China starch sugar market 2025 data reveals a complex period of adjustment. While industrial applications provided a stable foundation for specific products, the broader sector grappled with a transition in demand patterns and a significant shift in the competitive landscape relative to white sugar. (April 17, 2026 — YnSugar Research)

Supply and Demand: New Energy and Chemicals Drive Growth

Market activity in 2025 was highlighted by a notable increase in Crystalline Glucose production. This trend was largely decoupled from the traditional food sector, finding its primary support in China’s rapidly expanding new energy and chemical industries. For other starch sugar categories, production levels remained largely consistent with the previous year or saw only marginal increments.

Price Performance: Seasonal Slump and Weak Consumption

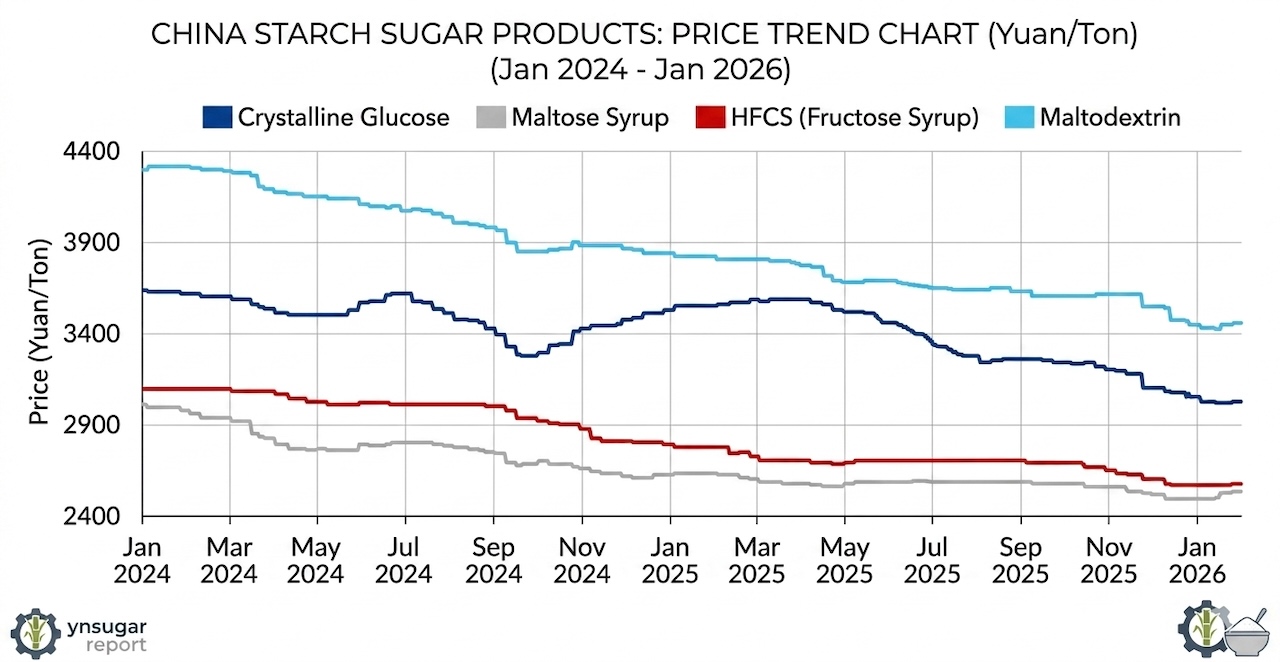

The 2025 calendar year saw a general downward trend in transaction prices across the starch sugar spectrum. Following the Lunar New Year, a period of heightened inventory pressure emerged as demand from the core food and beverage sectors entered a seasonal trough.

-

Crystalline Glucose: Average factory prices settled at 3,407 Yuan/ton, a 3% decrease from 2024. By year-end, prices stabilized near the break-even point.

-

Maltose Syrup: Following a “fall-rise-fall” trajectory, prices averaged 2,585 Yuan/ton, representing a 7.5% year-on-year decline.

-

HFCS F55 (Fructose Syrup): Price movements were relatively contained, yet the annual average fell to 2,705 Yuan/ton, a 9.78% drop from the 2024 level of 2,998 Yuan/ton.

-

Maltodextrin: Faced persistent downward pressure due to shrinking domestic demand and product replacement, with average prices sliding 9.34% to 3,704 Yuan/ton.

Profitability Dynamics: The Impact of Raw Material Costs

Profitability across the sector faced headwinds in 2025 as selling prices struggled to keep pace with raw material fluctuations. Even as corn (maize) prices trended upward during specific windows, the weak downstream demand prevented producers from passing these costs along.

-

Glucose: Average profit reached 282 Yuan/ton, a 22.6% decrease from the previous year. The second half of the year was particularly challenging, with brief periods of net losses.

-

Maltose Syrup: Annual average profit plummeted by 89.7% to just 8 Yuan/ton.

-

HFCS: Margins narrowed by 75.8%, averaging 52 Yuan/ton for the year.

-

Maltodextrin: Average profit fell 58.9% to 239 Yuan/ton, though a slight recovery was noted in the second half of the year as input costs moderated.

Substitution Dynamics: The Narrowing Gap with White Sugar

One of the most critical developments in late 2025 was the narrowing price spread between white sugar and High Fructose Corn Syrup (HFCS). Historically, a gap of 1,500–2,000 Yuan/ton serves as the psychological and economic threshold for industrial substitution.

By late 2025, this spread had contracted to approximately 2,000 Yuan/ton, a reduction of 500 Yuan since the start of the year. As white sugar prices continued their descent, the incentive for manufacturers to switch to starch-based alternatives diminished. In certain fermentation and chemical sectors, the market witnessed a rare reversal, with white sugar reclaiming market share previously held by starch sugars.

Ynsugar Outlook: A Rebalancing Act in 2026

The 2025 data signals a major rebalancing in China’s sweetener complex. The era of starch sugar’s easy gains through “price-gap substitution” is facing a reality check. As the spread toward white sugar nears the critical 1,500 Yuan mark, starch sugar producers are no longer operating in a vacuum.

At Ynsugar, we expect 2026 to be defined by a focus on operational efficiency and the exploration of high-value industrial niches. The ability of starch sugar to maintain its footprint in the food sector will now depend heavily on the price floor of the global and domestic white sugar markets.