Thailand Sugar Production 2026/27: Why Output Could Drop Sharply

Analysis by the ynsugar Research Team | July 2026

Overview: Thailand’s Weight in the Global Sugar Market

Thailand stands as one of the world’s premier cane sugar producers and consistently ranks as the second-largest sugar exporter globally, trailing only Brazil. For international traders, European buyers, and food manufacturers sourcing raw and refined sugar from Asia, shifts in Thai supply have immediate consequences for global pricing and spot availability.

Following a bumper 2025/26 crop, the outlook for the Thailand sugar production 2026/27 season demands close attention. A combination of unfavorable cane economics, aggressive crop switching, and an emerging El Niño points to a significant year-on-year contraction.

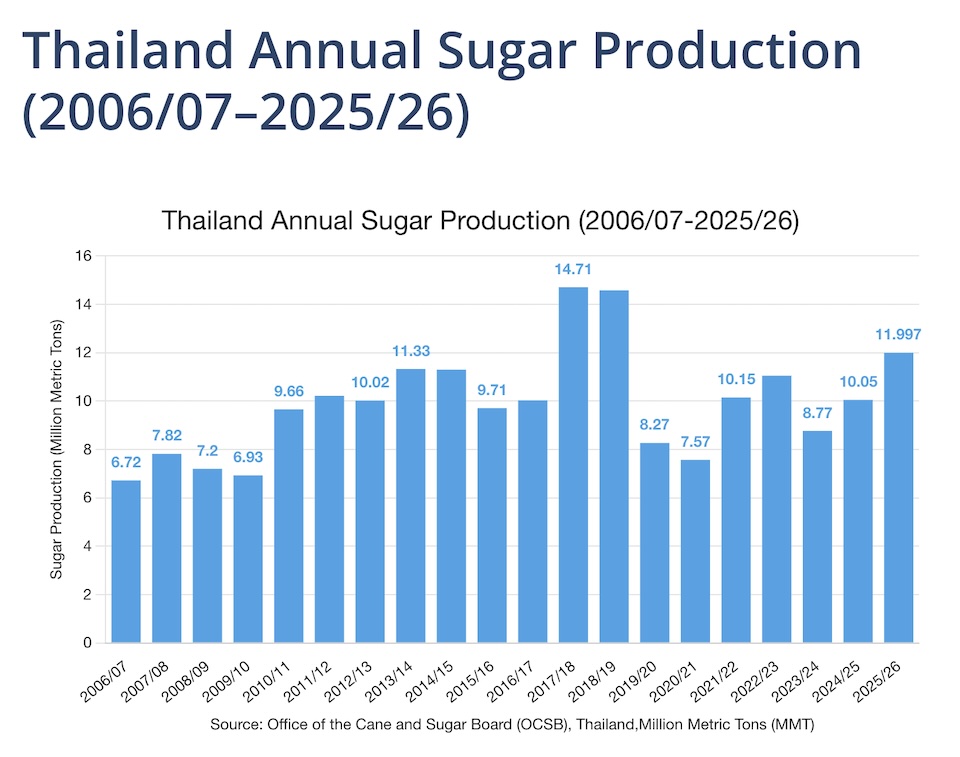

A Record 2025/26 Season Sets a High Base

The context for the upcoming downturn is the exceptionally strong preceding year. In 2025/26, Thailand crushed a robust 105.86 million tonnes of cane, marking a 15.01% year-on-year surge, and produced 11.997 million tonnes of sugar. This final volume represents an increase of 1.946 million tonnes (up 19.37%) and finished roughly 1 million tonnes above the initial 11-million-tonne consensus estimates.

These gains were supported by a brief return of favorable weather. The onset of the La Niña phenomenon during the 2025/26 cycle boosted soil moisture across key growing regions. Official crushing data from the Office of the Cane and Sugar Board (OCSB) confirmed the scale of the crop, reporting a sugar extraction rate of 110 kg per tonne of cane, up from 109.17 kg in 2024/25.

