On the global map of sugar trade, the Brazil sugar industry is a name that simply cannot be overlooked. As the world’s largest producer and exporter, Brazil sets the benchmark for global price dynamics and supply chain efficiency.Decoding Brazil’s Sugar Industry: How the World’s Largest Producer Wins

Heading into the 2025/26 crushing season, this South American sugar giant’s dominant position has not only held firm but grown even stronger. Flat, fertile land, a natural climate tailor-made for sugarcane, a dual-track sugar-and-ethanol production system, near year-round operations, and crushing capacity unmatched anywhere else in the world — together these factors have made Brazil the industry benchmark for efficiency, scale, and policy coherence.

This article aims to take a closer look at the inner workings of Brazil’s sugar industry — from the cane fields to the mills, all the way up to the policy framework — to understand what exactly puts the country so far out of reach of its competitors.

1. A Record-Breaking 2025/26 Season

The 2025/26 marketing year (April 2025 through March 2026) once again confirmed Brazil’s grip over global sugar supply.

According to the latest figures from Brazil’s National Supply Company (Conab), sugar output for the season topped 44 million tonnes, accounting for more than a quarter of global production. On the export side, Brazil shipped roughly 35.7 million tonnes of sugar to 150 countries across six continents, generating around USD 14 billion in foreign exchange earnings from this single commodity alone.

The geography behind these numbers is genuinely unique.

The state of São Paulo is the heartland of Brazilian sugar, producing somewhere between 52% and 60% of the country’s total output. Sitting between 20° and 24° south latitude, the state enjoys ample sunshine and well-distributed rainfall during the growing season, while the dry stretch from April to November opens an ideal window for harvest and crushing. This dry period is more than just a weather story: arid conditions raise the sucrose content of the cane (measured as Total Recoverable Sugar, or ATR, per tonne of cane) and significantly ease mechanized harvesting operations.

2. Cane Cultivation and Production: Near-Total Mechanization

One of the “quiet revolutions” in Brazil’s sugar sector has been the consolidation of cane farming at scale.

The traditional model — thousands of smallholders operating independently and selling cane to local mills — has given way to an industrialized supply chain dominated by integrated sugar groups. Today, mechanization rates across Brazilian cane production run between 85% and 100%, with manual labor confined to only a handful of niche tasks in planting and harvesting.

In the 2025/26 season, harvested cane area in Brazil reached approximately 8.95 million hectares. Large contiguous plantations combined with high mechanization have reshaped the productivity curve of the entire industry: labor output has risen sharply, production cycles have smoothed out, and the boom-and-bust “big year, small year” swings that plague sugar industries in many other developing countries have been markedly suppressed.

The end result: lower unit costs, more stable returns for cane growers, and more reliable feedstock supply for the mills.

Pricing by Quality: The TRS System

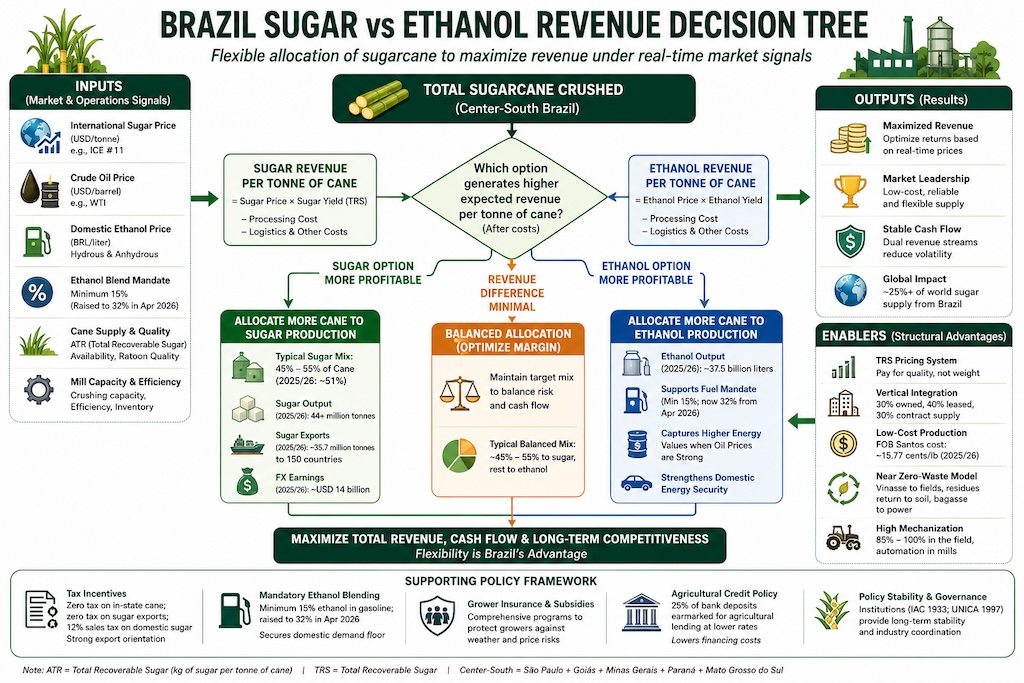

In Brazil, cane is not priced by weight but by sugar content. The entire pricing mechanism is built around Total Recoverable Sugar (TRS), with adjustment factors layered on top to reflect domestic and international sugar and ethanol prices. The logic is simple but powerful: the higher the quality and sugar yield of your cane, the higher the price you receive.

