This China sugar market outlook report examines the structural shifts reshaping the market across production, imports, consumption, supply-demand balance, and pricing. Drawing on data released by the Market Early-Warning Expert Committee of China’s Ministry of Agriculture and Rural Affairs on June 11, the following analysis provides essential insights.

1. Production: Sustained Expansion

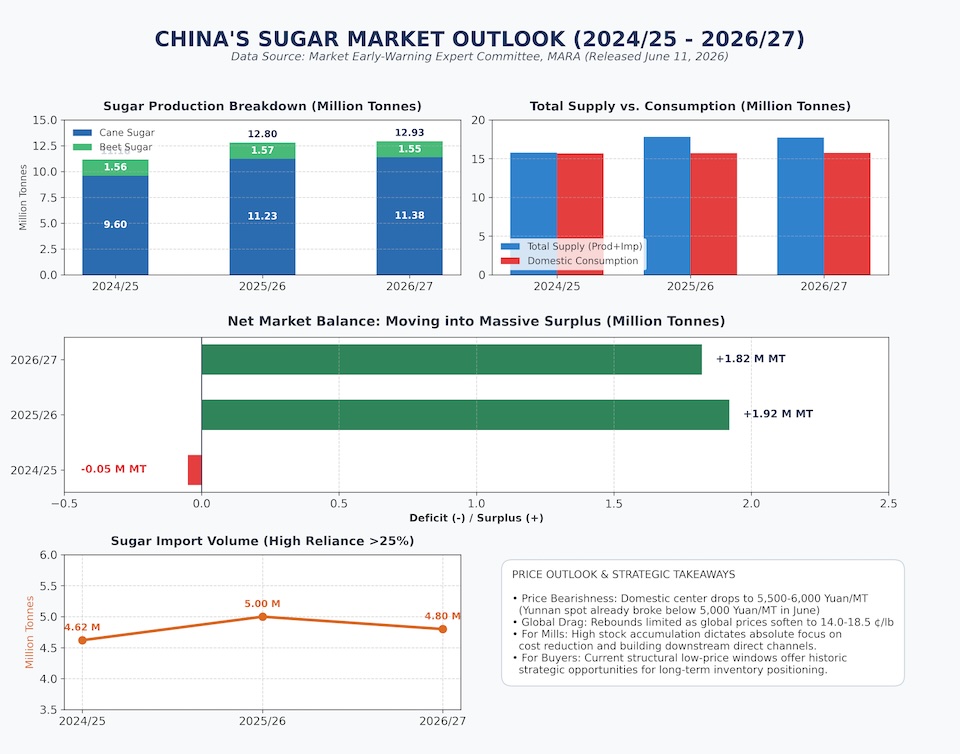

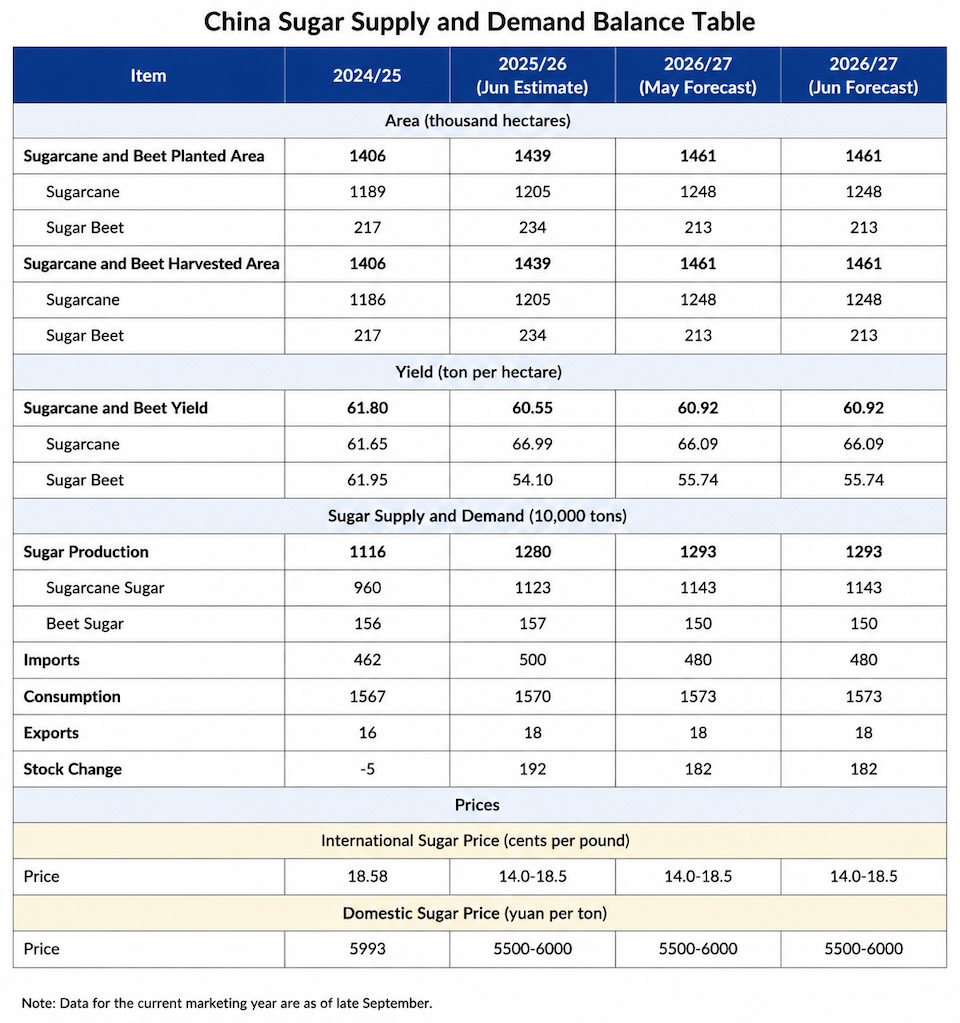

China’s sugar output is set to climb sharply from 11.16 million tonnes in 2024/25 to 12.80 million tonnes in 2025/26—a gain of roughly 14.7%—with the 2026/27 forecast edging slightly higher to 12.93 million tonnes.

The primary engine behind this growth is cane sugar, which surges from 9.60 million tonnes to 11.23 million tonnes, a 17% jump. Beet sugar, by contrast, holds steady within a narrow 1.50–1.57 million tonne range, leaving little room for further upside.

Planted acreage tells a similar story. Sugarcane area expands from 1,189 thousand hectares to a projected 1,248 thousand hectares in 2026/27, while beet acreage slips modestly from 217 thousand to 213 thousand hectares—underscoring a structural tilt toward cane.

Notably, cane yields reach 66.99 tonnes per hectare in 2025/26, a marked improvement over 61.65 tonnes per hectare in 2024/25. This yield gain is the decisive factor driving the explosive rise in total output.

2. Imports: Still Substantial

Import volumes rise from 4.62 million tonnes in 2024/25 to 5.00 million tonnes in 2025/26, before the 2026/27 forecast eases back to 4.80 million tonnes.

This “rise-then-retreat” trajectory aligns closely with the backdrop of expanding domestic production. As China’s home-grown supply capacity strengthens, its reliance on imported sugar is expected to soften gradually.

Even so, imports still account for more than 25% of total supply, signaling that China’s dependence on overseas sugar remains considerable—and that swings in global sugar prices will continue to transmit meaningfully into the domestic market.

👉 Deep Dive: China Sugar Import Report — Analyzing Trade Volumes, Supply Chains, and Market Impacts.

3. Consumption: Steady but Sluggish Growth

Consumption across the three years stands at 15.67, 15.70, and 15.73 million tonnes respectively—an exceptionally slow pace of growth, adding only about 30,000 tonnes annually.

This reflects a mature domestic sugar market, heightened consumer health awareness, and the rising penetration of sugar substitutes. Exports remain at a negligible 160,000–180,000 tonnes, confirming that China has virtually no competitive edge in sugar exports and remains a textbook net importer.

4. Supply-Demand Balance: From Tight to Decisively Loose

This is the single most important shift in the data. The balance swings from a deficit of -50,000 tonnes in 2024/25 (a tight market) to a surplus of +1.92 million tonnes in 2025/26, with the 2026/27 forecast at +1.82 million tonnes.