Why the Thailand Sugar Production 2026/27 Outlook Looks Volatile

1. The Lowest Cane Price in Five Seasons

The single most powerful driver behind the looming contraction is financial. The government-set farm-gate cane benchmark for the recent crop was slashed to 890 baht per tonne—a severe 23.28% year-on-year cut, marking the lowest price in five seasons.

Independent assessments from Green Pool confirm that these initial government-set returns fall squarely below the actual cost of production for most smallholders. According to the USDA, sugarcane acreage is forecast to contract heavily as a direct response to this policy-driven squeeze on grower margins.

2. Mass Crop Switching to Cassava

With cane returns deeply squeezed, sugarcane growers in Thailand are actively switching to cassava. Cassava farm-gate prices, hovering firmly in the 2,500–2,800 baht/tonne range, have delivered vastly superior comparative returns. This economic shift is further reinforced by robust external demand, particularly strong import appetites from China.

Market analysts view this as a structural inflection point for the regional agricultural landscape. According to StoneX data, the return of cassava profitability is directly threatening the dominance of sugarcane in core producing provinces. Reflecting this acreage migration, independent consultancies like Datagro estimate a 5% to 6% reduction in Thai cane area for the new cycle. Consequently, total cane crushed is projected to slide toward 86 million tonnes, a steep drop from the 105.86 million metric tons achieved previously.

3. Escalating Production and Labor Pressures

Beyond structural price signals, cost inflation is discouraging active cultivation. The operational cost of producing cane has risen due to rigid environmental regulations on burnt cane. Mills now rely heavily on green cane cutting, which carries significantly higher harvesting and transport costs.

Furthermore, the local migrant labor supply remains heavily strained. Ongoing geopolitical tensions in Cambodia and the civil conflict in Myanmar have severely restricted the seasonal cross-border workforce that Thailand’s agricultural sector traditionally depends on. Severe crop disease pressures, particularly white leaf disease, have compounded the incentive to abandon cane fields.

4. An Emerging El Niño Severe Threat to Yields

The final, unpredictable risk factor is climate. Cumulative rainfall nationwide has hovered roughly 10% below long-term norms just as the Thai cane crop enters its critical elongation (jointing) growth stage.

Meteorological agencies warn that Thailand faces a high risk of strong El Niño conditions extending into early 2027, bringing lower rainfall and abnormally high temperatures. Some regional climate assessments project that overall rainfall across major agricultural zones could drop by as much as 18.6% compared to last year. Because sugarcane requires intensive water volumes during its primary growth phases, this developing dry pattern presents a dangerous downside risk to per-hectare yields.

Production Outlook: How Low Could 2026/27 Go?

Synthesizing these variables, the ynsugar Analysis Team maintains a highly cautious stance on the market. Factoring in a 5%–6% reduction in cane acreage, an estimated 10% decline in agricultural yields due to drought, and assuming a stable industrial extraction rate of 11.3%, Thailand’s sugar output for the 2026/27 season is projected to fall to roughly 10.0–10.3 million tonnes. This implies a sharp year-on-year contraction of 1.7–2.0 million tonnes.

Thailand Sugar Production Outlook (2026/27)

===========================================

[11.99 MMT] --> 2025/26 Bumper Crop (Actual)

|

| -- (5-6% Acreage Loss to Cassava)

| -- (10% Yield Loss via El Niño Drought)

v

[10.00 - 10.30 MMT] --> ynsugar 2026/27 Projection Range

This estimate aligns with the more conservative end of international trade forecasts, which generally span between 9.6 and 10.8 million tonnes. Notably, the USDA remains highly bearish, forecasting Thai sugar production down to 9.5 million tonnes due to the aggressive contraction in harvested area.

The critical variable to monitor over the coming months will be the monsoon rainfall distribution through October. Should the El Niño intensify as climate models suggest, Thai supply will likely collapse toward the USDA’s absolute lower bound, injecting substantial upside risk into world raw and white sugar premiums heading into 2027.

Sources: Office of the Cane and Sugar Board (OCSB); USDA Foreign Agricultural Service; Thailand’s Department of Climate Change and Environment; and ynsugar analysis. Figures are estimates and subject to revision as the season progresses.

Note: This article is intended for market-information purposes and does not constitute trading or investment advice.