New data from the Brazil sugarcane harvest shows that the Center-South region processed an estimated 611 million metric tons of sugarcane in the 2025/26 cycle…

YnSugar | Sugar-Energy Sector Analysis & Market Intelligence

Brazil’s Center-South region — the global powerhouse behind roughly 90% of the country’s sugarcane output — processed an estimated 611 million metric tons of sugarcane in the 2025/26 harvest, a modest 1.7% decline from the previous cycle. Despite adverse weather during critical crop development phases, the industry’s operational resilience held firm, largely buoyed by an expansion in harvested area.

These are the key findings from the latest annual ranking released by FG/A, a leading corporate finance and strategy consultancy specializing in Brazil’s sugar-energy sector.

Raízen Holds the Top Spot, but Loses Ground

Raízen retained its position as Brazil’s largest sugarcane processor, with an estimated crush of 70.3 million tons — though this figure represents a significant 10.2% year-on-year decline. The drop was driven by a series of strategic divestments: Raízen offloaded its Leme, Rio Brilhante, and Passa Tempo mills during the season and decommissioned the Santa Elisa unit. Notably, four of the six major M&A transactions recorded in the sector during this period involved Raízen assets.

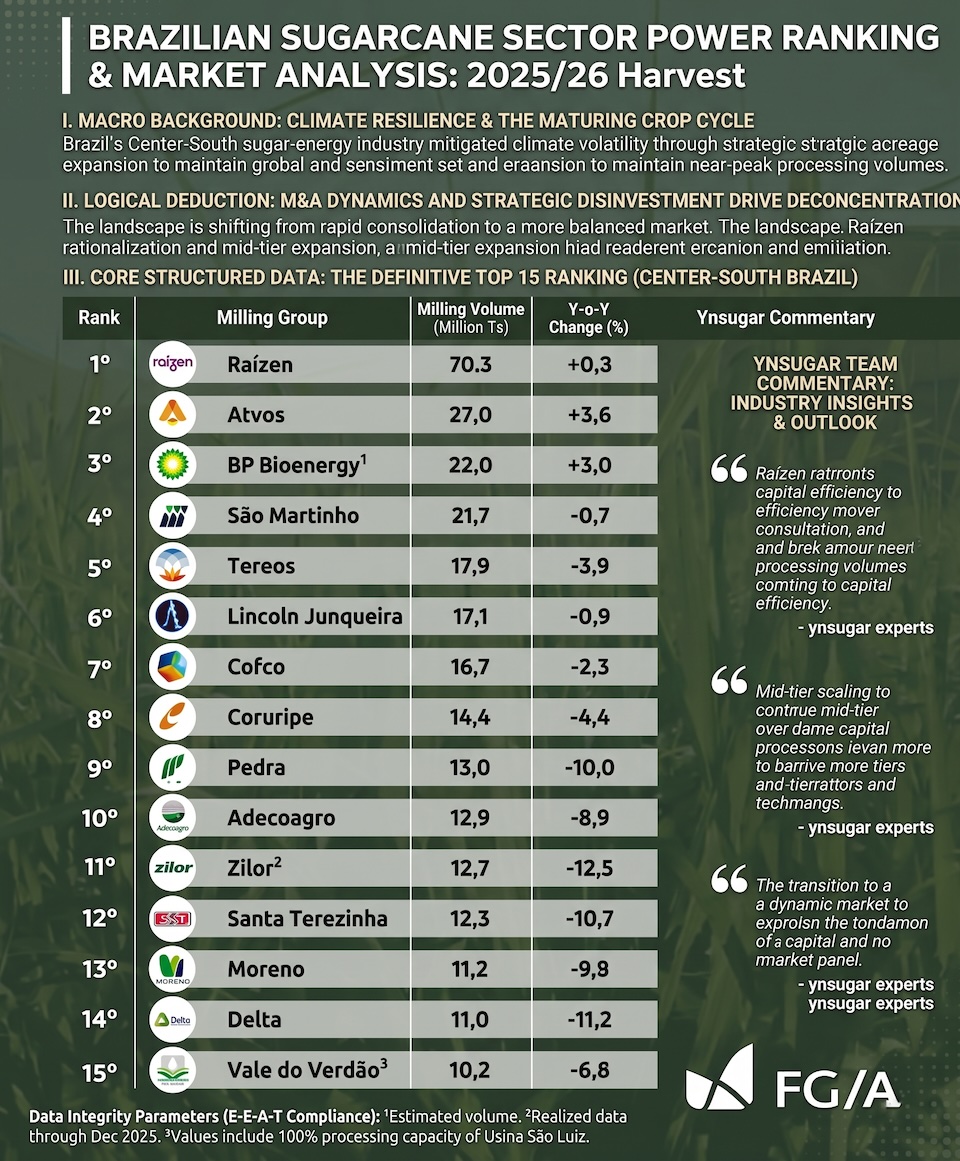

The Top 5 Sugarcane Processors in Brazil (2025/26)