This “pay-for-quality” approach delivers two important effects. First, it ties grower incentives tightly to downstream quality requirements. Second, planted area can adjust dynamically in response to international sugar prices. More importantly still, it gives Brazil a “shock absorber” no other country possesses — the dual-track production of sugar and ethanol, allowing mills to flexibly switch the end-use of cane based on the relative profitability of the two products.

That flexibility was on full display in 2025/26. In a typical year, Center-South mills allocate roughly 45% to 55% of their cane to sugar, with the rest going to ethanol.

For 2025/26, the sugar mix came in around 51%, slightly above the historical average, mainly because international sugar prices early in the season looked more attractive than domestic ethanol returns. Ethanol production for the year totaled roughly 37.5 billion liters — a reminder that Brazilian mills are, at heart, “food plus energy” platforms with two revenue streams.

In China, by contrast, sugar is not treated as a simple “food product.” Across newspapers and online media, sugar is consistently framed as a strategic reserve commodity — and rightly so, given that it forms a critical pillar of the food-processing industry.

The dual-revenue, or dual-track, system means Brazil’s actual sugar supply to the global market is never determined by harvest size alone. It depends on the sugar-to-ethanol price ratio at any given point in the crushing season.

Put differently: when crude oil prices are high enough to make ethanol competitive, even a bumper cane crop can translate into shrinking sugar output. Conversely, when oil prices weaken — for instance, with WTI hovering between USD 62 and USD 66 per barrel in Q1 2026 — more cane gets diverted toward sugar production.

3. The World’s Lowest-Cost Sugar Producer

According to estimates from consultancy Pecege, the average FOB Santos production cost for Brazilian raw sugar in 2025/26 came in at roughly 15.77 cents per pound. On this metric, no other producing country can match Brazil.

Brazilian sugar production costs break down into two main components: mill processing costs (equipment depreciation, labor, taxes, and logistics) and cane feedstock costs — with cane consistently the single largest expense.

Vertical Integration: The Anchor of Cane Costs

The reason Brazil can keep feedstock costs firmly in check comes down to deep vertical integration.

Cane supply at Brazilian sugar groups typically flows through three channels: about 30% from company-owned and company-operated plantations directly attached to mills and ethanol distilleries; roughly 40% from cane grown on leased land; and the remaining 30% sourced through contracts with third-party growers. Owning a meaningful slice of plantations gives sugar groups a stable “price anchor” and a guaranteed supply floor — a structural advantage that independent refiners elsewhere in the world simply do not have.

At the Mill: Automation and Continuous Processing

Step inside a Brazilian sugar mill and the level of automation is immediately apparent.

Plant-wide intelligent control networks monitor equipment in real time, eliminating the need for fixed-station operators. This has enabled larger equipment scales while supporting leaner staffing. On the process side, continuous crystallization and pan-boiling systems have largely replaced traditional batch crystallizers, shrinking the building footprint while cutting labor and energy use.

At the same time, nearly 90% mechanization in the field, paired with remote crop monitoring, allows cost advantages to compound at every stage of the operation.

It’s worth noting that Brazilian sugar processing technology is broadly similar to China’s, but the differences in technology choices and equipment configuration are precisely where cost control is won or lost.

4. Squeezing Value from the Whole Chain: Turning Waste into Profit

If there is one aspect of Brazil’s sugar industry that deserves particular study, it is the near “zero-waste” model of integrated cane utilization.

The vinasse — the alcoholic stillage left over from ethanol fermentation — is returned in full to the cane fields as fertilizer.

Rich in minerals and organic matter, vinasse cuts chemical fertilizer use, supports cane growth, prevents potential water pollution, and directly lowers production costs — all in one stroke. Cane leaves and tops are similarly returned to the fields at close to 100%. Used in tandem with vinasse, they substantially improve soil moisture retention and boost the cane’s drought resistance — a feature whose value is becoming ever more important in an era of intensifying climate volatility.

Brazil’s fuel ethanol story dates back to the first oil crisis of the 1970s.

It was Brazil that first scaled up sugarcane ethanol fuel as a substitute for gasoline in passenger vehicles, becoming one of the earliest countries in the world to commercialize fuel ethanol technology.

Today, Brazil is the world’s second-largest fuel ethanol producer, with roughly half of its annual cane crop channeled into ethanol production. The bagasse left after crushing is fed to biomass power plants, where the renewable electricity generated not only meets the mills’ own needs but often leaves a surplus that is fed into the public grid.

