined Sugar Production (million tonnes) | Sugar Beet Delivered (million tonnes) | Cultivated Area (ha) | Avg. Yield (t/ha) | Sugar Content (%) |

|---|---|---|---|---|---|

| 2023/24 | 4.22 | 29.81 | ~364,000 | 81.8 | 16.4 |

| 2024/25 | 4.64 | 32.70 | 386,200 | ~85 | 16.33 |

| 2025/26 | 4.42 | 28.60 | 348,700 | 82 | 17.59 |

| YoY Change | −4.7% | −12.5% | −10.0% | −3.0% | +1.26 pp |

Sources: WVZ, Reuters, Sugaronline, Selina Wamucii

This contraction follows the bumper 2024/25 campaign, when Germany’s sugar industry produced 4.64 million metric tonnes of refined beet sugar—up from 4.22 million tonnes the previous season. The dramatic swing between back-to-back seasons illustrates how tightly German output is now coupled to volatile global price signals in the post-quota era.

5. The 2025/26 Contraction: Why German Output Is Falling

The European sugar market is currently going through difficult times: domestic sugar prices have fallen to record lows—as they have elsewhere in the world—while production costs are rising. The EU sugar beet sector is set to contract in the 2025/26 marketing year due to falling sugar prices, rising production costs, and market oversupply. Total EU beet sugar production is projected at 14.8 MMT, down 9 percent from 16.3 million in 2024/25. The harvested area was expected to shrink by 10 percent to 1.35 million hectares, with significant declines in France and Germany, the bloc’s largest producers. A nearly 7 percent drop in sugar beet area was anticipated in Poland, while Belgium and the Netherlands forecast even sharper reductions. Eastern European growers are reconsidering sugar beet planting due to unfavorable margins and competition from alternative crops.

The price collapse has hit Germany’s flagship processor hard. Suedzucker’s operating results declined by 63% in the 2024/25 fiscal year to EUR 350 million (US$392.6 million), due to the weak performance in the sugar segment amid a sharp decline in prices.

Table 2: Drivers of the 2025/26 Contraction in Germany

| Factor | Impact on German Sugar Sector |

|---|---|

| Sugar price collapse (~−35% YoY) | Eroded farm margins; beet crop loses competitiveness vs. cereals |

| Rising input costs | Energy, fertilizer, and labor inflation squeeze processors |

| Reduced plant protection products | Disease pressure (Cercospora, SBR, Stolbur) increases yield risk |

| Ukrainian sugar imports | Add downward pressure on EU prices |

| Pending Mercosur, Mexico, India FTAs | Future tariff competition expected |

| 10% drop in planted area | Direct production decline confirmed at 4.42 Mt for 2025/26 |

Notably, despite all these headwinds, the higher sugar content (17.59% vs. 16.33%) driven by favorable weather has acted as a partial buffer—keeping the production decline (−4.7%) much smaller than the area decline (−10%) would otherwise have implied.

6. CAP 2023–2027 and the Coming 2028 Reform

The current CAP framework is itself in flux. The Common Agricultural Policy (CAP) for 2023–2027, adopted in 2021, has been under review since March 2024 following farmer protests over administrative burdens and pricing issues. In May 2024, the European Commission adopted amendments to simplify the policy, aiming to reduce red tape.

Looking further ahead, the EU is preparing an even more fundamental restructuring. The Commission has proposed reform to the Common Agricultural Policy (CAP) as part of its 2028–2034 EU budget. The proposal marks a major reform, scrapping the CAP’s two-pillar structure and merging farm funding into broader National and Regional Partnership Plans. The new CAP aims to prioritize performance-based spending, tighter targeting of income support, and greater Member State control. While environmental objectives remain, implementation would shift largely to national discretion.

For German beet growers, this means greater uncertainty. The EU sugar sector continues to adapt to structural, market, and policy pressures. Reduced access to plant protection products, rising input costs, declining margins, and persistent pest and disease pressures illustrate the ongoing agronomic challenges. Global competition, particularly from Ukraine, combined with potential future trade liberalization with Mercosur, Mexico, India, and Indonesia, alongside CAP reforms and broader EU policy frameworks, influence planting and production decisions.

