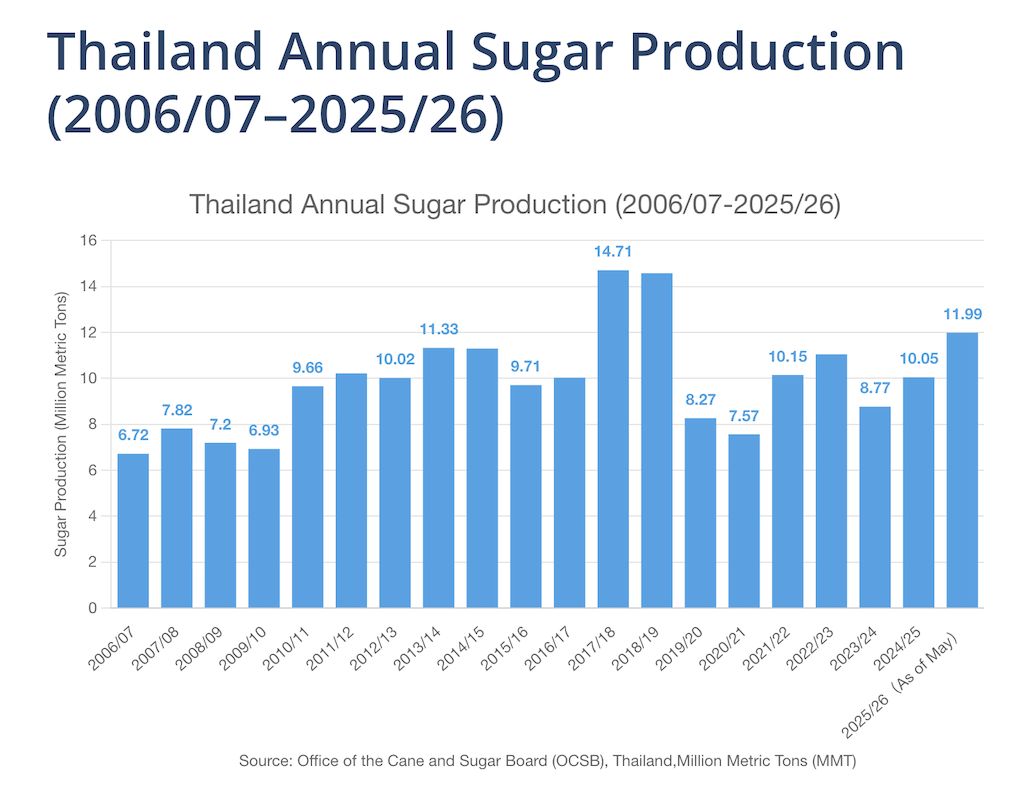

Thailand’s sugar production for the 2025/26 crushing season has reached nearly 12 million tonnes, according to the latest figures from the Office of the Cane and Sugar Board (OCSB), even as government officials warn of mounting oversupply risks in the second half of the year.

Strong Production Momentum

Data released by the OCSB show that as of May 3, 2026, cumulative sugarcane crushed during the 2025/26 season totalled 105.86 million tonnes. Sugar content in the cane averaged 12.94 percent, while the yield rate stood at 11.333 percent, translating to a total sugar output of 11.997 million tonnes.

For a detailed historical perspective, you can refer to the Thailand sugar production statistics 2006-2026.

A breakdown of production by type shows raw sugar leading the mix at 9.16 million tonnes, followed by white sugar at 2.36 million tonnes and refined sugar at 474,000 tonnes. Looking ahead, favourable rainfall and expanded planting areas have lifted Thailand’s full-season cane crush expectations to approximately 106 million tonnes — a significant year-on-year increase of nearly 15 percent.

Warning of a Domestic Glut

Despite the robust output, Thailand’s Trade Policy and Strategy Office (TPSO) has urged the country’s sugar industry to prepare for headwinds in the latter half of the year. TPSO Director-General Nantapong Chiralerspong told local media that rising sugarcane and sugar output — both domestically and globally — combined with Indonesia’s push toward sugar self-sufficiency, could create a surplus in the Thai market.

He called on industry stakeholders to align production with shifting market demand, diversify export destinations, and accelerate the transition toward bio-energy and bio-based products as part of a broader move up the value chain.

Export Landscape Under Pressure

Thailand ranked as the world’s second-largest sugar exporter in 2025, trailing only Brazil, with shipments of 5.5 million tonnes generating more than USD 2.6 billion in revenue.

Indonesia was by far the largest buyer, accounting for USD 715 million — more than 27 percent of Thailand’s total sugar export earnings. Other key markets included Cambodia, South Korea, and the Philippines. However, Jakarta’s drive toward sugar self-sufficiency is expected to significantly reduce Indonesian demand for Thai sugar going forward.

TPSO identified two principal risks for the sector in the second half of 2026: a potential domestic oversupply and shrinking offtake from Indonesia. Expanding output from other major producers, notably India and Brazil, is also likely to exert downward pressure on global sugar prices.

Against this backdrop, TPSO is positioning the transition to a bio-economy model — encompassing bioethanol, bioplastics, and other higher-value derivatives — as a strategic imperative for Thai producers seeking to insulate themselves from commodity market volatility and reduce their reliance on a narrowing pool of traditional export buyers.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute financial or investment advice. While we strive for accuracy based on official reports from the OCSB and TPSO, market conditions are subject to change. Readers should conduct their own research before making any business decisions based on this data.