In other words, the market structure has fundamentally reversed—from a slight shortfall to substantial inventory accumulation. The market now faces clear oversupply pressure.

5. Prices: Persistent Bearish Pressure

Global sugar prices are revised down from 18.58 cents per pound in 2024/25 to a range of 14.0–18.5 cents per pound across 2025/26 and 2026/27, with the midpoint shifting noticeably lower. Domestic prices likewise decline from 5,993 yuan per tonne to a 5,500–6,000 yuan range, with the price center under downward pressure.

On the ground, as of the data’s June 11 release, ex-factory prices at Yunnan mills had broken below 5,000 yuan per tonne, while Guangxi mills were quoting just 5,250–5,350 yuan per tonne.

Against a backdrop of loose supply, a trend-driven price rebound looks unlikely through 2025/26 and 2026/27, and profit margins across the upstream and downstream supply chain are set to compress.

6. Integrated Assessment

| Dimension | Trend | Key Risks |

|---|---|---|

| Production | Sustained expansion, cane-led | Yield volatility, extreme weather |

| Imports | Modest contraction | Shifting price spreads may reverse the import trend |

| Consumption | Low-speed growth | Accelerating penetration of sugar substitutes |

| Inventory | Sharp buildup | Stock pressure could trigger a deeper price decline |

| Prices | Under downward pressure | FX volatility compounded by global price uncertainty |

Taken together, China’s sugar market is entering a new phase defined by ample supply, steady consumption, and elevated inventories. Near-term downward price pressure is significant, cane sugar’s dominance is further entrenched, and while import dependence is easing, it remains at a relatively high level.

For all participants along the supply chain, preparing for price corrections and inventory pressure is essential—while staying alert to potential policy-driven market interventions. For mills, cost reduction, efficiency gains, and the development of downstream channels will form the core of any defensive strategy. For traders and end-buyers, the current low-price window may offer a strategic opportunity for inventory positioning.

Disclaimer: The analysis and market outlook presented in this article are based on public historical data and forecasts released by the Market Early-Warning Expert Committee of China’s Ministry of Agriculture and Rural Affairs. This content is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Sugar market dynamics are subject to rapid shifts driven by weather, international trade policies, and macroeconomic factors. Readers and market participants should conduct independent research or consult with certified professionals before making business decisions. ynsugar and the author assume no liability for any financial losses arising from the use of this information.