June 2, 2026 | Sugar & Bioenergy Markets

When global commodity analysts talk about Brazilian sugar production, they almost always mean the Center-South — the powerhouse region that dominates headlines and trade flows. But Brazil’s sugar story doesn’t end there.

The North and Northeast regions are also significant sugarcane producers, and their 2025/26 harvest season is only now drawing to a close, adding millions of tons to the country’s total output that often goes unnoticed in international coverage.

North and Northeast: A Season Shaped by Tariffs and Weather

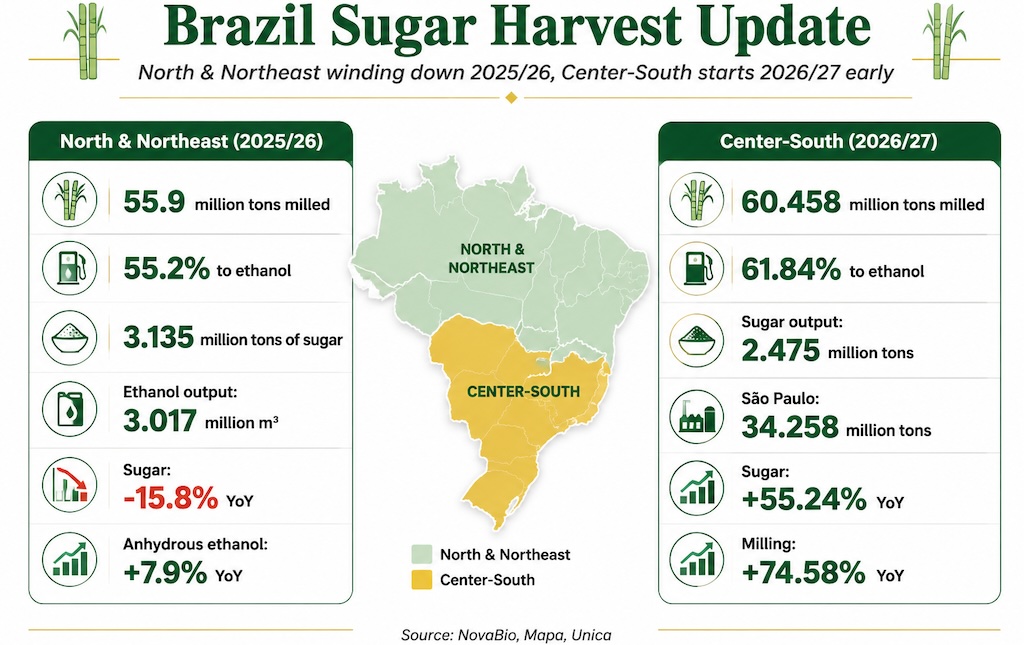

According to data from the Association of Sugar, Ethanol and Bioenergy Producers (NovaBio), compiled from official figures provided by Brazil’s Ministry of Agriculture, Livestock and Supply (Mapa), cumulative sugarcane milling in the North and Northeast reached 55.9 million tons as of April 30, 2026 — down 2% from the same point in the prior season.

Of that total, 55.2% of all processed cane was directed to ethanol production, a notably higher biofuel share compared to previous years. Sugar output from the two regions totaled 3.135 million tons, representing a 15.8% decline year-on-year.

Breaking it down by region:

-

North: 6.9 million tons milled, down 5.5% from the prior harvest.

-

Northeast: 48.9 million tons milled, down 1.4% year-on-year.

NovaBio CEO Renato Cunha pointed to two converging forces behind the season’s profile: “Producing units favored ethanol due to American tariffs, which reduced the competitiveness of sugar prices, and weather conditions explain the drop in milling,” he said.

In short, U.S. trade policy indirectly pushed more Brazilian cane toward fuel, while drier-than-expected conditions limited overall crush volumes.

Ethanol Output Rises Despite Lower Crush

Even with reduced milling volumes, total ethanol production from the two regions reached 3.017 million cubic meters, well above the 2.239 million cubic meters recorded in the same period of the prior cycle.

-

Anhydrous sugarcane ethanol: 892,800 m³ (+7.9% YoY)

-

Hydrated sugarcane ethanol: 1.392 million m³ (−1.4% YoY)

-

Corn ethanol: 732,000 m³ (637,500 m³ anhydrous + 94,500 m³ hydrated)

Ethanol stocks, however, remain notably tight. As of April 30, total ethanol inventories across all sources stood at 138,000 cubic meters — 23.9% below the same point last year. Hydrated ethanol stocks fell 28.1%, while anhydrous stocks dropped 15.4%.

Cane Quality Has Slipped

One concern underlying the data is raw material quality. The Total Recoverable Sugar (TRS) index fell 6.8% in final products. The ATR (Total Recoverable Sugar per ton of cane) also declined 4.9% versus the prior season. This helps explain why sugar production fell more steeply than the drop in crush volumes alone would suggest.

As of the data cutoff, the North and Northeast had collectively completed 94.7% of their projected milling targets.

Center-South Kicks Off Its 2026/27 Season with a Surge

While the North and Northeast wind down 2025/26, Brazil’s dominant Center-South region kicked off its new 2026/27 harvest on April 1, and early results are striking.

According to Unica, cumulative milling as of May 1 reached 60.458 million tons — a 74.58% surge year-on-year, reflecting both an earlier start and aggressive ramp-up. São Paulo state alone crushed 34.258 million tons, up 87.39% from the same period last year.

-

Sugar Production: Hit 2.475 million tons through May 1, up 55.24% from 1.594 million tons in the prior cycle. São Paulo contributed 1.689 million tons (+75.58% YoY).

-

The Ethanol Shift: Notably, the share of cane allocated to sugar in the Center-South dropped to 38.16% (down from 45.23%). The ethanol share climbed to 61.84% — mirroring the same biofuel-first logic driven by unfavorable sugar price dynamics tied to U.S. tariff pressures.

Key Market Takeaways

Taken together, the two regional pictures paint a nuanced portrait of Brazil’s 2025/26 and 2026/27 seasons. The North and Northeast are closing out a season with lower sugar output but stronger ethanol yields, while the Center-South is opening its new season at a record early pace — yet also prioritizing ethanol over sugar.

For global buyers and traders, the key takeaways are: Brazil’s total sugar supply faces downward pressure from the continued shift toward biofuel production, tight ethanol stocks suggest strong domestic demand absorption, and declining cane quality in the North and Northeast adds further uncertainty to near-term output projections.

Data sources: NovaBio / Brazil Ministry of Agriculture, Livestock and Supply (Mapa); Unica (União da Indústria de Cana-de-Açúcar e Bioenergia)

Global Trade Impact

As Brazil shifts its crushing focus toward domestic ethanol, global sugar flow dynamics are changing rapidly. For detailed insights into how these macro production trends affect top importing markets and pricing, view our complete China Sugar Import Report.

Disclaimer: The information and data contained in this article are sourced from official industry organizations including NovaBio and Unica. ynsugar provides this content strictly for global sugar market analysis, trading reference, and informational purposes. While we endeavor to ensure data reliability, market conditions change rapidly, and this content does not constitute specific investment or commercial trading advice.