5. Governance and Industrial Policy

Brazil’s sugar industry didn’t reach today’s heights through market forces alone.

A robust institutional framework has played a critical role from the outset. As far back as 1933, Brazil established the Brazilian Sugar and Alcohol Institute to provide unified oversight of the cane sugar and ethanol industries.

In 1997, the Brazilian Sugarcane Industry Association (UNICA) was founded. Today, it is the country’s largest organization in sugar, ethanol, and bioenergy, playing a leading role in industry consolidation and external advocacy.

In terms of specific policy instruments, four stand out:

Differentiated cane taxation. State governments impose no tax on cane grown within their own borders, but levy a tax of more than 9% on cane brought in from other states. Domestically sold sugar is subject to a uniform 12% sales tax, while exported sugar is fully tax-exempt. This pronounced “export-friendly” tilt explains much of Brazil’s aggressive posture in the international sugar market.

Mandatory ethanol blending. The federal government sets the ethanol-to-gasoline blending ratio. Mills must dedicate at least 15% of their output to ethanol production; above that floor, they are free to allocate cane between sugar and ethanol based on market economics.

In April 2026, President Lula confirmed an increase in the gasoline ethanol blend to 32%.

Grower insurance and subsidy schemes. A comprehensive support program is specifically designed around the risks faced by cane farmers, with clearly codified subsidy rules. This provides institutional protection against weather and price shocks.

Agricultural credit policy. The government requires commercial banks to direct at least one-quarter of their deposit base to agricultural lending, at interest rates below standard commercial benchmarks. For capital-intensive cane operations, this “cheap credit” is an unobtrusive but extremely important competitive edge.

Key Policy Instruments

| Policy Tool | Mechanism | Strategic Effect |

| Tax Incentives | Zero tax on sugar exports vs 12% domestic sales tax | Strong export orientation |

| Mandatory Blending | 32% ethanol in gasoline (as of April 2026) | Secures domestic demand floor |

| Credit Policy | 25% of bank deposits earmarked for ag-lending | Lowers financing costs for expansion |

| TRS Pricing | Settlement based on sucrose content | Aligns grower incentives with quality |

6. The 2026/27 Outlook

Looking ahead to the 2026/27 season, the market broadly expects a modest pullback.

Consultancy Datagro projects output in Brazil’s main producing region (Center-South) at around 43.2 million tonnes — below 2025/26 — primarily because the 2024 droughts and fires degraded ratoon cane quality, weighing on yields. At the same time, mills are recalibrating their product mix, lowering the sugar mix and dialing up ethanol output to capture the premium offered by rising energy prices.

This strategic pivot will take effect with the new crushing season starting in April 2026.

For global buyers, the takeaway is increasingly clear: Brazil’s sugar machine is not just enormous in scale — more importantly, it offers structural flexibility, deep vertical integration, and consistent policy support.

It is precisely these qualities that have kept Brazil at the top of the sugar export rankings year after year. And it is precisely for these reasons that anyone serious about studying commodity markets needs to genuinely understand the inner logic of the Brazilian model.

FAQ: Frequently Asked Questions

1. How much sugar does Brazil produce annually? In the 2025/26 season, the Brazil sugar industry produced over 44 million tonnes, accounting for more than 25% of global output.

2. Why is Brazilian sugar so cheap compared to other countries? The competitive edge comes from 85-100% mechanization, deep vertical integration where mills control their own cane supply, and a “zero-waste” model that generates revenue from electricity and ethanol.

3. What is the current ethanol blending ratio in Brazil? As of April 2026, the mandatory ethanol-to-gasoline blending ratio in Brazil has been increased to 32%.

4. Which region in Brazil produces the most sugar? The state of São Paulo is the heart of the industry, contributing between 52% and 60% of the country’s total sugar production.

Data Transparency and Sources

This report is compiled by the YnSugar Analysis Team using the latest consolidated data from Conab (National Supply Company), UNICA (Sugarcane Industry Association), and Pecege/ESALQ research models (Updated May 2026).

Executive Summary

Brazil has cemented its position as the undisputed powerhouse of the global sugar market. With a record 2025/26 season, unmatched cost efficiency (15.77 cents/lb), and a strategic pivot toward a 32% ethanol blend, the Brazil sugar industry offers a level of structural flexibility that remains difficult to replicate. For global buyers and analysts, understanding the “Brazilian model” is no longer optional—it is essential.

Meet the YnSugar Team at Guangxi Sugar Expo 2026

As part of our commitment to global sugar industry analysis, the YnSugar team will be present at the 19th Guangxi International Sugar Industry Technology & Smart Equipment Exhibition. This is the premier event to understand China’s technological leap in sugarcane processing.

Plan Your Visit:

-

When: July 24-26, 2026

-

Where: Hall D, Level 2, Nanning International Convention & Exhibition Center

-

Inquiries: [email protected]