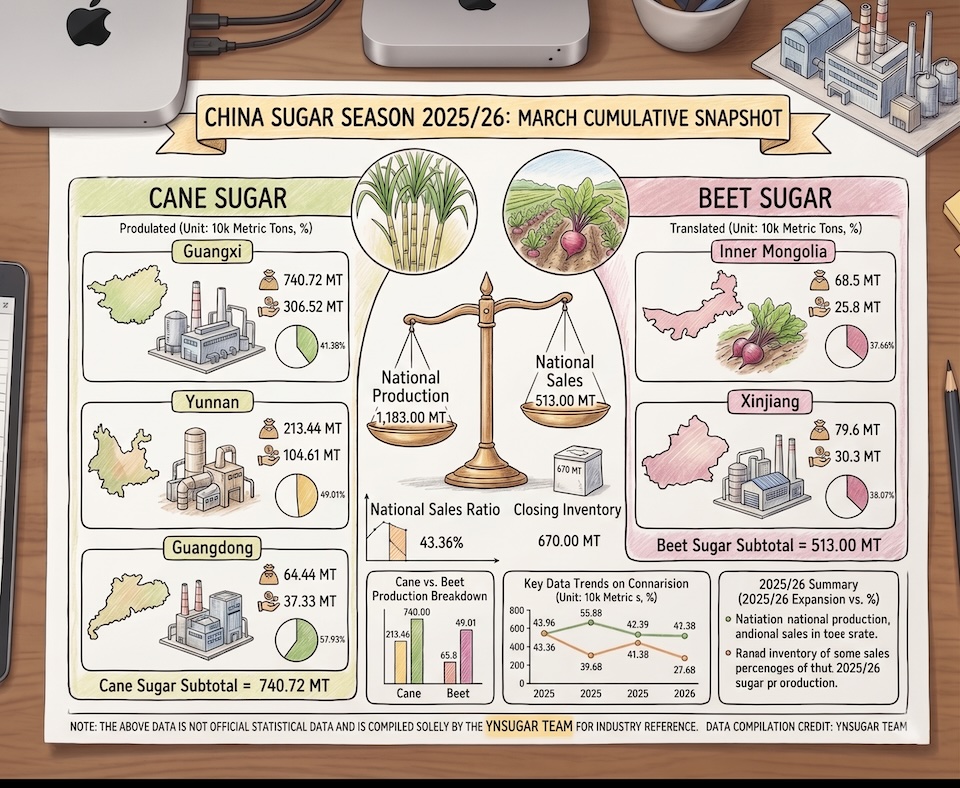

Cumulative data as of the end of March 2026 | Unit: 10,000 Metric Tons, %

| Region / Category | Production Volume | Volume Sold | Sales Ratio (%) | Closing Inventory |

| National Total | 1,183.00 | 513.00 | 43.36% | 670.00 |

| Cane Sugar Total | 1,027.94 | 453.32 | 44.10% | 574.62 |

| – Guangdong | 64.44 | 37.33 | 57.93% | 27.11 |

| – Guangxi | 740.72 | 306.52 | 41.38% | 434.20 |

| – Yunnan | 213.44 | 104.61 | 49.01% | 108.83 |

| Beet Sugar Total | 155.06 | 59.68 | 38.49% | 95.38 |

| – Inner Mongolia | 68.50 | 25.80 | 37.66% | 42.70 |

| – Xinjiang | 79.60 | 30.30 | 38.07% | 49.30 |

Note: The above data is not official statistical data and is compiled solely by the ynsugar team for industry reference.

Market Overview: As of late March 2026, the cumulative sugar production for China’s 2025/26 crushing season has reached 11.83 million metric tons. The industry has shown steady progress, with 5.13 million tons already entering the commercial channel, representing a national sales ratio of 43.36%.

Key Regional Insights:

-

Guangxi continues to lead the nation’s output, contributing over 7.4 million tons of cane sugar, though its sales ratio (41.38%) currently lags slightly behind the national average.

-

Guangdong shows the highest market activity with a sales ratio of 57.93%, indicating strong immediate demand or efficient regional distribution.

-

Cane Sugar vs. Beet Sugar: Cane sugar remains the dominant pillar of China’s production, accounting for approximately 87% of the total output this season. Beet sugar production in Inner Mongolia and Xinjiang remains stable, with a combined output of 1.55 million tons.

Disclaimer: The information contained in this report is for general informational purposes only. While we strive to provide accurate and up-to-date data, the ynsugar team makes no representations or warranties of any kind, express or implied, about the completeness, accuracy, or reliability of the figures provided. These statistics are based on internal monitoring and industry estimates rather than official government releases. Any reliance you place on such information is strictly at your own risk. In no event will we be liable for any loss or damage arising from the use of this data.

These monthly figures provide a foundation for the broader [China’s sugar market outlook and the steady growth expected in 2025/26].