| Rank | Group | Milling (Million Metric Tons) | Y-o-Y Change (%) |

| 1 | Raízen | 70.3 | -10.2% |

| 2 | Atvos | 27.0 | +4.7% |

| 3 | BP Bioenergy | 22.0 | -17.6% |

| 4 | São Martinho | 21.7 | -0.5% |

| 5 | Tereos | 17.9 | -12.6% |

The Full Top 15 at a Glance (Ranks 6–15)

| Rank | Group | Milling (Million Metric Tons) |

| 6 | Lincoln Junqueira | 17.1 |

| 7 | Cofco | 16.7 |

| 8 | Coruripe | 14.4 |

| 9 | Pedra | 13.0 |

| 10 | Adecoagro | 12.9 |

| 11 | Zilor | 12.7 |

| 12 | Santa Terezinha | 12.3 |

| 13 | Moreno | 11.2 |

| 14 | Delta | 11.0 |

| 15 | Vale do Verdão | 10.2 |

Source: FG/A Consultancy. Data realized through December 2025; values estimated considering the April–December milling window.

Market Deconcentration: A Gradual but Clear Trend

One of the most notable storylines of the 2025/26 season is the continued deconcentration of milling volumes among the sector’s biggest players:

-

The top 10 groups now account for 38% of the Center-South’s total crush, down from 40% in 2024/25.

-

The top 5 represent 26%, down from 27%.

-

Looking further back, the top 10 held 42% of milling in 2021/22, and the top 5 held 30% — meaning the sector’s largest operators have shed meaningful market share over just four harvests.

This shift reflects both asset disposals by the largest groups (notably Raízen) and strong performance by mid-tier producers absorbing new capacity through strategic acquisitions and organic growth.

Winners and Losers: Who Grew, Who Shrank?

Biggest Gainers

-

Zilor led all top-15 groups with a 20.1% increase in milling, fueled by its strategic acquisition of the Salto Botelho mill.

-

Santa Terezinha grew by 12.8%.

-

Moreno expanded by 10%, climbing into the top 15 at 13th position.

-

Atvos posted a 4.7% rise, outpacing the regional average.

Biggest Decliners

-

BP Bioenergy registered the steepest fall among the majors, with a 17.6% decrease.

-

Tereos dropped 12.6%.

-

Coruripe declined 9.4%, and Vale do Verdão fell 7.3%.

-

São Martinho and Delta were essentially flat, posting marginal decreases of 0.5% and 0.9%, respectively. Pedra, Cofco, and Lincoln Junqueira all finished the harvest with declines exceeding the Center-South regional average.

M&A Activity Continues to Reshape the Landscape

Beyond Raízen’s high-profile divestments, other transactions reshaped the competitive map. Zilor’s incorporation of Salto Botelho directly boosted its ranking. Meanwhile, the Graciano family — previously controllers of the Santa Isabel group — acquired the Diana mill, signaling that family-owned groups remain active dealmakers in Brazil’s sugar-energy space.

These moves reinforce a broader pattern: assets are flowing from the very largest operators toward mid-sized groups eager to scale up, gradually flattening the industry’s concentration curve.

Outlook: Weather Remains the Wild Card for 2026/27

As the sector transitions into the 2026/27 harvest, the primary variable remains the weather. Drier-than-normal conditions weighed on agricultural yields in 2025/26, and the industry’s ability to sustain crush volumes above 600 million tons will depend heavily on rainfall patterns during the current crop development window.

The recovery of sugarcane field productivity — measured in tons of cane per hectare (TCH) — will be the key metric to watch. If weather cooperates, the Center-South could stabilize or even rebound in total milling. If not, the trend of area expansion may reach its limits as a compensating factor.

Disclaimer: The market data, rankings, and analysis provided in this article are based on the annual report published by the Brazilian consultancy FG/A, incorporating realized data through December 2025 and industry estimates. While ynsugar strives to ensure the accuracy and reliability of the shared information, this content is for informational and educational purposes only and should not be construed as financial, investment, or commercial advice for trading in the sugar-energy commodities market.