7. Germany’s Position in Global Sugar Trade

Despite domestic headwinds, Germany retains a powerful export footprint. Germany has historically been a major exporter of raw sugars and processed confectionary. In 2024, the export value reached $4.9 billion, the fifth highest worldwide, according to Trading Economics. Germany, Brazil, India, Thailand and France together supplied 68.7% of the global raw sugar export value in 2024. Raw sugar exports by Germany in the 2024-25 season amounted to over $1.197 billion or a 3.2% share globally.

In terms of unit value sales, sugar from Germany is pretty expensive in the international market. In 2024, for example, it shipped at $792 a tonne, behind Mexico’s $929/tonne, among the top 12 exporters. This high rate helped Germany attain a trade surplus of $706.5 million in sugar versus imports.

The main EU sugar exporting Member States are France, Germany, Poland, the Netherlands, and Belgium, with the primary destinations being the UK, Israel, Türkiye, Sri Lanka, and Ghana. EU sugar exports to the UK stopped in January 2021 following Brexit, but exporters quickly adapted to the new rules, allowing for an immediate recovery.

8. Structural Outlook: A Slow but Steady Decline

The longer-term picture suggests German output will continue to face downward pressure in line with broader EU trends. The 2025/26 contraction—now confirmed by WVZ at 4.42 million tonnes—aligns with a broader downward trend in EU sugar beet area and yields, as reduced availability of plant protection products and increasing production uncertainties continue to weigh on the sector.

Demand-side pressures compound the supply-side challenges. Trends, based on balance sheet data and using production and trade figures, indicate a structural decline in EU sugar consumption, reinforced by demographic factors such as a projected decrease in the EU population and continued reductions in per capita sugar intake. The European Commission anticipates an annual decrease of 0.2 percent through 2035.

Table 3: Timeline of CAP Sugar Policy and German Impact

| Year | Policy Event | Effect on German Sugar Sector |

|---|---|---|

| 1968 | Common Market Organization for Sugar established | Quotas allocated; German production protected |

| 2003 | Brazil files WTO challenge | Triggered review of EU export subsidies |

| 2006 | Major reform: voluntary quota buyback, restructuring fund | German processors consolidated; output rose ~1.6% |

| 2010 | End of restructuring period | German industry emerged dominant in EU |

| 2017 | Production quotas abolished | Processors expanded; price volatility increased |

| 2023–2027 | Current CAP (greening, eco-schemes) | Higher compliance costs; pesticide restrictions bite |

| 2024 | CAP simplification amendments | Reduced administrative burden after farmer protests |

| 2024/25 | Bumper harvest at 4.64 Mt | Coincided with 35% price drop; Südzucker profits −63% |

| 2025/26 | Area drops 10% to 348,700 ha | Production confirmed at 4.42 Mt (−4.7% YoY) |

| 2028–2034 | Proposed CAP overhaul | Two-pillar structure to be scrapped |

Conclusion

The arc of EU sugar policy under the CAP—from rigid quotas to full liberalization and now to a performance-based, climate-conscious framework—has placed Germany in a paradoxical position. As Europe’s most efficient beet producer, Germany initially gained from each successive reform, expanding output and consolidating processing capacity. Yet the very liberalization that enabled this growth has also exposed German farmers and processors to global price volatility, cheaper competing imports, and tightening environmental rules.

The newly confirmed 2025/26 figures crystallize this exposure: with refined sugar production at **4.42 million tonnes (−4.7%), beet area at 348,700 hectares (−10%), and beet deliveries at 28.6 million tonnes (−12.5%)**, the German sugar sector is contracting in real time. Only a remarkable rise in sugar content—from 16.33% to 17.59%, courtesy of favorable weather—prevented the decline from being far steeper. With domestic prices at record lows, production costs climbing, and Südzucker’s profits already collapsed by 63%, the German sugar sector now faces a familiar question that has shadowed it since 2006: how to remain competitive in a market where CAP support is increasingly decoupled, environmental demands are rising, and the world’s most efficient cane producers are only a free-trade agreement away.

For more detailed analysis on international market trends and structural shifts, stay updated with the latest insights in our Global Sugar Insights series.

Disclaimer: The data and analysis provided in this article are based on reports from the German Sugar Association (WVZ), the European Commission, and various market intelligence sources available as of May 2026. While every effort has been made to ensure accuracy, the sugar market is subject to rapid volatility. This report is for informational purposes only and does not constitute financial or investment advice. ynSugar.com is not liable for any trading decisions made based on this information.