The newly released Brazil UNICA sugar data shows that the world’s largest sugar producer and single biggest exporter is entering a critical phase. The latest production report from the Brazilian Sugarcane Industry Association (UNICA) for the 2026/27 harvest season presents a counterintuitive picture: mills crushed significantly more sugarcane through June 1, yet total sugar output actually fell year over year. The reason lies squarely in the sugar-ethanol allocation decision — and the implications for global sugar markets are significant.

Cumulative Season Data: Breaking Down Brazil UNICA Sugar Data

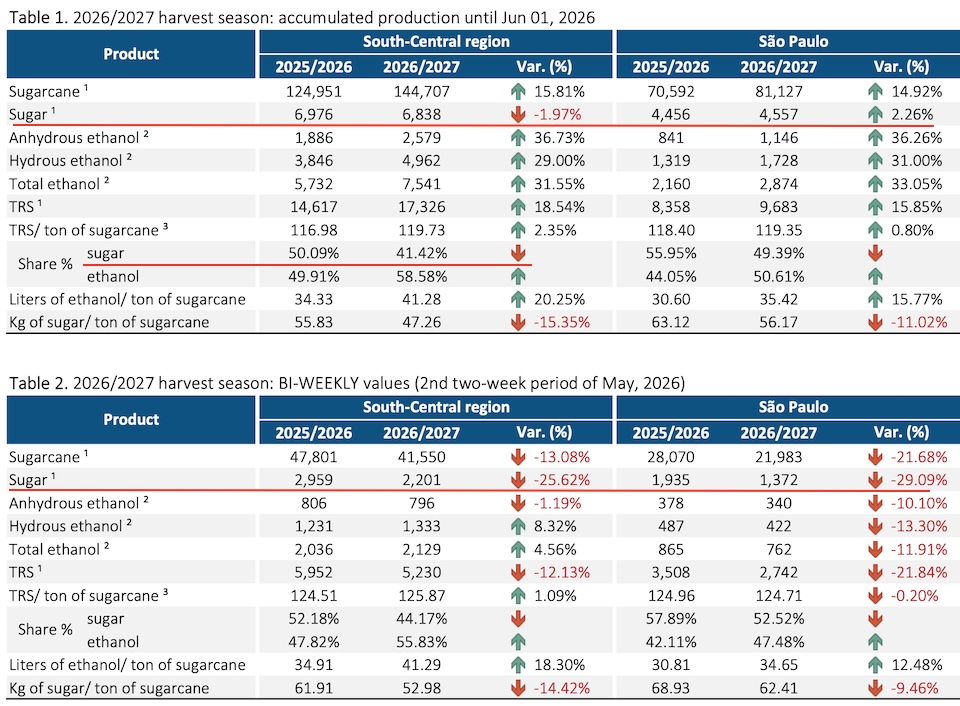

According to UNICA’s release, cumulative sugarcane crushing in Brazil’s Center-South region — the country’s primary production zone — reached 144.71 million metric tons (MMT) through June 1, 2026, a robust +15.81% increase year-over-year versus 124.95 MMT in the same period of 2025/26.

Despite that surge in raw material throughput, cumulative sugar production came in at only 6.838 MMT, down 1.97% from the 6.976 MMT recorded in the prior-season comparable period. São Paulo state — Brazil’s top sugar-producing state — bucked the regional trend, posting a modest +2.26% gain to 4.557 MMT.

The divergence is explained almost entirely by the dramatic shift in mill allocation ratios:

-

Sugar’s share of cane: dropped from 50.09% to 41.42% year-over-year

-

Ethanol’s share of cane: rose from 49.91% to 58.58% year-over-year

In practical terms, Brazilian mills processed nearly 20 MMT more sugarcane but directed the overwhelming majority of that incremental volume toward biofuel rather than sweetener production — resulting in 138,000 tonnes less sugar despite a much larger cane crush. Cumulative ethanol output reached 7.541 billion liters (+31.55% YoY), with anhydrous ethanol at 2.579 billion liters (+36.73%) and hydrous ethanol at 4.962 billion liters (+29.00%).

Bi-Weekly Snapshot: Late May Slowdown

The bi-weekly figures covering the second half of May 2026 paint an even sharper picture of the ethanol-first strategy:

During this fortnight, cane crushing slowed meaningfully — down 13.08% — but sugar’s production decline of 25.62% was nearly double the rate of the crush decline. This amplified drop reflects two compounding forces: fewer mills operating and those that were running allocating a smaller fraction of cane to sugar.

Cane Quality Is Strong — Sugar’s Decline Isn’t About Quality

One important clarification from the data: cane quality in 2026/27 is actually better than the prior season, not worse. The TRS (Total Recoverable Sugar) per tonne of sugarcane — a standard industry quality metric — rose from 116.98 kg/t to 119.73 kg/t in cumulative terms (+2.35%), and the bi-weekly value held above 125 kg/t. São Paulo’s TRS similarly improved.20260625-2-820.jpg+1

This confirms that the decline in sugar output is not a quality problem. The cane being processed is richer in sugar content than last year — mills are simply choosing to convert that sucrose into ethanol instead of crystallized sugar.

Four Market Signals from the YnSugar Analysis Team

Based on this data, the YnSugar analysis team identifies four key takeaways for traders and market participants:

-

No supply shortage at the cane level. Cumulative crushing in the Center-South remains well above the prior season’s pace, confirming no significant reduction in sugarcane availability for 2026/27.

-

Sugar output is now negative year-over-year despite a bigger crush. With crushing up 15.81% but sugar production down 1.97%, the message is clear: higher cane volumes are not translating into higher sugar supply. This could provide a degree of price support in international markets where Brazil’s sugar export capacity is closely watched.

-

Ethanol diversion is the single most critical variable this season. The Center-South sugar allocation ratio has fallen from 50.09% to 41.42% — a swing of nearly nine percentage points — and ethanol’s share has climbed to 58.58%. This is the most important data point in the entire release.

-

Oil prices remain the key external driver of the sugar/ethanol mix. Brazil’s flex-fuel mill infrastructure allows rapid reallocation between sugar and ethanol based on relative profitability. If crude oil prices remain elevated, the ethanol-first trend is likely to persist — and even a large cane harvest may not deliver the sugar supply volumes the global market is pricing in.

Why This Matters for Global Sugar Markets

Brazil’s flex-fuel milling model is unique globally: mills can shift cane between sugar and ethanol almost in real time based on price signals. With the government’s ethanol blend mandate under review and international oil prices playing a central role, the 2026/27 season is shaping up to be more ethanol-heavy than early forecasts suggested. Conab had projected Center-South sugar output at around 40.22 MMT for the full season — a 1.4% decline — and the early-season data trajectory is consistent with that outlook, or potentially more bearish for sugar supply.ynsugar+3

The bottom line: more cane does not automatically mean more sugar. As long as ethanol premiums remain attractive relative to raw sugar export parity, Brazilian mills have every incentive to keep the ethanol tap open — and the June 1 UNICA data confirms they are doing exactly that.

Data source: UNICA (Sugarcane Industry Association of Brazil), bi-weekly production report for the 2026/27 Center-South harvest season, released June 2026. Analysis by YnSugar.